John Koetsier is a journalist and analyst. He's a senior contributor at Forbes and hosts our Growth Masterminds podcast as well as the TechFirst podcast. At Singular, he serves as VP, Insights.

Where are location-based games in 2023? We all know Pokémon Go is the one massive success for location-based gaming, but it launched 7 years ago in 2016. Niantic Studios, the company behind Pokémon Go, is using the mapping built for Go into multiple games including Pikmin Bloom, launched in 2021, and NBA All World, which “turns the real world into a basketball theme park.”

What else is out there?

There’s a The Witcher-based game by Spokko, a Polish game development studio, there’s Orna, a “geo-RPG,” there’s Jurassic World Alive by Ludia.

But it’s not a huge category, and even Niantic had to punt on Wizards Unite, a Harry Potter-themed location-based game that just didn’t take off. So what does the future of location-based games look like? Is it possible that just one company can succeed in this niche?

“It’s not as big as I think it’s going to be, but I also don’t think it’s massive,” says Atlas Reality president and CTO Beau Button. “It’s not gonna like take over the gaming industry.”

That’s startling humility from a leader in a space. I’m not used to that, frankly. Most executives in a specific vertical are ridiculously, even insanely bullish on their chosen space. In some sense, they almost have to be, because not only do they need to convince themselves that huge success lies ahead in the venture they’ve dedicated a massive chunk of their lives to, they also have to sell it to potential employees, users, customers, and investors.

But it is realistic.

Gaming is big, and location-based gaming is probably going to stay a niche for some time. As is so many other forms of gaming, like puzzle games.

Here’s Button’s take on how to grow location-based gaming: don’t demand people invent new habits to play the game. Rather, build the game around what they’re already doing. It’s the classic don’t invent a parade marketing advice: rather, go find an existing parade and get in front of it.

“If we can do things that are fun and not change behaviors, but kind of augment existing behaviors, we can see success,” he told me in a recent Growth Masterminds interview.

His first game is Atlas Empires, which allows people to claim space in the “real” world, build fortresses, find resources, attack enemies, make alliances, become mayor, governor, or president of a territory, get virtual rent when your properties get popular, and earn virtual currency for watching ads. Currently the game is at 1.5 million players, Button says.

Interestingly, virtual in-game money can be turned into real cash via PayPal … not Ethereum, or Bitcoin, or some kind of no-name token, or some other layer 2 cryptocurrency. What Button has done intentionally is to build common web3 themes into Atlas Empires without building the underlying technology — blockchain or crypto — into the code.

“So I’ve always looked at the blockchain as nothing more than like an evolution of a database,” he says. “And I was inspired by not only the blockchain on how it worked, but some of the games that were built on top of the blockchain.”

But blockchain and wallets and cryptocurrencies come with a cost.

“I wasn’t convinced that it was ready for the mainstream because the onboarding flow for web3 — getting a wallet, remembering where to put your keys, is it a custodial wallet, a non-custodial wallet, is it a hardware wallet — those are not terms that are easily digestible by average gamers.”

Plus, the common challenge to any mobile game is that whenever you increase your seconds-to-fun count, you lose players. Which means that perhaps you don’t have to be a purist around the technologies underlying your game as much as a participant in the ethos of decentralization, sharing, and distributed ownership.

A lot of that makes sense, I think.

Another design choice, of course, is making the game location-based, adding world-as-a-service via APIs from Mapbox. But Atlas Reality has done that sparingly: you don’t have to walk or drive around if you don’t want to, although doing so does add to the gameplay. Which is probably a good idea if we’re thinking about the future of location-based games: use location when it adds to gameplay, not in every situation and scenario

It’s hard to see if we’re going to eventually have a rich diversity of thousands of location-based games. But it’s pretty clear that we’re likely to see an emerging distinction between location-based games and location-aware games. While both might be a bit challenging for people who don’t travel or move around much, location-based means location is a core part of the gameplay. I wouldn’t be surprised to see location-aware games become more and more common where location impacts gameplay, but doesn’t drive it.

Think Subway Surfers in your current city while traveling.

Think regional battles and championships for specific geos in battle games.

Think puzzles with location-relevant items … and much more.

The M-word features in here as well: metaverse. The more we see digital elements overlaid on physical geography, the more gamified any enhanced experience is likely to become, whether that’s in utilities like mapping, in social apps, or in ratings/reviews apps. Ultimately, the true golden age of location-based games (and apps) is likely in the medium-distance future as we get smart glasses that take over some of our smartphones’ functions.

But hopefully we’ll also see more successes in the space before then. Any niche with just one major competitor is a little boring.

Check out our entire chat in the full video, or subscribe to the Growth Masterminds podcast on your preferred platform:

We’re now in the era of privacy in mobile adtech. Apple and Google kicked it off in 2012 and 2013, respectively, with Limit Ad Tracking on iOS and a toggle to turn off Ad Personalization on Android. Apple upped the ante in 2021 with iOS 14.5 and App Tracking Transparency, which makes the iOS ad identifier (IDFA) rare, while Google will roll out Privacy Sandbox for Android in late 2023 and into 2024, which will make the Android ad identifier (GAID) extinct.

Limit Ad Tracking is now part of history, having been replaced by App Tracking Transparency.

But before it did, LAT limited advertiser visibility on users’ ad actions significantly, hitting 31.5% in the U.S. and a global average of 15.61%. This was a rare instance of the U.S. leading the world in privacy: usually Europe is much more privacy-conscious.

But people anywhere on the planet opting out of ad personalization on Android was extremely rare in 2020. Only 2.3% of people opted out in the U.S., while just 3.14% in Germany, 1.4% in India, and 3% of people in France switched the toggle to stop ad personalization on.

Where are those numbers now in 2023?

Ads personalization on Android: what 5 billion events show

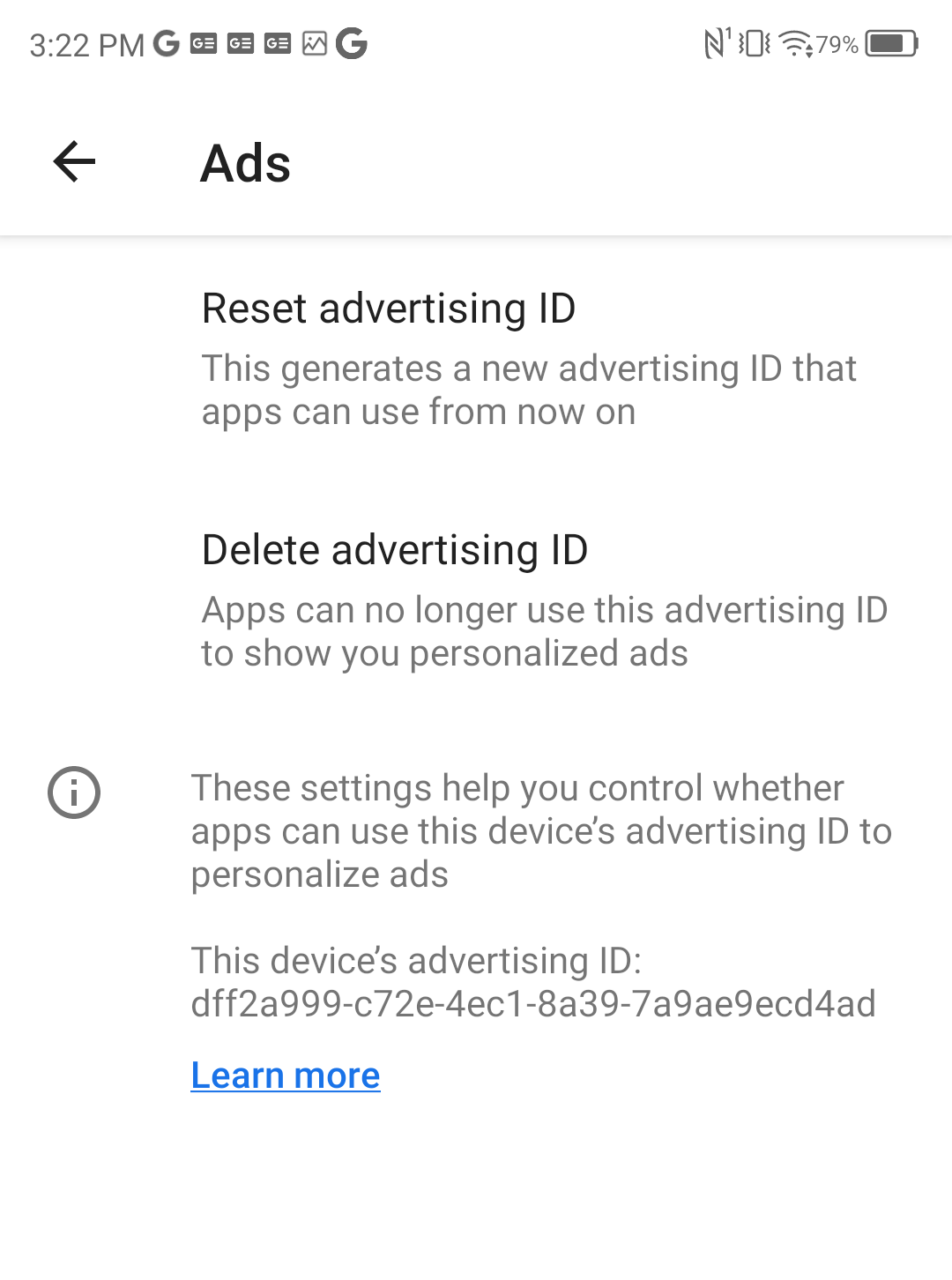

Ads personalization on Android has changed somewhat over the last few releases of the Android operating system. From a toggle to opt in or out of ad personalization the control has been split into two binary options:

Reset your advertising ID (this restarts your device’s digital breadcrumb trail, so to speak)

Delete advertising ID (this removes the GAID entirely, meaning ads can no longer use it to show personalized ads and — though this part isn’t mentioned — track your activity around the digital ecosystem)

Either option is easy to do, though finding the right place to do it might take a few moments of searching.

Few people, however, bother. In fact, almost everyone opts in.

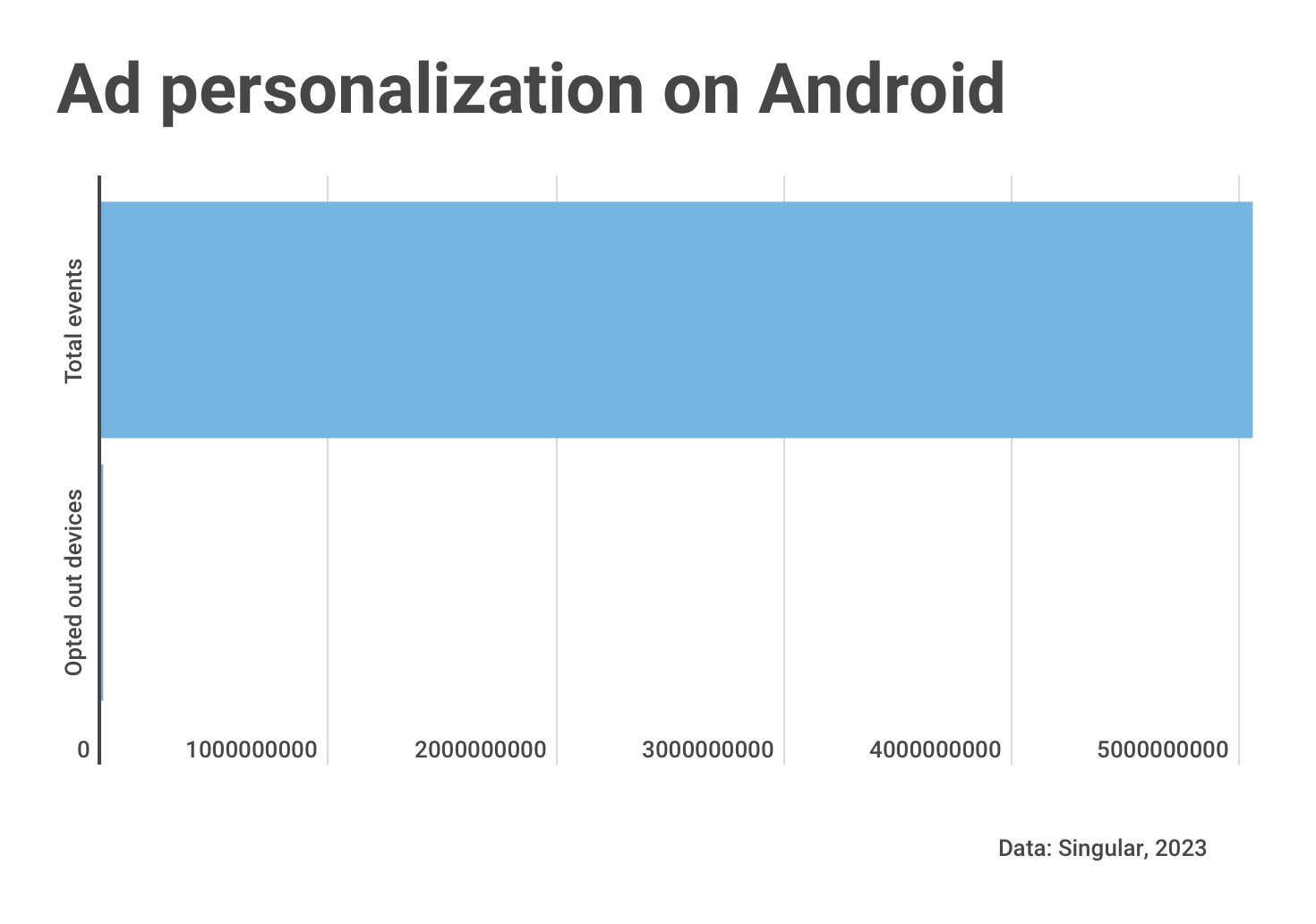

We queried data from over 5 billion ad events on Android smartphones last week: mostly ad impressions, some clicks, some app installs. Out of this massive number, only 9.2 million were from devices that opted out of tracking by deleting the Google ad ID: in other words, saying no to ad personalization on Android.

That’s a miniscule .18%.

Devices linked to some networks and services opt out much more

While the overall average is tiny, there are specific networks and marketing platforms that engage with devices that are much more likely to have deleted GAIDs. Many of them are from top Chinese phone manufacturers, plus Sony in Japan:

Sony: 5.47%

Xiaomi Global: 4.87%

Samsung: 3.07%

Oppo: 2.07%

Vivo: 1.9%

Others are from ad networks or agencies, typically with business in China or India:

Realme: 2.99%

SingleTap: 2.32%

GMM 1.38%

Cronbay Technologies: 1.08%

Mintegral: .54%

Ignoring some outliers with tiny numbers of events that hit 20% or even over 30%, filtering by ad partners with at least 100,000 events shows that even the most privacy-centric customers in the most privacy-concerned regions rarely delete their Google ad ID.

The one common denominator here is companies that do business in China and India, which seem — at least in the case of ad personalization on Android — to be more privacy focused than the rest of the world. SingleTap is a Digital Turbine technology for instant app installs on Android that bypass Google Play. Cronbay Technologies is an Indian marketing agency.

In almost no cases do the numbers really approach significance. Even at a 5% opt-out rate, advertisers are still seeing customer journey data on 95% of their potential customers or users, which is more than enough to avoid hampering any ad optimization they wish to do.

What does this low rate mean?

A few things are obvious here.

People are pretty OK with ad personalization on Android on a global scale.

Either iOS users care a lot more about privacy than Android users in general, or Apple’s positioning on privacy made iPhone owners much more conscious about the technology they can use to restrict access to their data. Their Limit Ad Tracking rates were high on pre-ATT iOS, and their opt-in rates for App Tracking Transparency hover around the 20% range, meaning 80%, the vast majority, decline to allow apps to track them. Given that ATT is a double opt-in scenario requiring a yes on both the publisher and advertiser apps (both the app that carries an ad and the app that the ad advertises) IDFA access on iOS in 2023 is rare.

But Android users opted out of ads personalization infrequently in the older versions of the Android ad ID customization screen, and delete their GAIDs even less frequently now.

A big caveat:

Theoretically, there could be a large cadre of Android users who don’t delete their advertising IDs but simply reset them from time to time. This would enable a limited amount of tracking across digital touchpoints: somewhat helpful for advertisers, and more privacy-enabling for people.

I don’t have the data to either suggest this is the case or disprove it. But it seems unlikely. I only go to my Settings app when needed for some specific reason, not to browse or pass the time or to periodically refresh a setting, and I supposed that most are like me at least in that regard.

What this means for the future of Android is not obvious.

Google will most likely launch Privacy Sandbox for Android late this year or early next. Unlike the iOS ATT, which doesn’t eliminate the IDFA but makes it user-optional, Google’s changes will hard deprecate the ad identifier on Android. So it’s not like Android users’ behavior now will say anything about their behavior under Privacy Sandbox: there will be nothing to grant or deny.

Most likely, what it says is that Google’s increased privacy moves on Android will be well-received by end users, if they even bother to notice.

According to emails viewed by the Wall Street Journal, Twitter’s having a buy-one-get-one-free ad sale. Twitter BOGO means you can buy up to $250,000 in advertising, and the social/news/entertainment platform will match it with another $250,000, free of charge.

One catch: you have to complete all your ad spend — up to $500,000 worth — by February 28, according to the WSJ story.

Twitter BOGO free ad sale: are you in or out?

As a growth marketer or mobile user acquisition specialist, you have to at least consider this. There are valid questions to be asked and answered about brand safety and the overall direction of Twitter post-acquisition by Elon Musk, of course. And there are reasons that over 500 former Twitter advertisers have reportedly paused campaigns on the news social platform.

But when you have a chance to get a 2-for-the-price-of-1 free ad sale on an established and successful advertising platform, you have to at least consider it.

Here’s some data to help you make a decision.

Mobile user acquisition spend on Twitter in 2022

Elon Musk’s acquisition of Twitter officially completed on October 27. But it’s hard to see how all the angst about the on-again, off-again acquisition impacted advertiser spend in calendar by Singular advertisers’ spend on the platform in calendar 2022.

Except two oddities:

A massive post-summer, pre-acquisition jump

No typical year-end holiday bump

Somewhat strangely, while spend jumped 144% from August to September and app installs paced spend with a 134% increase, ad impressions grew by only 38%, suggesting that Twitter presumably got much more efficient at translating traffic to cash. Clicks on ads jumped by about the same third as ad impressions.

After a sharp dip in October from the September spike, post-acquisition ad spend by Singular customers actually rose about 12% between October and December, more or less followed by impressions and clicks.

But in a worrisome sign, app installs dropped by 52% across the board in pretty much a continuous downward-trending line between September and December 2022.

Big picture, Twitter has dropped slightly in market share for ad spend year-over-year, as clients who check the Singular Benchmarks data can verify. But its share of ad spend is higher than its share of app installs, suggesting that installs from Twitter tend to be significantly more expensive than from other sources. As sophisticated mobile marketers know, this is not necessarily a bad thing if quality is good. (More on that later.)

Moving right up to the present day, the median cost to generate an app install via Twitter is $2.32, but the range is large and extends up to $11.22.

Twitter’s placement on the Singular ROI Index for 2022

Twitter was a top-10 ad network in the Singular ROI Index for 2022, with placements on no fewer than 19 lists, including 8 rankings in the top 5 for specific categories or regions. Twitter achieved rankings on lists of top ad networks for categories such as:

Best ROI for Android

Best ROI for non-gaming

Top North America

Top EMEA

Top APAC

Top retention

Best ROI for iOS

In short, while Twitter wasn’t the best ad network in the world for app install marketers, it was certainly on the list of those to think about, especially in non-gaming categories. Quality has been there, historically.

Singular ROI Index 2023: where Twitter will slot in

The Singular ROI Index for 2023 has yet to be released, and I’m not going to spill the beans on all the details of where Twitter ranks right now.

But what’s increasingly obvious in the era of SKAN is that those platforms that own their own supply and demand for advertising tend to do well. I’m talking about companies that sell ads via their own tools against inventory on their own platform … the Facebooks, Googles, Snapchats, Reddits, and TikToks of the world. While Twitter has lost a lot of talent — including sales and marketing staff that big customers like to be able to contact — Twitter is in that conversation as well.

First-party data, as everyone in adtech knows, is increasingly valuable.

What that means for the 2023 Index is that Twitter actually improved its overall positioning, coming in tied for seventh for the most rankings on top ad network lists per geo or vertical. In a year of turmoil and change, that’s no small achievement.

(For more details, stay tuned for the release of the Singular ROI Index in a few weeks.)

Decision time: spend big on Twitter’s free ad sale now or not?

Gaming has never been a big strong suit for Twitter, so I’ll confine my remarks to non-gaming verticals. (This doesn’t mean don’t even think about it if you’re marketing a game, but it’s going to be a harder decision as a game to be a buyer on Twitter’s BOGO sale.)

Twitter has consistently ranked in the top 10 of ad networks for return on investment. If you feel that this historical achievement is likely to continue in an environment where there’s been some significant change and accompanying angst, testing the waters might be a good idea.

Some things to think about:

Do you have recent data for your app on Twitter performance?

The easiest way to say yes Twitter’s free ad sale to this opportunity is if you’ve been continually advertising on Twitter over the past 4 months. If you’ve been seeing positive ROI and no downside or significant negatives, going bigger for free is a no-brainer.

If that’s not you, you have some (but very limited) time to do a quick test and make a decision. (Or try to negotiate an extended deadline.)

Super Bowl

One thing to keep in mind: Super Bowl 57 will be played on February 12. Activating your spend in early February in North America will compete, to some extent, with that hype. But there’s two bits of good news if you’re not a tremendously sports-oriented app:

While there’s no denying it’s a massive event, globally speaking the Super Bowl is fairly regional, and you can market in APAC or EMEA with limited crossover

You have until February 28 to complete your bonus campaigns, which is well past the Super Bowl time frame

And guess what: Twitter is offering this sale because it needs more revenue. That means there might be room for negotiation behind closed doors on when you actually need to complete the spend.

Cheaper ad spend for a triple boost?

Which brings up another good point: ad spend is down on Twitter in general. According to Pathmatics, the top 30 advertisers dropped their spend by 42%, contributing to “Twitter’s fourth quarter revenue [falling] about 35% year over year.”

When ad spend is down, cost per slot should be as well as there’s less competition. Which could lead to a triple boost for your Q1 Twitter ad spend:

Natural boost from your paid spend

Extra boost from the BOGO offer

And yet more boost due to advertising in a less competitive environment, meaning that there’s potentially both cheap ad slots and less surrounding noise

The decision is yours

Ultimately, the decision is up to you.

It’s obviously not just about the free ad sale opportunity on Twitter. It’s also about your capability and appetite for risk. But if budgets are down and belts are tightened for a ride-out-the-economic-storm strategy, you may not be able to take advantage even if you do think it is a good option.

If you have available ad dollars, however, it might just be worth diverting them to Twitter for a few weeks to take advantage of a very rare opportunity.

The SKAN 4 era has begun: we are now seeing live SKAN 4 postbacks coming from ad networks.

The scale is tiny right now, so don’t get too excited. But getting live SKAN 4 postbacks is a big deal. This is not just the beginning of the next evolution in iOS marketing under SKAdNetwork, it’s the beginning of the ability of ad networks to test and iterate their implementations of SKAN 4. And it’s also the first step in marketers and analytics providers like Singular learning how the new crowd anonymity, postback timers, and conversion values will function in the real world.

First step in SKAN 4 adoption

“Singular processing SKAN 4 postbacks is the first step in SKAN adoption,” says Singular product manager Omri Barak. “It’s a chance to start looking at the privacy thresholds and seeing the behavior out in the wild.”

It’s very unlikely that any ad network will send live SKAN 4 postbacks at scale right now: they know marketers and the ecosystem at large aren’t ready for a full transition, and may not be until Q3 this year. So if you’re not 100% set up for SKAN 4, don’t panic.

You still have time to prepare.

What we will be seeing over the next few weeks are really early postbacks, Barak told me: networks still have a long way until they actually move the majority of traffic to SKAN 4. A big part of the challenge for all the ad networks and major marketing platforms is deciding on their strategies for how to use the new source identifier, coarse conversion values, and extra postbacks. This is a big, big deal: get it right and ad networks can achieve better signal, better campaign management, better creative optimization, and ultimately better results with more conversions. And that, of course, can expand their market share.

Get it wrong, and the consequences won’t be so pretty.

What you need to do now

The most important question for marketers right now: what do I need to do?

First, make sure your entire team is getting ready for SKAN 4. We just published a massive and comprehensive SKAN 4 strategy guide with details on the changes, preparations you need to make, implementation of your SKAN 4 strategy, and operational details on what you can expect from Singular in terms of marketing analytics. (It will soon be available in guide form so it will be more readable and have better, more explanatory graphics, but it’s complete right now.) Check it out and, if you need, contact us to get help.

Second, talk to your ad partners.

“Marketers need to check with the networks they are advertising with to see if they are signing their ads with SKAN 4,” says Barak. “If so, they can expect delays in postbacks, as all SKAN 4 postbacks by default would be sent after 48 hours.”

Again, don’t panic: if your networks are testing SKAN 4 now, they won’t be sending 100% of your postbacks as SKAN 4 postbacks. They’ll probably just be sending a very few for testing, so you’re not going to lose a lot of signal. Also, while most MMPs still only update in the first 24 hours, Singular clients’ current active models will not be affected, Barak says, for models that are up to 48 hours. Data in these SKAN 4 postbacks is available in your Singular logs, your reports, and your ETL deliveries.

When we’ll see live SKAN 4 postbacks at scale

Note: what we’re seeing right now are SKAN P1 postbacks … the first of 3 postback that SKAN 4 provides.

SKAN 4’s second and third postbacks probably won’t show up for many marketers, if any, because likely zero or almost zero marketers have SKAN 4 models set up with their MMPs yet. Once that’s available and created, then postback 2 and postback 3 will become available.

If you’re a Singular client, chat with your customer success manager about this; if you’re not, feel free to book some time with a Singular expert to talk it over.

The big question on everyone’s mind, of course, is when we’ll see SKAN 4 postbacks in the wild at scale. That’s most likely calendar Q2 this year, says Singular CTO Eran Friedman.

“The volume doesn’t matter much right now,” he adds. “The big news is that SKAN 4 is live and working, and we’re the first to show our customers their testing results.”

How do you know when your mobile app marketing campaigns are working?

Traditionally this has been fairly easy for mobile marketers on iOS, using the IDFA (Identifier For Advertisers.) However, since iOS 14.5, the IDFA is only available upon request via Apple’s App Tracking Transparency modal, and only about 12% of iPhone owners say yes to Apple’s App Tracking Transparency.

That cuts the amount of data that marketers rely on to optimize ad campaigns by almost 90%.

So Apple’s recently updated SKAdNetwork framework is now essentially the only deterministic way to measure mobile app marketing success. And that’s why it’s critical for app publishers to deeply understand and fully exploit all the data that Apple does provide for advertisers in the fourth major iteration of the company’s SKAdNetwork framework, SKAN 4.0.

“SKAdNetwork is a framework created by Apple for privacy-preserving mobile app install attribution,” Friedman said in a recent presentation for GameCamp via Google for Startups.

If you’re in the mobile advertising space, you probably know a ton about SKAdNetwork and App Tracking Transparency already. (See this post on SKAN 4.0 strategy to learn more about transitioning from SKANn 3.) If you’re not, however, Friedman explains the broad strokes:

Advertisers with apps they want to promote buy ad campaigns from an ad network

Ad networks buy space in app publishers’ apps for the ad. Each campaign needs a specific SKAN campaign ID.

The ads get shown to people using a publisher’s app

The person who sees the ad taps on it, installs the advertiser’s app, and launches it

Code inside the newly installed app watches for specific predetermined behavior in the app, and if it sees something like “completed level” or “subscribed” or “purchased,” updates a conversion value. This value is not tied to a specific person or even device, and can only be a number between 0 and 63. (That’s part of Apple’s “privacy-preserving” technology.)

After a randomized timer between 24 to 48 hours, the device sends a notification — a SKAN postback — to the ad network to let them know their ad campaign worked.

If and only the number of app installs from that campaign surpasses an Apple-set privacy threshold limit, postbacks will include conversion values.

(Note: some of these details are changing in the currently ongoing transition from SKAN 3 to SKAN 4; more details here on what those changes include.)

MMPs like Singular, of course, have been helping marketers make sense of all this. Up to this point under SKAN 3, they’ve been doing 4 key jobs:

Collecting all postbacks

Enriching them with campaign information

Decoding numerical conversion values to human-readable names

Modeling missing data, since about 21% of all SKAN postbacks don’t carry conversion values due to Apple’s privacy thresholds

The goal in the fourth step it to replace as much data as possible and emulate, as much as you can, the data that was fully visible before App Tracking Transparency, when 70-80% of iOS installs were measurable via IDFA (the Identifier for Advertisers that now requires App Tracking Transparency consent to acquire.)

“The end result that you want to get from SKAdNetwork is providing a report with the full analytics, end-to-end, of your best-performing campaigns,” says Friedman. “For a specific source, such as Google, you see how much you’ve spent, how many impressions or clicks, how many SKAdNetwork installs you received … without the need for consent, total installs across all users that came from this campaign.

“From this you can calculate your CPI, your CPM, your CPC, you can even decode back your revenue coming back from your conversion values providing ROI on your campaigns.”

But the real magic, Friedman says, requires modeled data.

SKAN intentionally drops data due to privacy constraints. If Apple gave you everything, instantly, some would be able to correlate SKAN postbacks with specific devices and people. So privacy thresholds in SKAN 3 and crowd anonymity in SKAN 4 delete some of that data, and SKAN applies random timers to postbacks to obfuscate individual actions. The result is that SKAN data on its own has a major problem from a marketing perspective: campaigns can look both expensive and ineffective. Marketers looking to scale good campaigns and drop poor performers lack sufficient compelling data to make those vital calls.

The solution: modeling SKAN data by enriching it with first-party data, thereby giving advertisers an accurate picture of results while not violating privacy.

Of course, Apple is now updating SKAdNetwork to SKAN 4.

The software is already released, but there’s a lot of work happening behind the scenes in the mobile adtech ecosystem to make it all work. Singular released a SKAN 4-compatible SDK in November of last year, but there’s a lot more work to be done by ad networks, advertisers, and app publishers.

SKAN 4 will provide richer data in the first postback advertisers can get — assuming high levels of installs per campaign providing significant crowd anonymity — and additional postbacks over time to get more insight into campaign performance over time. Singular’s using these additional signals to enhance the virtual cohorts SKAN Advanced Analytics already provides. The complete SKAN 4 version of SKAN Advanced Analytics, Friedman says, will add new elements to the 4 key jobs above, including long cohorted KPIs, extremely accurate data estimations thanks to SKAN 4’s additional data, and decoded SKAN 4 coarse conversion values.

Watch the video embedded above or on YouTube for a full explanation of both our current situation and the ongoing transition to SKAN 4.

The pandemic years were the golden age of subscription-based connected TV as streaming media companies invested tens of billions in new content, shows, and platforms.

The post-pandemic years will be the golden age of ad-supported connected TV as the streaming media ecosystem switches from a blue-ocean go-get-em new customer acquisition phase to a red-ocean hyper-competitive go-win-em model.

Another factor: consumers struggling with subscription fatigue in uncertain economic conditions.

“Viewership from platforms that have ad-supported placement is growing one and a half times faster than the rate of subscriptions for streaming services,” says Guillaume Lelait, managing director Americas at M&C Saatchi Performance in a recent Growth Masterminds podcast episode.

So what are the opportunities for mobile marketers in this emerging space?

Fast growth in connected TV and streaming media

Another M&C Saatchi executive that I recently spoke to, Jonathan Yantz, suggested that ad spend in connected TV might eventually rival ad spend in social media. That’s a big prediction, given that Facebook ad revenue alone is already in the $100 billion annual range while connected TV is forecasted to be around $39 billion (U.S. only) in 2026.

But connected TV ad revenue has been growing fast.

Plus, 92% of U.S households are already accessible on connected TV, and you have to think that good-old-fashion TV advertising, still at almost $70 billion in 2022 (U.S. only), will mostly transition to connected or streaming TV over the next few years.

That adds a lot of runway for growth.

“CTV ad spend represents 18% of the whole video ad spend,” Lelait says. “Linear, it’s still 57%.”

And while growth of the CTV advertising industry is slowing to perhaps 30% annually over the next few years after a torrid 40-50% annually in the last few years, that’s still double the growth of mobile ad spend, Lelait adds. So as the bulk of linear TV ad spend transitions over to connected TV and streaming, there’s huge upside potential.

CTV advertising is a different world than mobile advertising

Much as those of us who have cut our teeth in tech during the long rise of the smartphone to computing platform supremacy might wish otherwise, mobile is a mature space. It’s known. It’s consolidated.

There are 2 major powers: Google and Apple.

And, correspondingly, there are 2 major channels: Google Play and the iOS App Store.

We’ve lived this now-familiar world for more than a decade, and we know it pretty well. We know the ad formats that work, the agencies that make the ads, the DMPs and SSPs and exchanges and mediation platforms that deliver them, and the attribution solutions that measure them.

Connected TV is a different world. And it’s not just one world, either.

Connected TV is technically internet-connected TVs from brands like Sony, Samsung, LG, and others

Streaming is technically services such as Netflix, Amazon Prime Video, Disney+, Hulu, or Peacock

OTT is technically hardware platforms such as Apple TV, Amazon Fire TV, Roku, cable/satellite TV boxes, and more

All of these are slightly different, but all are getting mashed up as platforms, channels, services, and hardware get extensively interwoven in a considerably more complex and less consolidated landscape than mobile. The result is that you can get Apple TV+ (the service) on a connected Sony TV, or Roku Channel (the platform) on a Vizio smart TV, or Amazon Prime Video and Disney+ on Apple TV (the hardware), or pretty much any streaming service via Roku hardware, and so on. Throw in Hulu, Peacock, HBO Max, Paramount+, Tubi, Crackle, Pluto TV, and many more … and there are a huge number of players.

And of course some players, like Apple, Roku, and Amazon, play in multiple spaces, offering all of hardware, software, platforms, and services. Plus both connected TV and OTT platforms offer app-store-like functionality, allowing consumers to install different streaming services in addition to natively-available channels, entertainment, and functionality.

The upshot is that the CTV and streaming ecosystem is vastly different from mobile, and significantly more complex in some ways.

The ad formats are very different too.

“A large amount of the inventory is video based, and it’s actually non-skippable,” Lelait says. “Compared to Facebook, Instagram, TikTok, where everything we think about is hook rate — how many seconds is someone watching — here the platforms are like: ‘We are seeing your campaigns worked. You had a 96% completion rate.’”

Another difference: the ad slots are typically 15 seconds and 30 seconds, much like linear TV. But there’s far fewer ad slots than either mobile or linear TV.

“If you play a casual game, every couple of levels you get exposed to an ad,” Lelait says. “On CTV, it’s about four to six minutes per hour.”

Measurement on connected TV: a whole new world

Attribution and measurement are still fairly new in the CTV market.

One way connected TV players enable marketing measurement is by matching at the user level. For example, a CTV platform might pass ad views to a DSP, and the DSP will work with a measurement provider such as Singular to match these with devices who took action on the ad campaign.

That’s good as far as it goes, but there are obvious challenges.

“They basically create the attribution in a very, ‘Well done, you achieved a $6 CPI’ way,” says Lelait. “But what you actually don’t really know is that the conversion may have happened from another channel — from Facebook, Google — during the same window of time.”

But there are also additional models, including using impression tracking via tags, which is not universally supported, or click measurement on Singular links via a remote control, for example. Linear TV’s panel-based methodologies that estimate viewership are of extremely limited value.

One method Lelait is decidedly not sold on is the QR methodology that Coinbase made famous in their $14 million Super Bowl ad. Despite virtual menus in restaurants accessed via QR codes, they’re still not a common functionality for most people.

“We have a [running] joke with someone: ‘Please, the moment you see a 1% engagement rate on your Q code … send me the report,” Lelait says.

There are also measurement SDK integrations.

A streaming provider, for instance, that is resident on both a smart TV app and a mobile device might notice engagement with an ad and kick off a push notification on a consumer’s mobile device, where he or she can more easily take action. That’s an interesting option particularly for massive companies like Amazon or Google, who are likely to be installed both on your TV and your phone, and both of whom can use their vast troves of data to understand which ads to target to which audiences. But it’s also a major reason for streaming providers to work hard to make all customers multi-device.

About targeting: that’s another key point of differentiation.

Targeting on mobile has generally been behavior-based, though not on iOS since App Tracking Transparency. Targeting on CTV can use first-party data that platforms gather on your viewing behavior, or it could use prior purchase or search data, potentially, in the case of Amazon or YouTube. But targeting on CTV is more likely to be via demographics, geotargeting, income targeting, and other household parameters.

Which, in conjunction with contextual targeting based on content being shown can be quite effective.

What verticals CTV advertising works for

“Apps and gaming will lead the way,” Lelait says. “[But] I think commerce is going to really take over on CTV.”

There are mobile app install campaigns on connected TV, and they continue to achieve significant results, just like mobile app install campaigns on linear TV. But over time, commerce might be the sweet spot, Lelait believes. Which, of course, aligns with what has worked on linear TV in the past, and therefore also aligns with what linear TV advertisers who are moving over to connected TV and streaming TV are familiar with.

One interesting opportunity: triangulation.

Or, as another marketer I chatted with once called it: surround sound marketing: on your big screen on the wall and on your little screen in your hand.

“We are seeing … traditional mobile DSPs who now have an offering on CTV and what they’re doing is actually smart,” Lelait says. “I’m going to keep the IP of the household where the ads have been shown. And then on top of that I’m going to run some display ads and also some re-engagement campaigns. So you can see how they are bringing maybe a DMP in the middle and they’re trying to triangulate you and, and basically extend the reach that those DSPs all have.”

How’s that going to work?

Giants like Google are able to connect viewers with search data, show ads that relate, and allow people to engage with those ads via their Apple TV remote, or TV remote, or on their phones.

Looking for open-source SKAdNetwork software to kickstart your SKAN 4 implementation? Apple’s update to SKAdNetwork for SKAN 4 is the biggest change in mobile advertising on iOS since the formal launch of SKAdNetwork with iOS 14.5 in early 2021. SKAN 4 is a massive update, changing how many postbacks advertisers get, offering richer post-install conversion insight, and featuring complex conversion-value locking and postback timing capabilities.

It’s tough to prepare for this change, largely because SKAN is a complicated dance between advertisers, iPhone owners, ad networks, publishers, and devices themselves.

It’s easier, however, if you have some reference code to work off of.

That’s exactly what Singular is providing in a convenient SKAdNetwork-App GitHub repository, where you can find sample apps demonstrating the logic you need to implement SKAdNetwork as an ad network, as an advertiser, or as a publisher.

Open source SKAdNetwork software: What the GitHub repo contains

Similar to the code Singular released in 2020, the repo contains code for:

An advertiser sample app (the app that advertisers’ want to drive adoption of)

A publisher sample app (the app that will show an ad to a potential new user)

A server that simulates an ad network API, including ad signing (the ad network serving the ad)

Use this open source SKAdNetwork software to build and test your own SKAN 4 implementation. Note that if you’re working on SKAN 4 compatibility, you’ll need to be working in Xcode 14, not prior versions of Xcode.

If you’re building towards SKAN 4 support, also check our SKAN 4 readiness checklist, which includes details on who you need to talk to in order to enable full support, updating the Singular SDK in your app, and information on sharing your source hierarchies with ad networks so that they can optimize your campaigns based on creative, ad sets, offers, or other criteria.

SKAN 4 is challenging, but it offers much more

The good news about enabling SKAN 4 support with Singular’s recently updated SKAN Advanced Analytics is that you’ll get:

More accurate long cohorts

Visual reporting on D2 revenue, modeled D7 revenue

Additional data via coarse postbacks

Confidence intervals on modeled revenue

D30 revenue

Singular was first to announce SKAdNetwork support in 2020, first to release reference code for implementing Apple’s mobile attribution framework in June of that year, and first to announce MMP SDK SKAN 4 compatibility in November of 2022.

What that means is simple: we’ve got your back in an increasingly complex mobile marketing environment.

It’s a sad exercise to look for the top mobile marketing podcasts on Apple Podcasts. Most of what you see is general marketing theory, Shopify store optimization, influencer marketing tips, or social media marketing. It’s a bit better on Spotify — better search engine, perhaps — but the first result, like many others, is a podcast that hasn’t been updated since September 23, 2021.

Not helpful.

If you’re like me, you’re looking for the best mobile marketing podcasts right now. Not ones that haven’t been updated since 2016, not ones that are re-broadcasts of a conference’s sessions, and not podcasts that are about general marketing issues. Mobile marketing and mobile advertising are both incredibly niche in terms of technology and knowledge and jargon and also incredibly central and important as the fastest-growing space in marketing over the past decade.

So a mobile marketing podcast needs to be specifically about mobile, and specifically about mobile marketing to be able to provide insights and anecdotes that will be at the same time interesting and helpful to mobile growth professionals. And yeah, while I like Prof G too, if it’s not specifically about mobile AND marketing, I can’t include it on this list.

Here’s some of the top mobile marketing podcasts I’ve found and enjoyed. If I missed one you like, ping me about it!)

Two & a Half Gamers Podcast

If you know Matej from his Brutally Honest newsletter, this podcast will be interesting to you. A practitioner, consultant, and mobile expert, Matej Lancaric produces this mobile marketing podcast with Jakub Remiar, Felix Braberg, and a few guests here and there.

What’s particularly good:

They’ve been there and done that, and so you’re getting insight from people who know what they’re talking about. Plus, having a bunch of experts in a (virtual) room all together ensures you get some interesting interactions that liven up the “no bullshit” conversation.

Eric is smart and opinionated, and sees a lot of the data that defines the mobile ecosystem and the app economy. Add that to generally interesting guests with good vantage points and interesting points of view, and you’ve got the recipe for learning most times you push play on the Mobile Dev Memo podcast.

What’s particularly good:

Big picture meets boots on the ground. As much as we hate to admit it, macroeconomic forces impact everyone’s business, and understanding what’s happening at the high level while being able to apply that to the nuts and bolts of running a mobile-centric business is what makes Mobile Dev Memo impressive. And what makes it one of the best mobile marketing podcasts.

Besides, the great name, this is a smart and funny podcast that focuses on — you guessed it — the gaming industry, with a strong focus on mobile. It’s about business and growth and all that they require, but it’s done in an entertaining way. Deconstructor of Fun is hosted by a somewhat rotating cast of characters including Michail Katkoff, Eric Seufert, Eric Kress, Laura Taranto, Adam Telfer, and Ethan Levy.

What’s particularly good:

Sure, it’s games professionals, but the unique benefit of this podcast is the large group of hosts. Somewhat unusual in the world of business or marketing podcasting, having multiple hosts means you’ll always get a different opinion.

Mobile Heroes Uncensored interviews every Liftoff mobile hero from the biggest app publishers like Rovio and Huuuge and Mattel and Call of Duty and India’s Times Internet, but also tiny apps that lonely mobile marketers are scaling in comparative obscurity. It’s hosted by Peggy Anne Salz and — yeah, sorry, full disclosure — yours truly, but in spite of that egregious conflict of interest I swear it’s actually really fun.

What’s particularly good:

Peggy and I are pretty much total opposites, so you can count on very dissimilar ideas, questions, and reactions. Pair that with a continuing cast of top-notch mobile experts and our ongoing efforts to make them say uncensored things, and it’s not half-bad.

Steve runs the App Masters agency, the App Masters conferences (at least pre-Covid, and maybe again!), runs App Masters Academy, and hosts the App Masters podcast. That’s probably enough for any average superhuman, but the net net for the podcast is someone who can speak, interview, and has the knowledge needed to get the best insights out of his guests.

What’s particularly good:

Steve has a laser focus on growth. Many other mobile marketing podcasts hit a wide variety of topics, which is great. When you want something that is always going to give you an hour with someone who is growing their mobile business and telling you how and why, App Masters is a great place to start.

Going strong since 2018, which not every podcast can say, Apptivate is a how-to podcast for mobile marketing by Remerge, the ad network/agency that made a name for itself in retargeting. Need help with contextual vs behavioral targeting? There’s an episode for that. Want to get better at offer walls? There’s an episode for that too … and pretty much any other topic you’d want from mobile marketing podcasts.

What’s particularly good:

Each episode targets a specific challenge or problem, so if it’s something that you need help with, care about, or just want to hear how others are managing, Apptivate is a great resource to dip your toes into.

Produced by live-ops vendor UserWise and hosted by Tom Hammond, Mastering Retention is another mobile game-focused podcast (it’s almost like games are big in mobile or something). Launched in summer 2020, Hammond is good at ensuring that almost every week there’s a new episode with something interesting to learn.

What’s particularly good:

Similar to Apptivate, each episode in Mastering Retention manages to be on a very specific topic that game marketers and product managers will find interesting, like game economies, optimal ad placements, building games for kids, or integrating your game with a blockchain solution.

I always love the data-driven insights from Apptopia, so it’s worth checking out Somewhat Mobile, “the show mobile app teams put on when they need to hear someone’s voice other than their manager.” It’s hosted by Adam Blacker, the “head content cook” at Apptopia. I’m sure he had a VP title at some point before he probably decided that was lame.

What’s particularly good:

Adam always asks guests to introduce themselves at the beginning of the podcast, which I usually hate because people are typically horrible at introducing themselves (too much pride, so too long, or too humble, so not long enough). But somehow, for Somewhat Mobile, it works.

The Mobile User Acquisition Show is hosted by Shamanth Rao, who also runs the Rocketship HQ agency and is a frequent guest on Singular webinars. The good thing about Shamanth is that he’s not beholden to any particular adtech vendor or network. He’s also — as an active practitioner — going to use what works, not just whatever happens to be the latest hot thing. Bringing that to the Mobile User Acquisition Show is exactly what makes it worth listening to.

What’s particularly good:

Shamanth does a great job of segmenting his podcast episodes by topic. So if you go to the podcast’s website, you can literally sort by ASO, creative, iOS 14/IDFA/SKAN stuff, and more.

Don’t tell anyone but this is Singular’s own podcast, where we chat with CEOs from companies like Unity and Zynga and InMobi, mobile marketers from Sky Mavis, Mixtiles, DraftKings, and Rovio, VPs from ad networks like ironSource, and experts like Eric Seufert and Thomas Petit.

What’s particularly good:

Besides the devilishly handsome and shockingly witty host who is worth the price of admission all on his own, Growth Masterminds dives into the biggest and toughest challenges facing mobile marketers in privacy, ATT, retention, and the evolution of the mobile space.

I’m sure I’ve missed some truly great mobile marketing podcasts. If I have, let me know. Hit me up on Twitter or via email and shoot me the details. I’ll be happy to add relevant and credible podcasts in the mobile marketing space to this list and expand the number of “top” podcasts from the very arbitrary 10 that it currently stands at.

What about mobile marketing podcasts in languages that are not English?

It might shock some people but not everyone in the world speaks English. Mobile growth marketers need insight in other languages too,

So while I can’t listen to them, here are a few podcasts to check out in other languages:

We gathered 5 mobile experts in our most recent webinar to answer that precise question. The sad truth for all mobile marketers exhausted by all the ecosystem disruption in 2022? Everything is probably going to continue to change, and likely at an accelerated rate. (Sorry!)

Those experts include:

Matej Lancaric, UA consultant

Omer Gerzon, Director of Marketing & Growth @ PlayStudios

Emre Bilgic, Apple Search Ads Client Partner @ MobileAction

Yash Patel, General Partner @ Telsta Ventures

Gadi Eliashiv, CEO and Co-founder @ Singular

All had great insights on the future of mobile marketing and user acquisition in 2023. Each sees from different angles depending on what they do and how they observe the mobile ecosystem and its challenges:

Adapting to privacy regulations and realities

Recession

Post-covid adjustments in the economy and in people’s lives

SKAN 4 and Privacy Sandbox next year

The crypto meltdown and its impact, if any, on web3

The (still happening) supply chain issues

War in Europe

Technological change in the form of Meta and VR, AR, MR

More on what to expect, and what their advice is for marketers, in a moment.

First: what mobile marketers think right now

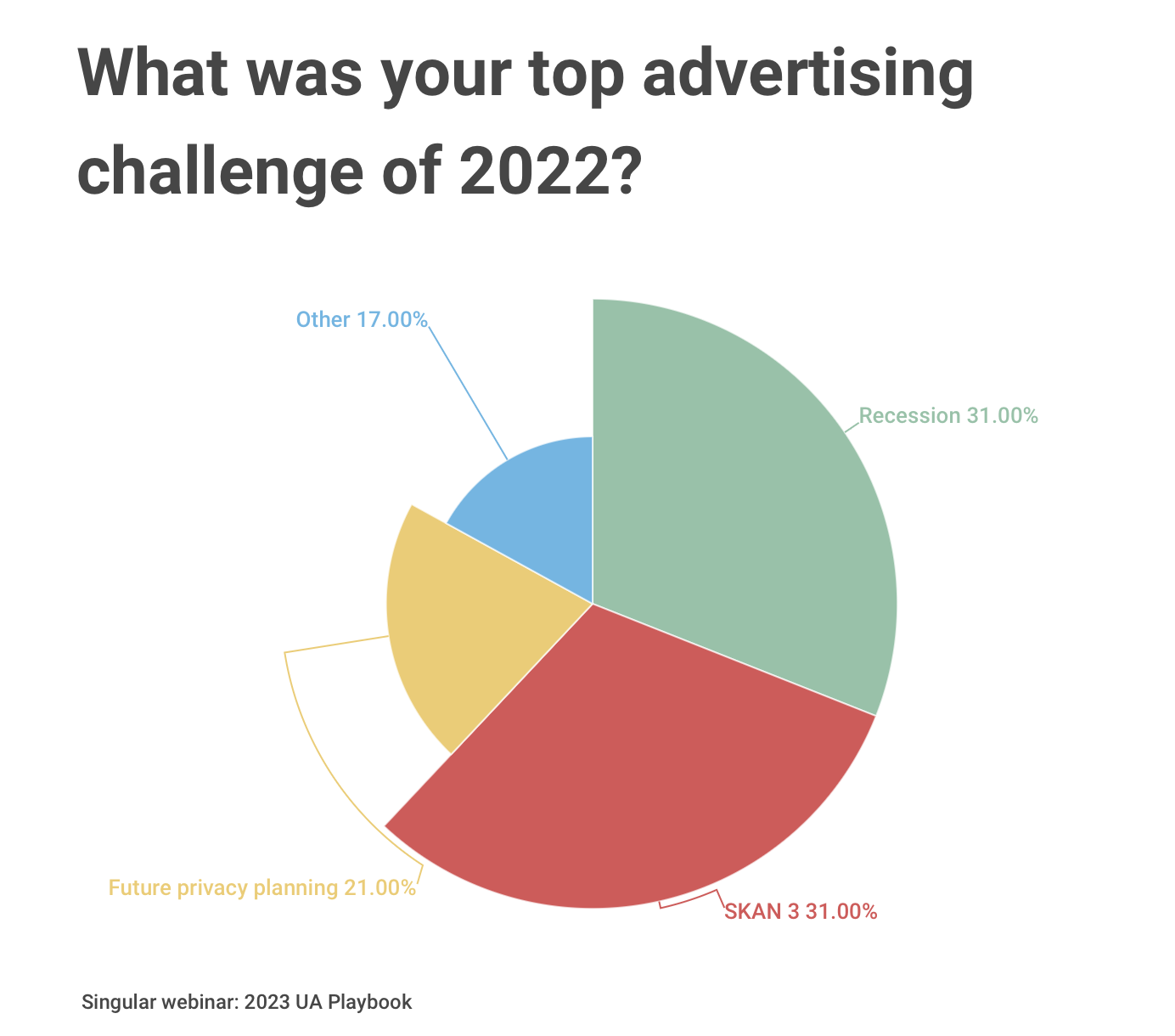

We asked the hundreds of marketers in the webinar some key questions, including what their top advertising challenge of 2022 turned out to be. The perhaps not-so-surprising answer?

Privacy.

Technically, the recession and SKAN 3 tied as the top challenges in 2022, each with 31% of the vote, while planning for future privacy changes in SKAN 4 and Privacy Sandbox for Android trailed with 21% of the vote. But let’s be real: SKAN 3 and planning for future privacy changes are both about privacy-driven changes in mobile marketing. Add them up, and you get to 52% of the vote.

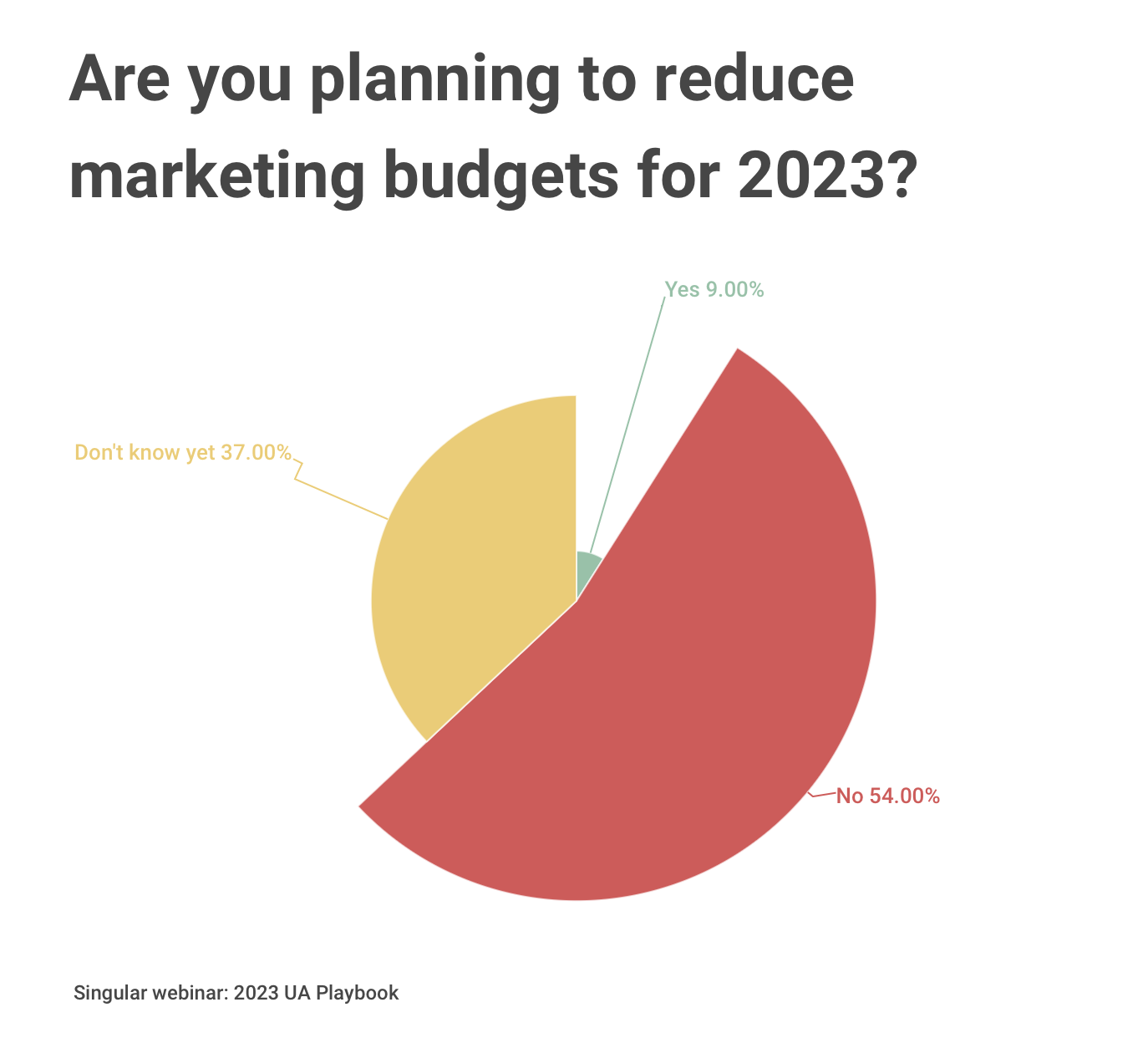

We also asked about marketing budgets for 2023.

In the current climate with plenty of talk of recession and doom and gloom, it’s easy to assume that user acquisition budgets will be down in 2023. But according to mobile marketers and what they know right now, that’s not going to be the case.

While 9% of advertisers said they’d spend less in 2023, 54% said they would not reduce marketing spend next year. 37%, however, said they simply didn’t know yet whether advertising budgets will be up or down.

Those numbers offer grounds for cautious optimism both for people in the mobile adtech space and for those who depend on advertising for mobile app monetization.

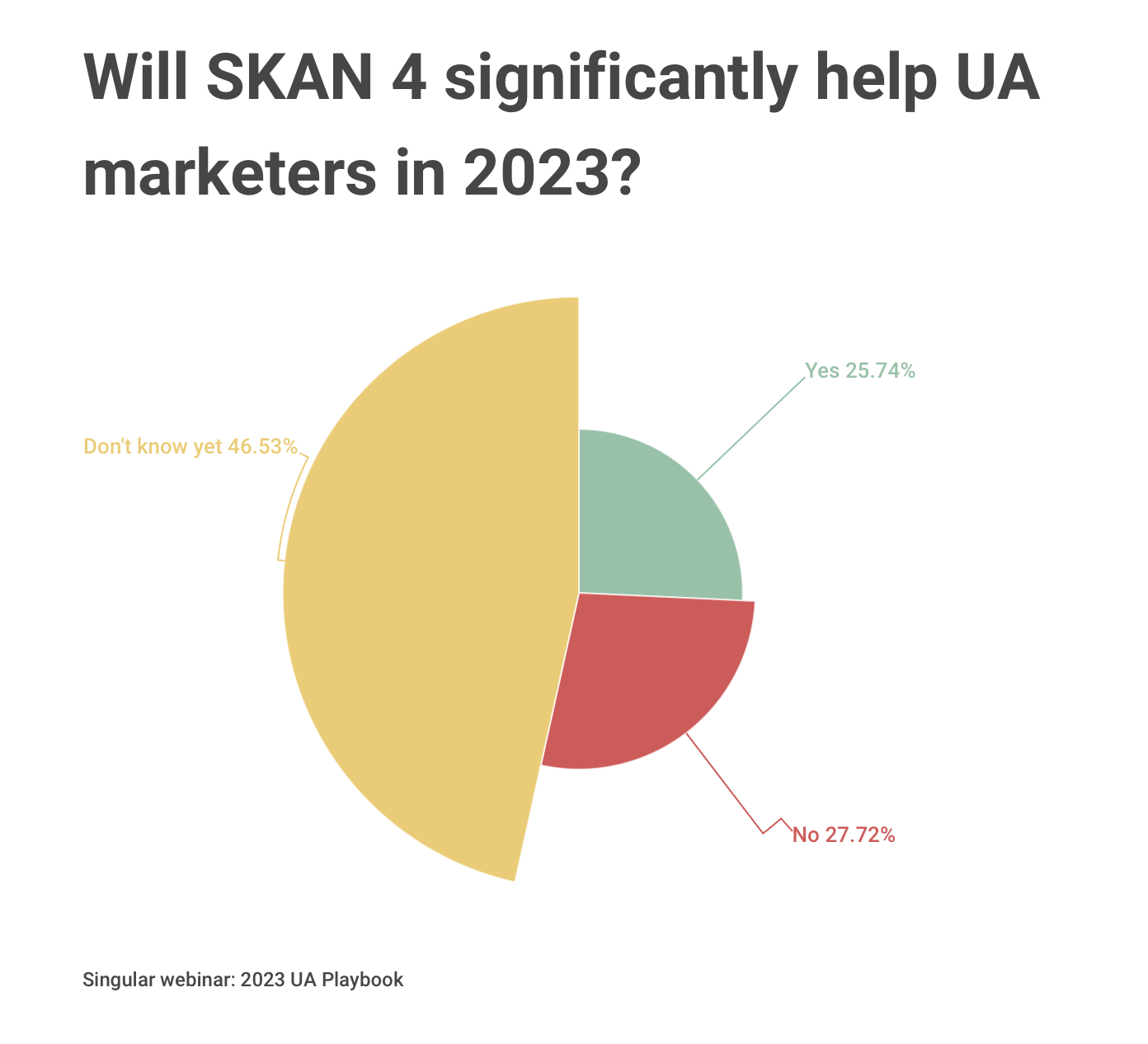

SKAN 4, of course, is a massive new release of Apple’s SKAdNetwork framework for mobile attribution, and offers new capabilities for more post-install conversion data, for web-to-app marketing journeys, and for additional creative optimization, among other things.

But marketers aren’t quite sold yet on its benefits. Or at least its cost/benefit ratio.

Only a quarter of mobile marketers think that SKAN 4 will significantly help user acquisition managers in 2023. Almost a third think it just won’t, period. And almost half simply don’t have enough information yet to decide whether it will or won’t.

Marketers just don’t know what to think yet, apparently. Which means that Apple — and marketing analytics companies like Singular — need to up their game on explaining SKAN 4 and implementing it in a way that makes it easy for marketers to adopt it and understand the benefits of it.

User acquisition 2023: what to do and what to expect

1. Go beyond D7 campaign performance

Matej Lancaric says a major mistake of 2022 to not repeat in 2023 is to view D7 performance as the holy grail of user acquisition performance.

“Not looking past D7 … is definitely dangerous and, in my opinion, definitely wrong.”

Some users take time to produce value. Some channels are better over the long term. It’s challenging when you want immediate insights — and you can certainly learn the signals of future value in each app over time — but D30, D90, and even D180 performance is really important, especially in subscription apps, and especially in high-value verticals.

2. It will no longer be OK in 2023 to lose money

It’s probably shocking to some, but there were many companies that were very comfortable losing money in early 2022. And there were also issues with the accuracy of life-time value calculations and customer acquisition cost numbers.

Why?

Free money.

“There was very fuzzy, optimistic math around LTV/CAC ratios,” says Yash Patel. “It was okay to lose money as long as these companies were growing 2X to 3X year on year because you knew you had a lot of late stage investors and equity market investors that would eventually foot the bill.”

With low interest rates and plenty of venture capital looking for companies to invest in, some companies lost discipline on acquisition cost and put rose-colored glasses on for their LTV projections. Now interest rates are higher, and VCs are much more careful.

3. Web and desktop are not dead

Mobile is where everything’s at, right? Wrong.

“We saw a lot of success with companies that launched web and desktop based experiences and saw higher retention rates and better user acquisition ROI as well,” Patel says.

The benefit of having a VC who invests in the mobile space on a webinar about user acquisition in 2023 is that you get a big picture global view. And part of the interest in web-to-app and app-to-web customer journeys and user acquisition flows is that there’s additional opportunity at sometimes-lower costs.

And, of course, not all your customer acquisition or player acquisition has to be for mobile. Some of your experiences can live on the desktop too.

4. Delaying SKAdNetwork learning and implementation will no longer be an option

Probabilistic matching is going away, says PlayStudio’s director of marketing and growth Omer Gerzon. And it will longer be a viable option to avoid learning SKAN.

“I hear a lot from other advertisers that are … saying, ‘I don’t need to deal with SKAN today. I will wait for the moment that SKAN will be forced on me,’” says Gerzon. “It’s not going to work for you. It’s just not going to work for you. SKAN is complicated. It’s complicated to understand. It’s complicated to understand how it works initially and it’s hard to run those campaigns.”

While it’s hard, some of the greatest success PlayStudios has is thanks to internal knowledge that the team has built around SKAdNetwork, Gerzon says.

And that’s becoming a competitive advantage that is more and more important.

5. Don’t underutilize Apple Search Ads

Apple Search Ads is both huge and hugely effective. We’ve always known search is a key avenue to enable relevant advertising thanks to the way it naturally surfaces intent, and doing that right where you can actually convert and install an app — and where you feel most comfortable doing so — is why ASA makes sense.

“Most marketers were underutilizing Apple Search Ads in 2022 despite all of the new placements that were coming out,” says MobileAction’s Emre Bilgic. “The biggest marketing wins for all of our partners have been utilizing the custom product pages that came out throughout the previous year … basically allowing us to match the messaging and the imagery that we have through the product search [and] just making the experience for the user more relevant.”

That improved overall tapthrough rates and conversion rates, Bilgic says. And the vast majority of marketers, he adds, have never used it. Many — 60% of the mobile marketers he’s talked to — haven’t even heard of it.

Properly utilizing custom product pages is going to be one of the biggest wins in 2023, Bilgic says.

6. Leverage the galaxy for Android wins

This might be one of the best-kept secrets in mobile marketing: use third-party app stores for big user acquisition gains in 2023.

At least, use one of them:

“The Samsung Galaxy store actually was a good way to drive Android downloads,” says Patel. “And it touches about 34% of the U.S. population.”

Do I sniff a hint of a blue ocean, a competitive backwater that avoids the hyper-competitive red ocean of Google Play and provides an opportunity for potentially cheaper Android user acquisition? Definitely something to try in 2023 for your Android apps.

7. Story-telling is the new targeting

Targeting is gone.

Whether that’s due to black boxes at Facebook or Google, or due to privacy shifts like Apple’s App Tracking Transparency or the coming Privacy Sandbox for Android, the way mobile UA marketers target users is massively changing.

PlayStudios’ marketing chief Omer Gerzon suggests story-telling is the new targeting.

“The new targeting — or actually the old targeting — is just to tell your story right because eventually, if you look at the most traditional marketing way to reach the audience that you want to reach … is just to tell your story right.”

This sounds crazy soft and brand-focused and la-ti-da for hard nosed performance marketers, maybe.

But using the right creative and messaging to ensure the right kind of users — the ones who will be high-value — notice your ad and install your app is genius. It’s a mix of using whatever targeting you can by channel, partner, and context, and then applying a mass marketing strategy to narrowcast to specific audiences within the crowd.

8. Events are the new targeting

Stories are great, and they work. To optimize ad campaigns in real-time, you also need signals. Matej Lancaric suggests those are events.

“I think we are moving … towards event-based targeting: event meaning anything that you can actually capture from your game and then send back to the UA channels … the first 24 hours for you to maximize the number of events you can actually get and capture from your players … and then send it back to UA channels and then optimize your campaigns based on those events, that is basically the new targeting. It’s going to happen. It’s already happening to a certain extent.”

In other words, bring in users.

See what key events happen: events that signal monetization. Send those back to user acquisition partners. Tell them you want more like that, and let them sort out how to find and get them.

Targeting, circa 2023.

9. Look deeper into your funnel

Gerzon essentially agrees with Lancaric on going beyond D7. In fact, he thinks that going deeper is going to be one of the major changes to user acquisition in 2023.

“The main change for most advertisers is going to be the ones that are more looking at deeper funnel events or optimization,” Gerzon says.

In other words, drop the clickbait ads. Ignore easy top-funnel wins like CPI or install rate. Focus on engagement and retention and all the things that happen deep down in the funnel. And really work with product to optimize user experience and onboarding.

10. Grab more granularity

We lost the age of granularity when the IDFA walked out, right? Sure, but not so fast …

“The good news is that next year with SKAN4, at least in theory, you should be able to get more granularity on your down funnel events,” says Singular’s CEO Gadi Eliashiv. “More granularity is good news.”

Learning SKAN 3 now is smart, because it sets you up better for SKAN 4. And deeply understanding how to use SKAN 4 will optimize the amount of insight you can derive from user acquisition campaigns.

The other good news: the mobile ecosystem is coming to your help.

“There’s probably 1,000 people in Meta working on optimizing their ads engine because it’s the biggest revenue driver,” Eliashiv says. “They’ll find ways to use those bits that will make their way to advertisers.”

And not just Meta.

Google as well, and all the other titans of adtech that you might partner with.

11. Embrace multiple measurement methodologies

Mobile marketers might be able to get some of their missing granularity back. But what’s not coming back is the sole reliance on IDFA for ROI, LTV, CAC, optimization, retargeting, and basically everything else in mobile marketing on iOS. And GAID on Android is going the way of the dodo as well.

“Now you need multiple methodologies to understand what’s going on,” Eliashiv says. “You’ll find yourself where you’re not just using one method anymore. It’s gonna be a combination of tools that you use for different purposes.”

And, of course, the frameworks from major platform owners:

“Buckle up for SKAN 4.0 and Google Sandbox and the privacy changes,” Gerzon says. “This is the future of measurement. Don’t be afraid of it. Just embrace it and start working on it if you haven’t. All the traditional targeting and measurement is going to fade away.”

12. Embrace generative AI for mobile marketing

What are the biggest game changers going to be for mobile marketers in 2023?

One just might be generative AI, says Patel.

What for?

Testing, images, ads … pretty much everything.

“Using generative AI to scale AB testing in terms of creatives and ad performance across a whole bunch of channels,” will be a major difference maker, he says.

So go get your Stable Diffusion, your ChatGPT, your MidJourney, and all the other tools. And expect some generative AI startups that are laser-focused on delivering the benefits of these tools specifically in a marketing and advertising context.

So much more in the full webinar

As usual, I can only excerpt a few fragments of the value in a full webinar in a recap post. Go check out the full on-demand webinar here to get all the insights from the experts we assembled.

If you’re taking some time off around the end of year holidays, this is a perfect time to cue it up, grab a drink and a snack, and chill out to enjoy the show.

What changes in a world with third party app stores on iOS?

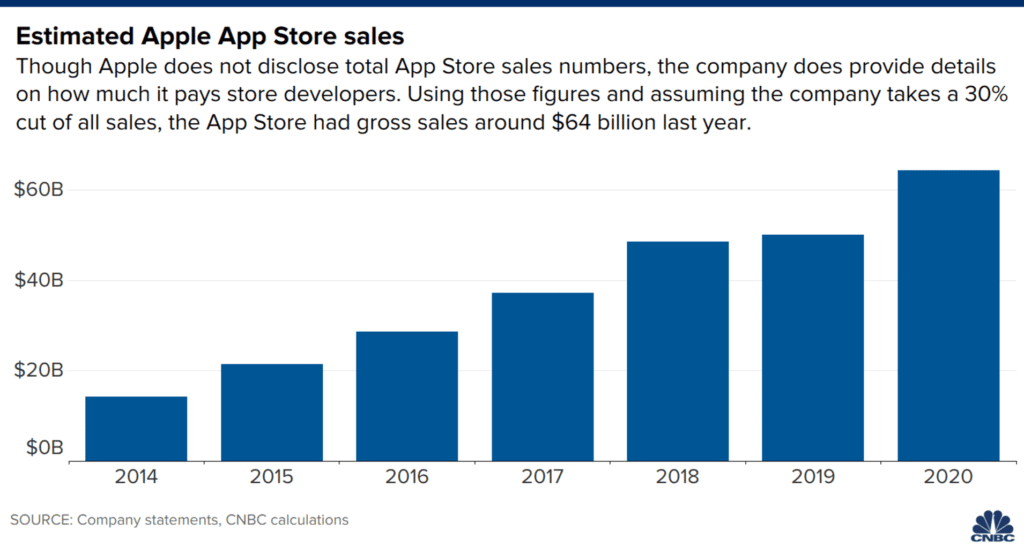

We’re seeing multiple news reports that Apple is planning for a future with third-party app stores for iPhone and iPad apps. We predicted this back in early July because the EU’s Digital Markets Act essentially requires it. It would be the biggest change on iOS since Apple launched the original App Store, and it would put at risk Apple revenue of $64 billion in 2021 alone, and perhaps $300 billion over the past 8 years.

But what does it change in the mobile marketing ecosystem?

Pretty much everything.

Estimated App Store revenue, by CNBC

Potentially, a multi-app-store world on iOS changes almost everything about mobile marketing. Here’s a short list of things to be thinking about as we prepare for a world in which the only way to get an app onto an iPhone is NOT the official Apple-owned App Store.

1. Will there be third-party app stores in the EU only, or in the whole world?

The impetus for the expansion to third-party app stores is clearly from the European Union’s new Digital Markets Act, so if and when Apple allows third-party app stores to exist, you have to believe that they will launch first in the EU.

But …

When the United States sees third-party app stores for iOS apps in Europe, it’s hard to imagine government officials — and people — not wanting the same privilege. And I think the same goes for basically every country in the world.

So, Apple may just bow to the inevitable and make a new third-party app store policy globally, or may force countries to fight for the right one by one, or region by region. Either way, it’s likely to happen everywhere eventually.

2. Will Apple still charge fees for apps installed via third-party app stores?

The Netherlands has already legally required Apple to allow apps to run their own payment processing systems. (This is no small task, by the way, requiring a full e-commerce infrastructure with the ability to handle currencies, refunds, security for credit card numbers, taxes, coupons, and more.)

But while app developers probably thought that doing so would enable them to avoid Apple’s 30% cut on most digital sales in their apps, Apple has so far had the last laugh.

Why?

Apple still requires a 27% fee on transactions that apps processed themselves:

“Consistent with the interim relief ruling of the Rotterdam district court, dating apps that are granted an entitlement to link out or use a third-party in-app payment provider will pay Apple a commission on transactions. Apple will reduce its commission by 3% on the price paid by the user, net of value-added taxes.”

Oh, and you have to report all sales to Apple weekly within 15 calendar days following the end of Apple’s fiscal week, and remit Apple’s commission within 45 days.

Plus, “in the future, if Apple develops technical solutions to facilitate reporting, developers will be required to adopt such technologies.” And, Apple has audit rights on your app. Fail to pay, and Apple can remove your app from the App Store.

So it’s a valid question: would Apple still charge fees even if the actual download and install process is now being handled by a third-party app store?

3. Will Apple drop the fees on the official App Store to compete?

Imagine this scenario:

Apple enables third-party app stores

Everyone goes nuts building app stores, shouting FREEDOM and anticipating huge paydays

Apple drops commission fees on most digital sales to 15%

Developers vote with their feet and stick with easy, pocketing the extra 15%

Competition creates competitiveness.

And if Apple is forced to compete in third-party app stores, it’s not hard to imagine that they might just shave their fees a bit to retain revenue, block the path to break-even by third-party app stores, and — importantly — keep all the user intelligence on purchase behavior.

(Which is essential, don’t forget, to the competitive advantage its growing Apple Search Ads ad network depends on, and which it could expand to multiple other verticals, including podcast ads, where Apple owns significant advantages.)

4. Why have app stores at all?

We’re very used to app stores today, thanks to Apple’s iPhone and Google’s Android ecosystem designs.

But we did without app stores for 3 to 4 decades in the packaged software world, where any store could sell any software on disk, CD, or DVD. And we did without app stores for easily 2 decades in the internet age, when any website or FTP server could offer software for downloading.

Today, for example, I can download an app from a software publisher’s website to my Mac, install it while clicking yes on a bunch of scary-ish warning screens from Apple, and use it in 5 minutes.

Theoretically, this would be completely possible on an iPhone as well: it’s a computer, it has storage, it can download files, it can install programs. App stores are conveniences, not necessities.

5. App Store-as-a-Service: will Apple completely reinvent itself and try something truly innovative?

OK, this is wild, so bear with me.

What if Apple reframed all of the features that make up the App Store experience as services, and made them available via API? In other words, third-party app stores could compete by saying apps are “Apple reviewed,” “Apple Approved,” “compatible with Apple Pay,” and so on. Even app ratings and reviews could be served from the App Store, and aggregated from all app stores, resulting in a better shopping experience for users.

Apple could make official app store reviews available at the cost of a few percent of fees, make payment processing available at another level of cost, and so on. Apple would still see and review all the apps installed by app stores that used these services, but each app store would have the ability to offer only what it wished.

What this would enable is a multiplicity of app store experiences and price points, but all with the same level of trustworthiness.

Not all third-party app stores would choose to participate in this option, but many might.

Now imagine if Apple went a step further and offered a no-code way to make app stores like this that it would then conveniently host on the App Store itself. Fred next door could offer an app store. So could your grandad. Gertrude’s Apps for People Who Knit could live next to Franklin’s Apps for Hiking Enthusiasts, not too far away from curated selections by the internet’s biggest influencers and Hollywood’s top celebrities.

Unlikely, I admit, but this would be a truly Art of War response to the current third-party app store legislation.

6. Will Apple be forced to host third-party app stores?

Allowing third-party app stores is one thing. Making them available and easy to access is quite another.

If Apple was forced to offer third-party app stores on its own App Store, they’d be easy to add to your iOS experience and easy to test, dabble with, and maybe get hooked on. That would be bad, most likely, from Apple’s point of view.

So third-party app stores are most likely going to need to be sideloaded, either via some new download process or perhaps by connecting to a laptop, going through a process, and clicking through a series of scary-looking dialog boxes.

More friction equals less adoption.

7. App Tracking Transparency enforcement implications: will Apple lose its power to enforce privacy regulations?

ATT is how Apple …

Wrested more control of app discovery from Facebook and other players while

Playing a massive global privacy card, and

Enhancing customer trust ahead of a not-too-distant release of a augmented reality/metaverse project that will put cameras on our eyes

App Tracking Transparency is currently enforced via App Store review processes, and violations are punishable by either refusal to release new app updates, or potentially the nuclear option: complete removal from the App Store, the only place Apple customers can get apps at all.

With multiple app stores, Apple either …

Loses control of the iPhone privacy story completely, or

Weaponizes privacy in a battle to retain customers’ app install/download/payments business, or

Moves enforcement of tracking to another software layer, perhaps in the iOS networking code

Each option has positives and negatives from Apple’s perspective, but option 3 is most likely.

A related question: how will access to device identifiers change? Apple controls how apps get to see the IDFAs and other device identifiers now; will this continue in a post single App Store future?

8. What happens to SKAdNetwork, Apple’s mobile attribution framework?

SKAdNetwork is a software framework in iOS that enables privacy-safe attribution of marketing efforts to results. In other words, it helps marketers figure out what ads and campaigns worked, and which didn’t, while not revealing personal information of people who see ads and install apps.

(Many marketers might argue it doesn’t do a very good job, but that’s a story for another day. If this is you, by the way, you need Singular’s SKAN Advanced Analytics, which gets you more and better data for calculating ROAS, measuring cohorts, and optimizing campaigns.)

But SKAN operates in a complex relationship between apps and iOS and the App Store (plus advertisers, ad networks, and measurement companies like Singular). What happens when there are multiple app stores? Will SKAN be implemented by other app stores? Would app developers build in calls to SKAN in apps on third-party app stores? Why would they?

9. What privileges and restrictions will third-party app stores have?

Will third-party app stores on iOS have the same privileges and capabilities as the original App Store? Or, as seems more likely, will they have limited control over how they act?

Today, the App Store offers access to millions of apps. Find one, tap to install, and you’ve got it. But the App Store is also involved in ongoing payments that requires integration with individual apps for in-app payments, subscriptions, and more. And the App Store is also instrumental in keeping apps updated regularly.

How will third-party app stores integrate with apps for ongoing monetization capabilities? And will they notify people when apps have updates to install, or will Apple allow background access to update apps automatically when there are updates, like the App Store does now?

10. What happens to the app review process?

Currently, Apple reviews each app that makes it on to the Apple App Store. There’s a human review, but there’s also an automated code-level review. The process isn’t perfect, and mistakes do happen, but the end result has proved to be pretty good: most apps are trustworthy, most apps don’t take advantage of users, and most bad actors are caught fairly quickly.

How will third-party app stores police what goes on their virtual shelves?

Probably in similar ways that today’s third-party Android app stores do, which means varying levels of scrutiny, technical capability, and due diligence. And that leads to what Apple will no doubt play up fairly loud: extra risk for users.

There will be malware. We’ve seen it on the Android side.

11. What privileges will apps downloaded from third-party app stores require?

Apple carefully controls how much data apps can access. Apple requires apps to ask permission for access to photos, to location data, to the camera, to the microphone. All of that should still work, because it’s an interplay between apps and the iOS operating system, which is secure by design.

But what if apps on third-party app stores say things like: allow IDFA sharing if you want to play the game? Or, give access to location in order to get the coupon? Or, let me access the clipboard to see what’s just been copied?

Or, worse, let me see keystrokes?

Or, let me continue to operate with all my permissions in the background while you’re in others apps?

Apple polices manipulative quid-pro-quos and other security nightmares like that via App Store submission guidelines and app reviews, but some third-party app stores are incredibly unlikely to do so. The result is very likely to be not only a reduction in privacy for iPhone and iPad users, but also significant breaches and attacks on people’s financial accounts or other areas of their lives.

Here’s the reality: we are all stupid about privacy. Some of us generally and often, some of us very occasionally. But we want what we want when we want it, and if we think this one app will provide it right now, we sometimes make foolish decisions.

12. Will every big publisher become its own app store … will Netflix, for instance, become an app store for its games?

Depending on how this all plays out and what is possible at what price, the temptation will be there for big publishers like Rovio or EA or Activision or Disney or Ubisoft or Gameloft to simply be their own app store and distribute their own games on their own platform.

Imagine that: set your own rules, manage your own fate, cross-promote however you wish, share resources between games — so web3 friendly — create a publisher-centric wallet for use in all apps and games from you as a publisher … the sky is the limit.

Also, will every big brand consider whether it should offer its own app store?

The Nike app store

The Coke app store

The Cadillac app store

We know there’s going to be an Epic app store …

And you also know that the second it can, Facebook will create its own branded app store, as will Google. And they have truly massive platforms to promote their own stores.

Plus, don’t count out the big ad networks:

Unity

ironSource

Liftoff

AppLovin

These titans of adtech make their living promoting app install campaigns. Imagine what they could do with more data on actual installs and more insight into conversions and just more revenue period by owning their own app stores.

More on this in the coming weeks …

13. Will Stripe offer a mobile app payments layer to abstract all the complexity for apps and app stores?

Payments are hard. Doing refunds sucks. Managing multiple currencies is a PITA. Taking into account taxation rates and rules in 200 countries is not fun.

None of these things are in the core competency of mobile gaming companies, nor in the competency of many other mobile apps in virtually any verticals.

Stripe famously offers payment infrastructure for the internet, but basically it’s for the web. Would Stripe — or similar companies — come in and offer a mobile-centric payments-as-a-service for mobile apps that they can just plug into and use without thinking or worrying about it?

Probably!

14. Content implications: who will police porn, violence, racist material?

Right now the Apple App Store review process checks what kinds of content an app offers, and Apple will decline to host and provide apps that offer full-on porn or other kinds of content, including hard-core racist ideology and so on.

What happens in a third-party app store world? Can the Aryan Nation set up an app store for content they approve? Will we have porn-focused app stores? Gambling-focused app stores? App stores focusing on the worst kinds of violent behavior?