John Koetsier is a journalist and analyst. He's a senior contributor at Forbes and hosts our Growth Masterminds podcast as well as the TechFirst podcast. At Singular, he serves as VP, Insights.

France fined Apple $150 million euros over App Tracking Transparency. That might be the start of major changes to how Apple employs ATT in the future in France, in the EU — where 26 other countries will instantly see a major revenue opportunity — and maybe even globally.

Spoiler alert:

Everyone in mobile growth is hoping ATT will go away. That is … unlikely.

But it could change significantly. Keep reading …

Why France fined Apple: “neither necessary nor proportionate”

Apple’s goal with App Tracking Transparency is not the problem, says France. France fined Apple, but not for giving people more control over their privacy. That’s generally a good thing.

The problem is the way it privileges Apple and punishes third-party developers, especially smaller ones.

“The introduction of the framework led to multiple consent pop-ups being displayed, making the use of third-party applications in the iOS environment excessively complex,” says France’s antitrust watchdog. “How ATT is implemented is neither necessary for nor proportionate with Apple’s stated objective of protecting personal data.”

ATT is only for third-party apps.

The reason is that Apple sees all iPhone and iPad owners as its own customers. In other words, their data is first-party to Apple, and there’s implicit consent for Apple to store and use data people use, share, or create in Apple-owned apps for multiple purposes … including targeting for ads in Apple Search Ads.

“Ads delivered by Apple may appear in the App Store, Apple News, and Stocks. These ads don’t access data from any other apps. In the App Store and Apple News, your search and download history may be used to serve you relevant search ads. In Apple News and Stocks, ads are served based partly on what you read or follow.”

Currently Apple limits contextual data collection for ad targeting to 3 apps. Conceivably, that could change in the future.

The problem is that under ATT, third-party apps had multiple privacy hoops to jump through, rather than just 1. Where Apple’s first-party apps could instantly ask for location, or access to other features, or data-sharing, third-party apps had those pop-ups to navigate in addition to App Tracking Transparency.

“The implementation methods artificially complicate the use of third-party apps and distort the neutrality of the framework. Small publishers financed by advertising are disadvantaged.”

That variance made ATT anti-competitive, according to France, and therefore illegal given Apple’s size and market share.

Another reason France fined Apple: ATT’s construction is ‘non-neutral’

There’s another problem with ATT, according to France, and it’s yet another key reason why France fined Apple.

The issue: App Tracking Transparency is constructed to limit acceptance and privilege denial by design.

To deny app tracking authorization, users simply need to say No in the initial prompt. In other to accept personalized advertising, people need to say yes to the initial prompt (#1 above) and yes to the full-screen explanation of ATT (#2 above).

Small changes in design could have fixed this, France says.

France: ATT could easily be integrated with GDPR and local privacy laws

France’s competition office not only said ATT was anti-competitive. It also said that Apple could “easily” integrate ATT with GDPR and help app makers meet their legal obligations at the same time as their platform obligations.

First off, France says that ATT does NOT by itself bring app publishers into compliance with GDPR out of the box … something that we’ve recently learned not all app publishers fully understand. To actually comply, publishers generally have to add a CMP (consent management platform), which makes for multiple pop-ups, general user annoyance, and all-round confusion.

A few changes, however, could have integrated GDPR and ATT:

“The ATT framework could easily, subject to a few modifications, also be used to collect the consents required by French law and the GDPR,” says French sister agency CNIL, the country’s data protection authority. “Making publishers systematically collect user consent twice for the same purpose constitutes an unnecessary and artificial complexity.”

In other words, CNIL is saying, Apple could have shown a single, unified prompt for everything: ATT acceptance, GDPR compliance, and authorization for Apple to use iPhone owners’ data for its own ad network. And that would have changed everything that led up to our current situation under which France fined Apple.

Something like this could have worked:

“This iPhone and apps on it may use your activity across Apple apps and other apps to personalize ads. Do you agree?”

Then, Apple could have provided clear yes/no options that in 1 simple step:

Cover both Apple’s ad tracking and third-party tracking together

Satisfy GDPR’s “freely given, specific, informed, and unambiguous” consent requirement

The implication, of course, is that Apple didn’t do this because Apple distinguishes between its own ad platform (which uses first-party data and — in truth — is particularly privacy-respecting) and third-party tracking. Plus, Apple likely feels that its ad targeting uses first-party data in a way that doesn’t require the same kind of consent under its interpretation of GDPR.

We all knew this right? So now what?

None of this is really a shock to anyone who has been paying attention in mobile marketing and advertising for the last few years.

The difference is that now you have a respected, influential, and powerful national organization saying what marketers have been saying: ATT is constructed in a way that confuses and scares users, makes life harder for third-party app publishers, and privileges Apple.

The question is: will it change anything?

Apple is likely to appeal as a matter of course, but is probably unlikely to win. France fined Apple to started this process, but every other EU country is likely to see this as an opportunity to do something similar … and extract some hundreds of millions of dollars from a big American tech company.

So France is likely just the start.

What can Apple do to avoid additional payments to the 26 other countries in the European Union?

Follow CNIL’s advice and merge ATT and GDPR, at least in the EU.

And, maybe, get ahead of the problem and do something similar globally, for every jurisdiction, to comply with local privacy laws and avoid adding a layer of challenging, difficult-to-understand pop-ups and settings just for Apple.

If Apple can find a way to do that while retaining its incredibly important image as a paragon of privacy, it may just do that.

Mobile app retargeting is a huge part of engagement, monetization, and retention for top apps, especially in categories like shopping, travel, and gaming. What could we learn about mobile app retargeting from a travel app with 100 million monthly average users?

I recently had a chance to find out.

The travel app is Ixigo, a booking app in India and elsewhere. I spoke to Ixigo’s senior manager for growth, Subhadeep Chakraborty, on a recent Growth Masterminds podcast.

We talked about:

Retargeting’s critical role in Ixigo’s business (and yours!)

The essential channels for retargeting that we never talk about

Why it’s so essential to have multi-platform users

How smart segmentation is the foundation of successful retargeting

How to to use behavior-based triggers intelligently

Determining the optimum wait time before retargeting

How important personalization is to retargeting

The mobile app retargeting waterfall: what to do when

Retention as a rewards strategy

How the best retargeting is free

And much more …

Watch the interview

Hit play, keep scrolling …

10 critical mobile app retargeting insights

1. Return opens and visits are crucial

30% of people who search for a ticket on Ixigo but don’t buy come back the next day. That’s another chance to deliver value and another chance to monetize, and it’s critical to Ixigo’s revenue and growth, says Chakraborty.

“ It’s not always that the customer couldn’t find value in the platform, but it might be different external factors,” says Chakraborty. “It’s our job to bring back the right set of users back to the platform so that they can complete the expected action.”

Subtract that return and retention factor, and monetization takes a massive hit. Build it in, and it’s a huge factor in overall business success.

2. Mobile app retargeting isn’t just about retargeting ad networks

Retargeting has been tough on iOS ever since App Tracking Transparency: there’s way fewer IDFAs to collect, jam into an audience, and shoot over to an ad network.

But the good news is that there are so many organic and owned means of retargeting. And it turns out those are the ones Ixigo leans on most.

Email

Push notifications

WhatsApp

The good news is that all of these are essentially free. But they do require a different focus during onboarding …

3. Multi-platform users make mobile app retargeting SO MUCH EASIER (and cheaper)

If you know nothing about your user but their GAID, some standard account info, and maybe a bit of app activity, retargeting takes a lot of cold hard cash.

But if you got an email address, a WhatsApp number, or some other communication-friendly PII in your app onboarding process, you’ve made that user/customer/player a multi-platform user. You have multiple means to communicate with that person on multiple platforms.

That makes this user far more valuable, and far more likely to engage and retain and monetize.

“ Whenever we are reaching out to the customers using the different paid channels, I believe that the customer is already out of reach,” says Chakraborty.

Ouch.

In other words, if you have to spend, you’ve already failed to some extent. (Counterpoint: yeah there are some caveats here. And yes, paid retargeting is not a bad thing in all cases, as you’ll see later.)

4. Smart segmentation is the foundation of mobile app retargeting

Retargeting that works is personalized based on what people want. In Ixigo’s case, this might be a flight, a train ticket, or a hotel room. To make that work, you need the right tech to immediately put users into audiences based on in-app actions, and then be able to take appropriate action.

You can roll your own or use a tool; Ixigo uses CleverTap.

Using the right tool doesn’t just enable smart segmentation, it also manages message orchestration across platforms. A good platform learns which ones work, which ones specific people respond on, what times they will see messages versus ignore them, and so on.

5. You have to use behavior-based triggers intelligently

If someone searches for a flight, you don’t just retarget based on flights.

You use a bit more intelligence.

“Let’s say that the customer was searching for a flight from a certain A city to B route,” says Chakraborty. “We would definitely add that to our copy, and we would also personalize even more.”

That “more” includes price changes, but it doesn’t end there.

It might also include different options on other airlines, or slightly different departure and arrival dates that might save money or be a quicker journey with fewer stops. Or a better package with a hotel stay or a car included.

And, of course, you get the user right where they need to be ASAP:

“We would also send a dynamic deep link so as to land the user back to the page from where he or she has dropped, so that they can very easily continue with the journey and complete the process, because it never makes sense to land the user back on the homepage.”

And yet … it happens. It’s happened to me in recent memory.

Also, perhaps counterintuitively, mobile app retargeting messages should not be just about pricing … even in a massively price-sensitive market like India:

“The first message is never about the offer because we don’t believe that offering just [better]prices to our customers is going to help them,” says Chakraborty. “It’s about personalizing the message for the user … and the timing.”

Which is a good segue …

6. The optimum wait time before retargeting varies … and matters

In most cases, the optimum wait time is not instant.

The first thing to think about when deciding how long to wait to retarget is not the offer or the event that triggered the retargeting opportunity.

It’s the customer, Chakraborty says, and the purchase.

So if the purchase could be cheaper in a day or two — not unknown in the flight industry — it’s better to retarget them later, when you have that infomation. And if someone is looking for a vacation, you have more time to allow their intention to solidify. Whereas if they’re looking at train tickets or any more immediate purchase, you need to execute your retargeting effort quicker.

It’s also about natural time frames for specific kinds of transactions.

Ixigo avoids bombarding users immediately after drop-off.

Instead, the company uses historical funnel data to determine how long the average customer takes to complete a booking. For example, if flight searches usually convert within three hours, Exigo gives that window for organic conversion before sending a message.

7. Personalization is critical in mobile app retargeting

It’s not just: complete your purchase, here’s a link.

Instead, it’s specific travel routes, price drops, and dynamic deep links back to the point of drop-off. And the specific names of the cities that the user was researching, along with routes and carrier companies.

The more personal, the more impactful.

8. The mobile app retargeting waterfall will save you money

Exigo’s approach to outreach is structured like a waterfall. It starts with low-cost, high-personalization channels and gradually moves toward paid options:

Email Email offers the most space and scope for detailed messages with personalization. This is a primary channel when available.

Push notifications & WhatsApp Push notifications and WhatsApp messages are good, more immediate follow-ups if email doesn’t deliver. They are both cost-effective and timely, while offering less scope for detail and content.

Paid ads Ixigo only uses paid ads after their organic CRM-based options are exhausted. These ads intentionally exclude recent search data to avoid conflicting with CRM outreach.

This channel prioritization helps Chakraborty maximize cost efficiency while maintaining user experience quality. It also reflects a broader philosophy: the users who’ve already downloaded your app or created an account shouldn’t require paid reacquisition.

9. Retention and loyalty programs: it’s rewarding to reward

Retention curves for Ixigo improve after 3 months, so if they can nudge new users toward long-term habit formation by incentivizing repeated usage, it’s generally a good thing. So Ixigo uses Ixigo Money to reward people who complete certain booking milestones over 3 consecutive months to get them to that place.

The equivalent for your app or service might be different: you’ll learn that by looking at cohort behavior over time.

Once you do, whatever you can do to incentivize users to act like those cohorts or users who retain will improve engagement, retention, and ultimately monetization.

Reward-based retention is a strategic long-term play. It’s not just about activating or reactivating users, but encouraging habit-driven behavior through meaningful incentives that build life-long customers.

Much more on mobile app retention in the full podcast …

Cross-device retention is now a standard part of Singular’s cross-device attribution solution and available to all Singular customers. It’s an essential part of fully understanding your ROAS, LTV, and customer journey.

Cross-device retention: so many devices

The average US household has over 17 connected devices. I personally calculated my own number at north of 50 about a year ago, though I’m probably an outlier. In 5 years, the number of devices owned by the average American jumped 63%, and the average European 68%.

That’s tablets, phones, smart TVs, and yes … good old-fashioned laptops and PCs.

Not shockingly, we use a lot of those devices.

Two thirds of shoppers use multiple devices in succession while considering online purchases and 40% of online transactions involve multiple devices. I know I like to see products on a bigger screen even if I’m mid-transaction with my phone.

And even when that web2app journey happens on the very same device, you need marketing connective tissue like deep links and cross-device attribution to connect all the dots, fully understand user journeys, and be able to accurately calculate ROAS, LTV, and retention.

The cross-device scenario you see every day

Cross-device retention gives you better insight on what’s actually happening. Because this is a fairly common scenario:

You acquire a new user on the web on PC (or console, or CTV)

At some point, they start using your mobile app

Around the same time, their web/PC use drops off

Your analytics goes \_(ツ)_/

In a legacy attribution solution, something bad happened. According to an old-school marketing measurement solution, you acquired a user who stayed for a while and then churned … maybe even before generating enough revenue to cover your customer acquisition cost.

In that same legacy scenario, a totally new organic user magically popped up in your app.

With cross-device retention, you know much better.

With cross-device retention, you know that you did a great job of acquiring that new user, customer, or player on the web. And that you did a great job of making that person a multi-platform user: someone you can engage with and provide services for via multiple channels. You also know that the CAC for the initial acquisition wasn’t wasted, but is actually being continually monetized on an ongoing basis on a new platform.

Which makes your ROAS and LTV numbers look better and be more accurate at the very same time: a very nice combination.

Plus, as an extra cherry on top, both of those newly-more-accurate metrics now provide better insight into smarter campaign optimization for the future.

Win, win, win.

How Singular’s cross-device retention works

Singular’s cross-device retention works at the user level, not the device level. It counts users across different devices, and calculates retained users across all the different devices they use. Singular then calculates your retention rate as retained users devices by total conversions in your campaigns.

Simple, obvious, expected?

Sure, but it requires the magic of cross-device retention to function.

Both retained users and your more accurate cross-device retention rate are cohorted metrics, so you see them in a cohort view by campaign.

Every Singular client who is using cross-device attribution has immediate access to this feature, and the data is retroactive to March 20.

In other words, it’s simple, built-in, on by default, and available to all right now.

Cross-device retention: essential for marketers

Of course your back-end systems ultimately have the best insight on what happened: a user onboarded in 1 platform and transitioned to another, and maybe bounces around a bit here and there between devices.

But without cross-device retention, your marketing and advertising analytics don’t.

That’s a problem, because you’ll never have accurate ROAS or LTV. You’ll never see the full customer journey, and you’ll have bad data driving future optimization decisions. That means it’s more likely that you’ll accidentally optimize the wrong campaigns for the wrong reasons, and maybe even drop channels that are actually profitable but don’t appear that way in your analytics.

Cross-device retention ensures that your marketing analytics more accurately reflect your product and user reality, regardless of exactly how people choose to use your product, where they decide to onboard, or how you managed to attract them in the first place.

Ultimately, it’s 1 less thing for you to worry about, and it’s better data for everything you do.

Mobile game monetization is hard. Very hard. Almost 2,000 apps are published every day to Google Play and the iOS App Store. Hundreds more are published on third-party app stores in China and elsewhere. If only 10% of them are games, that’s well over 200 games being published every single day.

Think 6,000 a month. 73,000 a year.

Plus the hundreds of thousands of already existing games on app stores around the world. And the 10s of thousands more that generative AI could add. Imagine a pre-schooler literally prompting a game via ChatGPT, for example, or making a game entirely by voice, which Roblox chief scientist Morgan McGuire told me isn’t too far off …

Last I checked, there’s only 10 games in the top 10. The top games list is incredibly exclusive, with the top 1% of games making maybe 90% of the money. And only a tiny percentage of games are actually profitable. (I’ve heard 2-3%, but don’t have hard data on this very depressing statistic.)

The key question about mobile game monetization:

How is your game going to be 1 of the very few that win?

We recently chatted with ad monetization expert Felix Braberg for our Hack Gaming Growth miniseries. There are tons of insights in the whole miniseries from experts like Matej Lancaric, Jesse Lempiäinen from Geeklab, Günay Azer from Gamelight, and others, plus Braberg himself, of course.

Our topic with Felix?

Monetization. Specifically, ads-based monetization, which is his speciality.

And that’s where he shared the 1 thing that differentiates games that win from games that fail.

Mobile game monetization: 1 key differentiator between winners & losers

Leadership should begin at the top, and so should product vision. People who know and understand mobile game monetization tend to be vastly superior at creating games that win.

And that’s the key difference between game publishers that win and those who build games that bleed cash, say Felix.

“ The best studios are the ones where the people who are calling the shots also know what they’re getting paid on the other side,” says Braberg. “That’s what I see as the biggest disconnect between people who have games that fail and who succeed. If a CEO or a product leader knows how much you actually get for an interstitial impression in non-U.S. geos and how much you get for one in the U.S. geos, you can start to design a gameplay around that.”

In other words, successful game studios build monetization at the very same time they’re building their game. They know how much revenue they can get. And they’re not bolting on an off-the-shelf monetization strategy at the end: they’re designing gameplay, levels, durations, challenges, and solutions around monetization.

That includes fun. But it also includes pain.

Elad Levy, who sold a game to Playtika and served as the CTO for the company’s massive social casino game House of Fun, once told me both pleasure and pain are essential to creating a great game. And they’re both also essential for creating a great game economy … AKA something a publisher can monetize.

“That’s the art of building a great economy and game progression systems … it’s a balance between pleasure and frustration,” he said. “Those are the most successful games. Sometimes you’re super happy. Sometimes you want to throw the phone out the window, but that balance between pleasure and frustration, that is what builds amazing games.”

Happiness keeps players in the game and keeps them coming back: usage, engagement, retention.

Frustration gives them something to work on, fix, overcome, defeat.

And frustration also gives game designers and publishers something to position a monetization model around, whether it’s standard interstitials between levels, or pre-boss-level boosts, or post death revivals … you name it.

Hitting the Goldilocks zone of ad monetization

We all know the Goldilocks story.

Goldilocks tries three bowls of porridge. The first is too hot, the second is too cold, and the third is just right. If she worked for a mobile games publisher with a job in monetization, she’d probably try at least that many levels of ads-based monetization as well.

The goal: not too much, where you’ll lose players. Not too little, where you’ll miss out on revenue.

But just right, where players are happy enough to stay and even engage deeper, and you’re making solid revenue.

“ I see people experimenting with what they allow with the end cards and the creative length,” says Braberg. “The eCPM goes up the longer the creatives, right, because you have better CTR. So [the ad networks] pass that on to you in terms of higher eCPM. So maybe you need to experiment with this … maybe you want to put 45 seconds, 15 seconds. It’s different depending on the type of genre, right?”

That makes sense, of course, and clever testing will allow you to unlock the Goldilocks zone of monetization for your specific app, in your specific geos — it could be different for each geo you’re active in — and for your specific players.

But there’s a challenge: you need to be pretty big already in order to get this kind of leverage with most ad networks: to tell them what length of creative and end cards you’ll allow.

“It’s very unfair for new developers,” Braberg says.

Mobile game monetization: designing for profitability

So if you’re building a game that has monetization running right through its DNA, and you’re looking to hit the Goldilocks zone of just the right amount of ads, what does that look like?

For a puzzle game, that’s probably about 5 playing sessions a day totaling 18 to 25 playable minutes, Braberg says.

Here’s how it breaks down:

“If you want to optimize towards interstitial and basically earning the majority of your revenue from interstitials, you need to have your user base watch about 12 to 15 interstitials per day. So that means that you’re aiming for anywhere between 18 to 25 playable minutes, over five sessions per day, because that means you have users’ attention playing games for about 1,200 seconds, which means that you can show interstitial every 90 seconds and get to those numbers.”

Which is a perfect example of working backwards to design mobile game monetization right from the start.

Hybrid monetization: segmentation right from UA campaigns

Ads-based monetization is important for a huge percentage of games. But hybrid monetization, using ads, IAPs, and subscriptions for a full suite of mobile game monetization options is important for even more.

But the most successful games publishers don’t just offer hybrid monetization options blindly. Rather, they’re intentional about how they present those monetization options to players.

Like Hexa Sort, which Braberg calls one of the most innovative games in the hybrid space right now. Hexa Sort segments players not by geo but by user acquisition campaign:

“If [a player] comes from an IAP campaign, you don’t see ads for the first three days,” says Braberg. “So it keeps this premium feel, it increases the likelihood of you making an IAP. If you are an organic user or if you are an Ad ROAS user, you see ads after the first time user experience.”

That kind of focus and personalization has driven the game to something near a $250M annual run rate, Braberg says.

The key: tailoring monetization efforts to each acquired segment. That starts before a player touches a game, with the kinds of creative and types of messaging in acquisition campaigns that target ad monetizing users and others that target IAP players.

There’s more in the entire Hack Gaming Growth miniseries

Fintech is eating banking. Every traditional bank wants to be a digital bank, and every payments app, wallet app, and other kind of fintech app wants to be a neobank. But who’s winning? And what fintech apps are leading in 2025?

I took a look at the top 100 fintech apps in the world right now by downloads over the past 90 days. Here’s what I’m seeing globally for the top fintech apps across both iOS and Android. Each top fintech app for 2025 is listed with the country of origin and the category that it belongs in, and growth is averaged across both iOS and Android apps:

Rank

App Name

Country

Category

1

PhonePe: Secure Payments App

India

Payments

2

Airtel Thanks: Recharge & Bank

India

Bank

3

Pi Network

United States

Cryptocurrency

4

PayPal – Pay, Send, Save

United States

Payments

5

Paytm: Secure UPI Payments

India

Payments

6

DANA Dompet Digital Indonesia

Indonesia

Digital wallet

7

Binance: Buy Bitcoin & Crypto

Malta

Cryptocurrency

8

Google Pay: Save, Pay, Manage

United States

Payments

9

UnionPay APP

China

Payments

10

Mobile JKN

Indonesia

Billing

11

Nu

Brazil

Bank

12

ShopeePay – Gebyar Ramadan

Indonesia

Payments

13

Mercado Pago: cuenta digital

Argentina

Bank

14

Electronic Taxation Bureau

China

Taxes

15

Google Wallet

United States

Digital wallet

16

Revolut: Send, spend and save

United Kingdom

Bank

17

Navi: UPI, Investments & Loans

India

Bank

18

Klarna | Shop now. Pay later.

Sweden

BNPL

19

Bajaj Finserv Loans, UPI & FD

India

Bank

20

Banco Itaú: Conta, Cartão e +

Brazil

Bank

21

Alipay – Simplify Your Life

China

Payments

22

Personal income tax

China

Taxes

23

PicPay: Conta, Cartão e Pix

Brazil

Bank

24

Groww Stocks, Mutual Fund, IPO

India

Investments

25

Phantom – Crypto Wallet

United States

Cryptocurrency

26

YONO SBI:Banking and Lifestyle

India

Bank

27

Cash App: Mobile Banking

United States

Bank

28

GoPay: Transfer Pulsa Bills

Indonesia

Payments

29

super.money – UPI by Flipkart.

India

Bank

30

Coinbase: Buy BTC, ETH, SOL

United States

Cryptocurrency

31

FGTS

Brazil

Insurance

32

Agricultural Bank of China

China

Bank

33

Angel One: Stocks, Mutual Fund

India

Investments

34

Kotak811 Mobile Banking & UPI

India

Bank

35

World App – Worldcoin Wallet

United States

Cryptocurrency

36

IPPB Mobile Banking

India

Bank

37

Intuit Credit Karma

United States

Bank

38

Bybit: Buy & Trade Crypto

Singapore

Cryptocurrency

39

Zapay: pagar IPVA 2025, Detran

United Kingdom

Payments

40

Trust: Crypto & Bitcoin Wallet

United States

Cryptocurrency

41

OKX: Buy Bitcoin BTC & Crypto

Seychelles

Cryptocurrency

42

TradingView: Track All Markets

United States

Investments

43

MobiKwik: BHIM UPI & Wallet

India

Digital wallet

44

CAIXA Tem

Brazil

Bank

45

Industrial and Commercial Bank of China

China

Bank

46

GCash

Philippines

Payments

47

TurboTax: File Your Tax Return

United States

Taxes

48

Easy Personal Loan – KreditBee

India

Loans

49

BRImo BRI

Indonesia

Bank

50

Inter&Co: Financial APP

Brazil

Bank

51

CAIXA

Brazil

Bank

52

Wise: International Transfers

United Kingdom

Payments

53

Sweatcoin Walking Step Counter

United Kingdom

Cryptocurrency

54

Crypto.com – Buy BTC, XRP, ADA

Singapore

Cryptocurrency

55

Electronic Taxation Bureau

China

Taxes

56

Serasa: Consulta CPF e Score

Brazil

Loans

57

MetaTrader 5

Cyprus

Cryptocurrency

58

Traffic fines

Russian Federation

Fines

59

PhonePe Business: Merchant App

India

Bank

60

bKash

Bangladesh

Digital wallet

61

Pocket Broker – trading

Costa Rica

Investments

62

Venmo

United States

Payments

63

TrueMoney

Thailand

Bank

64

BYOND by BSI

Indonesia

Bank

65

testerup – earn money

Germany

Earning

66

Méliuz: Cashback, Cartão e +

Brazil

Rewards

67

FamApp by Trio: UPI & Card

India

Payments

68

InfinitePay Tap, Conta, Cartão

Brazil

Payments

69

SeaBank

Indonesia

Bank

70

Chime – Mobile Banking

United States

Bank

71

POP:UPI, Shopping, Credit Card

India

Payments

72

Bank of China

China

Bank

73

Investing.com: Stock Market

Cyprus

Investments

74

MB Bank

Vietnam

Bank

75

Capital One Mobile

United States

Bank

76

Bitget- Trade bitcoin & crypto

United States

Cryptocurrency

77

MetaMask – Crypto Wallet

United States

Cryptocurrency

78

Branch – Digital Bank & Loans

United States

Bank

79

Loterias CAIXA

Brazil

Bank

80

GoodScore: Credit Score App

India

Loans

81

Shriram One: FD, UPI, Loans

India

Bank

82

Government services

Luxembourg

Taxes

83

Olymptrade – Trading online

Grenada

Investments

84

mPokket: Instant Loan App

India

Loans

85

Zelle

United States

Payments

86

Official Traffic Fines

Russian Federation

Fines

87

Banco Santander Brasil

Brazil

Bank

88

Moneyview: Loans, Credit Cards

India

Bank

89

CoinMarketCap: Crypto Tracker

United States

Cryptocurrency

90

Remitly: Send Money & Transfer

United States

Payments

91

Rocket Money – Bills & Budgets

United States

Payments

92

CoinDCX: Crypto Investment

India

Cryptocurrency

93

Postal Savings Bank

China

Bank

94

OPay

Nigeria

Bank

95

MoneyLion: Banking & Rewards

United States

Bank

96

Banco will: Cartão de crédito

Brazil

Bank

97

ATTO

United States

Loans

98

Banco do Brasil: Conta Digital

Brazil

Bank

99

Banco Bradesco

Brazil

Bank

100

easypaisa – Payments Made Easy

Pakistan

Payments

I’ve translated some of the Chinese and Russian names, but left the Spanish names as it, since they use the same alphabet as English. Note that where the app is based does not govern where it is marketed and used, necessarily. And that categories are an estimate, as this is often challenging to determine.

Looking beyond fintech? Don’t miss our roundup of the top finance apps

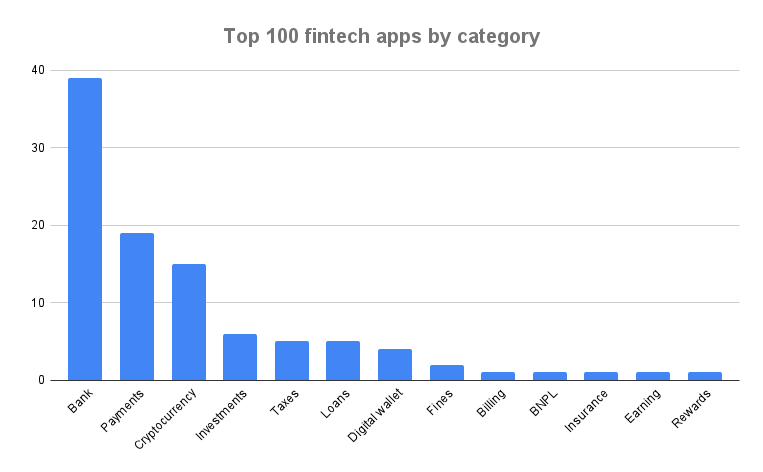

Top fintech apps 2025: top categories

The most immediately obvious insight in this list of top fintech apps is how many of these fintech companies are full-on or near-to banks. What we’ve been seeing over the past few years is that the top fintech apps have been expanding from payments to things like loans, investments, and rewards. Some still focus on 1 or a few main tasks, but many are trying to land and expand: get customers for 1 thing, and then offer multiple investment services.

So what we’re seeing is that 3 categories dominate: banking, payments, and cryptocurrency:

Bank – 39

Payments – 19

Cryptocurrency – 15

Investments – 6

Taxes – 5

Loans – 5

Digital wallet – 4

Fines – 2

Billing – 1

BNPL – 1

Insurance – 1

Earning – 1

Rewards – 1

Interestingly, BNPL (buy now pay later) is still a hot category, but most of the former players have added other services and so now fit into larger, more inclusive categories. Payments is still super-hot, and it’s a category where you typically see huge usage and engagement, especially in countries like China and India where digital payment is more a way of life than in the U.S., UK, or Germany, for example.

Newer categories I’m see pop up include government apps (and third-party apps) for paying fines, paying taxes, and getting benefits like employment insurance.

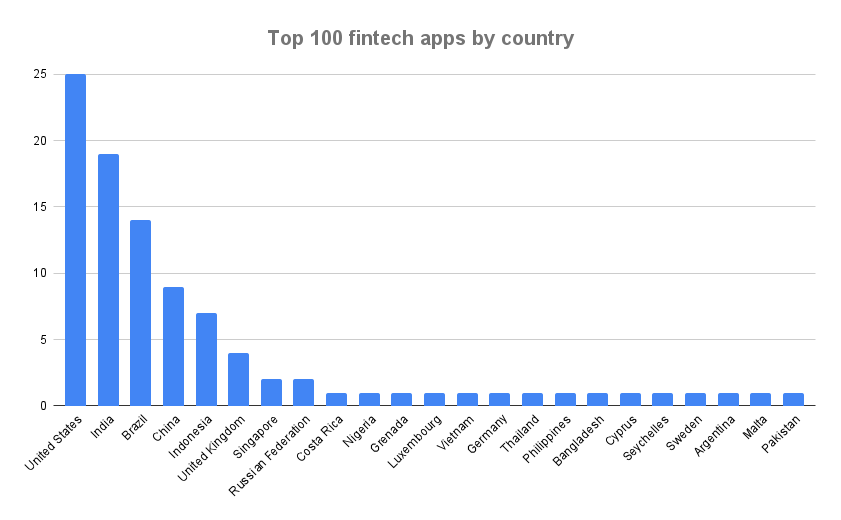

Top fintech apps 2025: top countries

Another insight in the top fintech apps list: many more countries are getting into the fintech space in a big way than we’ve seen in the past. Where before we would have seen China and India and the United States, we now see multiple European and Asian countries as well:

Of course, the United States, India, Brazil, and China dominate, but Indonesia and the UK are fairly prominent as well. And there’s a significantly long long tail for this chart:

United States – 25

India – 19

Brazi -l 14

China – 9

Indonesia – 7

United Kingdom – 4

Singapore – 2

Russian Federation – 2

Costa Rica – 1

Nigeria – 1

Grenada – 1

Luxembourg – 1

Vietnam – 1

Germany – 1

Thailand – 1

Philippines – 1

Bangladesh – 1

Cyprus – 1

Seychelles – 1

Sweden – 1

Argentina – 1

Malta – 1

Pakistan – 1

But let’s be honest: there are a ton of fintech startups and apps in the United States because it is wealthy and high-tech. And there are so many fintech startups, payments, and digital banking companies in India and China because those nations are huge and they have adopted mobile-first digital payments and banking technology like almost no other countries.

The future of fintech

Fintech is a super-interesting category right now. There’s still a significant growth trajectory in 2025 and beyond.

On the 1 hand, investment is down, with global startups raising the least since early 2020, but public valuations are up a sign that the massive Covid-era investments are paying off in real business value. And the outlook is positive too: fintech has a projected market size of $1.5 trillion in revenue by 2030.

The good news for fintechs focused on mobile is that mobile is central to the rise of fintech now and increasingly in the future:

Mobile apps are central to consumer fintech interactions

Payment apps, digital wallets, and mobile banking are seeing strong adoption rates

And innovations in connected commerce, in which banks and fintech companies use mobile data to offer personalized financial services, are growing too

This is most true in China. It’s incredibly adopted in India. It’s huge in Asia and parts of Africa. And over time, it’s increasingly becoming the norm in Western Europe and North America as well, despite the adoption challenges among the cash-obsessed older generation.

In other words, this is a category worth paying attention to.

Fintech is older than you think … literally over 100 years old

Fintech didn’t get its start when Apple invented the iPhone. Believe it or not, fintech is actually pretty old. In fact, if we define financial technology as digital or electronic means of dealing with money, fintech has its roots over a hundred years ago. No, there was no internet, but there were digital communications.

In 1918, the U.S. Federal Reserve built the Fedwire Funds Service, which still exists today. Using Morse code on public telegraph circuits, the Fed ensured that the U.S. dollar was worth the same amount in Pittsburgh as in Poughkeepsie, in Seattle as in San Antonio, and that interbank transfers could happen without time-consuming and risky transfers of cash or gold.

Much later in 1995, Wells Fargo — yep, the same company that operated the Pony Express in 1861 — made the first online checking account available.

And on May 22, 2010, a day that will forever be remembered as Bitcoin Pizza Day, Laszlo Hanyecz became the first person to spend cryptocurrency to purchase a physical item: a Papa John’s pizza. Hanyecz spent 10,000 bitcoin for the pizza, which would be worth approximately $650 million USD today. That is probably the most expensive pizza in history. I hope Hanyecz saved some other cryptocurrency for selling later when Bitcoin was actually worth real money.

When we think of fintech today, however, we think of new tech that manages, sends, invests, stores, and maximizes our money. And largely, we think of mobile apps as well as companion websites.

Categories and sub-verticals within fintech

There are likely as many different categorizations of fintech as people thinking about the category, but here’s an overview that simplifies the diversity in fintech as much as possible.

Fintech categories

Examples & top players

Banking

Branch, Airtel, Nu, Mercado Pago, Bank of America, Chase, Wells Fargo, Credit One, Navy Federal, US Bancorp, Citigroup

Budgeting

Mint, PocketGuard, Goodbudget, Honeydue, Personal Capital, YNAB, Everydollar, Intuit, Apple Pay

Buy now, pay later (BNPL)

Afterpay, Perpay, PayPal Pay in 4, Klarna, Affirm, Sezzle

N26, Chime, SoFi, Monso, Dave, Current, Tinkoff, MoneyLion, Starling Bank

Payments

PhonePe, Apple Pay, Google Pay, PayPal, Venmo

Tax

TurboTax, TaxAct, H&R Block, Electronic Taxation Bureau (China), Personal income tax (China)

Transfers/sending money

Remitly, Western Union, TransferWise, MoneyGram, Cash App, Apple Pay, Google Pay, Xoom, Facebook Messenger

As mentioned above, however, we’re seeing more and more consolidation in fintech. the top 100 fintech apps are all growing.

Payments apps want to be digital wallets. Digital wallets want to be banks. Banks want to offer insurance and investments. Essentially, once you have customers on your platform, it’s much easier to expand the services that they use. The more services they use, the more lucrative it is for the fintech providers, which is why the top 100 fintech apps have so many apps that offer multiple services for their users.

And it just makes sense for people too.

Wouldn’t you rather deal with 1 or 2 fintech companies than 5 or 6 … all of which need to have your financial details, your banking details, your payment information, and more? I know I would.

Big Tech and fintech: Apple, Google, Amazon

I mentioned earlier that Apple Pay didn’t even show up on the list of the top 50 payment apps on either platform because it’s a default in iOS. In fact, my new iPhone 16 Pro Max told me almost every day that my device set-up was incomplete until I finally gave up and set up Apple Pay by loading in my credit cards.

What’s interesting about Apple Pay is that it is deep integrated into both Apple’s mobile operating system and desktop. Plus, Apple has the innovative Apple Card — which is still U.S.-only — but offers no fees, ground-breaking family budgeting features, cash back, and useful data on spending patterns.

In addition, Apple Pay has simply huge existing reach and even more massive growth potential:

Apple Pay handled 1.8 billion transactions last year: up 40%

Over 90% of U.S. retailers accept Apple Pay

But there are still challenges. More than 90% of iPhone users who could use Apple Pay for in-store purchases still opt for traditional payment methods. (Yeah, I’m 1 of those. I sometimes use my phone for purchases, but not frequently.)

Plus the other big tech companies aren’t laying down and conceding the market.

Google has a much larger global userbase to convert to its financial apps

Google had over 150 million active users in 2022, which has certainly grown in the last 3 years

Google is also working with retail partners like Albertsons to integrate their operations with Google Pay. And there are enough Google fans on iOS who choose Google’s payment service over Apple’s that Google Pay is a top-25 app in the fintech category of the App Store.

In addition, Google has significant capabilities, installed base, and advantages in voice-based commerce on Google Home and in the Google app on both Android and iOS, suggesting that as customers get more and more used to asking Alexa, Siri, or Google to order more toilet paper or rent a movie, Google will do well here.

The rest of big tech is busy in fintech as well.

As you’d expect, Microsoft is working more on the business side of fintech, while Amazon has offered Amazon Pay since 2007 and has acquired fintech companies enabling both online and offline purchases. And, of course, Amazon is one of the biggest e-commerce companies outside of China. Facebook (or Meta) also offers some payment technologies, and as Facebook Marketplace gets bigger and more important, we might see some integrations there.

Top 100 fintech apps 2025: the challenge

COVID normalized digital banking, and the result was massive growth in fintech app usage, especially in the payments and banking categories. That’s only grown since.

The challenge for 2025 is to keep new users while continuing to expand both customer base and solution set. In some sense there’s a race to the middle between banks and neobanks. Traditional banks need to continue to get more digital and mobile. Neobanks in many cases need to offer more services and capabilities to amortize the cost of customer acquisition over more revenue-generating events … and to avoid losing customers to one-stop-and-you’re-done fintech competitors.

The challenge for fintechs today is to continue to grow in this hyper-competitive market that has been flooded with new cash. Finding the most optimal means of customer acquisition will be a huge competitive advantage, as well-funded rivals are almost guaranteed to be spraying money around like it’s the dot-com boom all over again. And with 26,000 fintech startups globally, this is not going to be an easy sector to win in.

Growth marketers and fintech

Growth marketers have a significant challenge in fintech. Your rivals literally have billions of dollars in new investment. Most of your top competitors have grown significantly through lockdown and quarantine periods.

What’s the best path forward?

Making sure every dollar of spend provides ROI. Optimizing ROAS across new, innovative channels and platforms. Killing poorly-performing partners quickly. Getting the best and the quickest insight into growth opportunities.

It’s 2025. What’s working for iOS mobile measurement? What is going to give you the data you need to beat the competition?

Sometimes it seems easier to identify what’s not working.

SKAN is still hard

IDFAs are still scarce

Creative testing is harder

Probabilistic has its own challenges

And modeling … each major platform has released or is working on its own particular flavor of modeling iOS app advertising results, but it’s not always clear what goes into that

That’s why I recently discussed the future of iOS mobile measurement and marketing in 2025 with Jesse Lempiainen, co-founder of GeekLab, and Neils Beenen from Singular. (This is part of our 5-part Hack Gaming Growth event: see all the episodes in 1 place here.)

Hit play and keep scrolling for the highlights:

iOS mobile measurement: what’s working

There is good news. iOS mobile measurement still works … just not quite like it did, and not quite to the same level as it did. But there are developments that are hugely successful in restoring ad tracking, creative measurement, and conversion analysis.

Measurement methodologies that matter include:

CAPIs (conversion APIs) CAPIs give you reliable deterministic data on conversions: usually conversions on a website. Snap, Google, Pinterest, TikTok, and Meta all have CAPIs. Learn more about CAPIs here …

AEM (Meta) and Advanced Conversions (Snap) and Ads Conversion Modeling (Google) Platform and ad network modeling give you additional data on ad impact, but they have some challenges (see below).

Advanced SAN from TikTok and similar programs from other platforms Advanced SAN and similar programs provide more data for MMPs like Singular to make accurate attribution decisions, while remaining privacy safe.

SKAN/AAK Yes, SKAN and its new iteration, AdAttributionKit are imprecise, partial, and delayed, but they are also deterministic and have value, even if they are not enough on their own.

Incrementality There are many ways to test for incrementality (see a 2025 guide to incrementality here) but they all have 1 goal: is my ad spend on Network X or Platform Y incremental. In other words, does it move the needle on growth, or does nothing change if I stop my spend there?

Probabilistic Let’s be honest, probabilistic is often used by programmatic networks, and likely others as well.

Data governance Data governance is simply enforced naming conventions for creatives and campaigns — Singular offers a platform which automates the process — that unlocks otherwise-hidden creative analysis capabilities.

The challenge for 2025 is for marketers to combine multiple attribution methods to navigate iOS mobile measurement in 2025. (Without going insane, or trying to boil the ocean, or stressing too much when varying means of measurement return slightly different results.)

The good news is that Singular does a lot of that for you in Unified Measurement.

And by mixing the deterministic data that we still can get, and modeled measurement techniques like incrementality, and insights based on smart data governances, marketers can still optimize their ad spend effectively.

Deduplication becomes the key when platforms model conversions

AEM and Advanced Conversions and Ads Conversion Modeling and all the other variants of platform iOS mobile measurement modeling are important in 2025. Yes, they’re a little black boxy. Yes, it’s challenging to know exactly how the big mobile adtech players are modeling their results.

But we are seeing more insights as a result of modeling that the big platforms are doing on conversion reporting, even if they’re a response to programmatic platforms using probabilistic methods and aimed at recapturing some of the installs and conversions that SANs won attributions on in the past.

The challenge is that when you’re looking at Advanced AEM or Ads Conversion Modeling from Google or Advanced Conversions from Snap, how do you know that they’re not all claiming the same installs?

“ Is there actually one way or one source of truth around how you can actually look at your performance data now?” asks Beenen. “That goes diametrically against the reality on the ground when it comes to measuring iOS signals because there’s too many sources available … the nitty gritty really goes into how you are doing your deduplication.”

Deduplication becomes key, and that’s where additional data from ad partners, like Advanced SAN from TikTok, is helpful.

“ We’re supporting AEM on TikTok, we’re supporting AEM on Meta as well,” says Beenen. “And if you then total the AEM up, of course we see a jump in the actual campaign performance.”

But it’s also important to look at data in your MMP dashboard, like Singular’s, to look for assists, showing you when ads on competing networks are working together to generate a result. And it’s important to check Singular’s attribution decisions, which are based on all the measurement data we can access. Singular sees what each network claims, but then makes an attribution decision that deduplicates all those claims, providing your best view of real, actual impact.

Ultimately you do want to bolster your iOS mobile measurement with incrementality testing as well. When done right, incrementality testing gives you extremely reliable data on what different ad partners and campaigns actually achieve.

Because ultimately you want data from your ad partners — or at least what they’ll share in a privacy-safe way with Singular — but you don’t want them completely grading their own homework.

Creative measurement requires smart data governance

The challenge with all modeling is creative measurement and optimization, which you’d really like deterministic data on. One solution for that lies outside the platforms and networks themselves, and it’s data governance.

Seemingly unnecessary for smaller organizations, data governance is essential for all because campaigns and creatives easily reach into the hundreds, even on just 1 platform, even at small scale. For large organizations, we’ve seen 10s of thousands of creatives, which very quickly scales out of control if you try to manage it manually.

Data governance helps with iOS mobile measurement because when you manage creative names, campaign names, geo encoding, conversion outcomes, and any other metadata you want for optimization and reporting well, you can get high-quality first-party data on which creatives and CTAs and campaigns worked best, converted most frequently, and resulted in the highest ROI.

Even, to an extent, inside platform black boxes that might take your creative and mix it up in the blender to build thousands of ads from dozens of components. You’ll still know that a certain image and a certain string of text were involved in good — or bad — results.

Conversion APIs (CAPIs) are increasingly important in iOS mobile measurement

When you think CAPIs, you think retail typically: a person clicks an ad, goes to a website — usually a mobile website, but not always — and buys a product. A web SDK in that retail site informs the ad network, and a conversion gets claimed.

But it can be used in gaming as well, via a mobile SDK.

And it’s another useful signal, says GeekLab’s Jesse Lempiainen:

“ That’s something that we’ve utilized quite a bit, both web2app campaigns that we partner up with Meta officially, and helping mobile publishers and developers do those web2app campaigns,” he says. “ We’re kind of staking a step back and measuring everything on a creative level and, and then utilizing these web technologies essentially … so conversion API to send events back to networks.”

Success that GeekLab is seeing there includes:

Lower cost

More daily new users in App Store Connect

Retention rate going up

But don’t expect it to be perfect: Lempiainen estimates the data accuracy level at around 70%.

Which brings up a good point in iOS mobile measurement for 2025: don’t expect perfect. And you don’t need perfect either. You do need good directional data that you can make quick decisions on … and that you can get.

In fact, that’s enough to keep the growth machine moving in the right direction.

User acquisition 2025 winners will need to be quick on their feet and nimble with their tactics. So much is changing, and so much of that is driven by developments in AI.

What can you expect in user acquisition for 2025?

Will AI do everything?

Will web2app be the trend of the year?

Will 2 or 3 ad networks totally take over mobile marketing?

We recently convened a group of experts to debate exactly this question: what should we expect in UA for 2025? Some of what you might want to learn is covered in our latest Quarterly Trends Report: check it out for all of the newest intel. But there’s even more in our Q1 2025 State of User Acquisition live event, which is now available on demand.

We talked about:

AI, LLMs

Web spend

CPI trends

The top growing ad networks

Predictions for 2025

And our expert panel of guests included:

Jonathan Reich CEO at Zedge, which has over 750M downloads (!!!)

Stephanie Pilon New CMO at Singular, led a digital transformation for a $600M business unit

Tomás Yacachury Strategic Partnerships at Kayzen (check out his reports: super insightful)

Ben Collins Jones Solution specialist, SplitMetrics (the first company ever to build an Apple Search Ads management platform)

Ashwin Shekhar CRO & co-founder, AVOW, which has partnerships with some of the biggest smartphone makers on the planet covering 86% of the global Android market for OEM UA deals.

State of user acquisition 2025: what to expect

1. Different targeting for AI-powered search

AI and large language models like ChatGPT are significantly changing the way advertisers need to approach search campaigns. Specifically, tight contextual targeting and keyword mapping for search campaigns aren’t the best way to go as search becomes more AI-driven.

Since the AI understands your intent and not just the exact match words you’re using, you’ll miss good opportunities by targeting too literally and too tightly. User acquisition 2025 winners will need to take this into account:

“As search advertising evolves with the rise of these large language models, ads using phrases or broad match for Apple Search Ads—essentially discovery campaigns—tend to perform better because these LLMs are getting smarter and understanding intent a bit better,” says Jones. “These formats capture a massive range of user inquiries compared to older systems, where exact match keywords risk missing alternative ways people might be searching for your product.”

This is the case both for very top of funnel searches on public search engines as well as bottom of the funnel searches inside the App Store and Google Play.

The flip side: watch out for overly-broad matching that dilutes your results and reduces profitability.

2. Generative AI for on-the-fly creative

We’ll see the rise of generative AI in making creative that is personalized to an audience of 1, says Reich.

“I think that the next generation is going to be where AI begins creating AI ads for whatever ChatGPT or any of the other providers are rolling out so that you can have super customized and personalized ads that are created on the fly.”

That is likely going to be better and more successful on platforms with more first-party data and deeper knowledge about its users, and it’s also most likely going to happen in high-value verticals, thanks to the much greater compute costs that generative AI requires.

4. OEMs for smart, nimble UA campaigns

Once upon a time, OEM campaigns were vast, slow, ponderous things that took 6 months to configure and run, and were essentially set-and-forget, because you couldn’t change them.

Now you can do local on-device search campaigns, preloads, ads in OEM-owned apps or first-screen or lock-screen experiences, and much more, like Google Play Auto Install prompts.

“ The OM platforms offer a lot,” says Shekhar. “They offer a large user base, advanced adtech, and they have a lot of first party data. They know user behavior, they know what kind of apps you have, and they are leveraging all of this to deliver the right ads to people at the right time.”

User acquisition 2025 success could include an OEM strategy, which we’ve seen result in huge scale.

5. User acquisition 2025: think AI for reporting and analysis

We’re definitely seeing AI more for reporting and analysis of marketing campaigns (keep your eye on Singular here for interesting announcements in the near future).

It just makes sense: more insight, more analysis, and less effort.

Something I’ll recommend on this: always do a sanity check yourself. AI is not perfect, especially LLM-based AI, and mistakes can happen.

6. Influencer marketing + guerrilla marketing … with some star power

Influencer marketing is still in its growth phase, says Ben Collins Jones. And he’s seeing more and more brands, including the biggest brands on the planet, do cool stuff that goes viral.

“ We’re seeing a shift of marketers towards organic growth through social media and traditional channels to boost brand awareness, and build communities,” he says. “This means partnering with celebrities — star power is never gonna go away, right — but also then adopting it across channels and engaging in co-marketing with well-known brands and barter agreements, and even then ultimately using guerilla marketing.”

The example he gave?

Severance, a show by Apple on Apple TV+, set up an office in Grand Central Station and actually had the show’s stars pretending to be working in that office. That created huge buzz, Reddit was taken by storm, and it turned into a massive promotion that they could not really have bought or paid for.

7. Better channel/partner testing efficiency via AI

If you have AI helping with analytics, you can also have AI helping with testing new channels and testing new partners.

Part of the reason marketers don’t test as many new channels and partners as they might like to is the overhead in attention and time that it requires, and the result is lower marketing efficiency. (Stay tuned for data that we’ll be releasing shortly that shows that generally, the more partners marketers use, the higher ROI they get.)

So if you can get help with AI, you can test more.

Testing more means you can unlock higher marketing ROI.

8. Web2app is super hot, but you need the right tech

63% of website traffic is happening on the mobile web, says Singular’s Stephanie Pilon, making it the perfect place to capture intent.

(Especially because a lot of that behavior is goal-oriented. Target well, and you have a good shot at getting attention.)

“ Think about how many times a day you’re opening your phone to do a search. I mean, this is the most beautiful place for you to actually advertise your app because that is where people are looking,” she says. “It’s often that I’m actually going to Mozilla or Google, basically to do the search before I’m even going into the app store.”

But you need the right tech to make it happen, including:

Comprehensive cost reporting, so you capture cost from all channels and all platforms

A web SDK, so you can capture all the events you need to track and optimize

Plus, of course, deep linking, which makes a smart contextual bridge between the mobile web and your app

And don’t forget link governance, which is going to ensure that all the insights you need will actually be captured and understood in a scalable, smart way

That ingredient list gives you full funnel understanding on creatives that drive action, landing page elements that work, and campaigns and partners that are effective, Pilon says. (See more details on the components of the solution, all of which you can get from Singular in 1 integrated package: cost aggregation, web attribution, deep linking, data governance.)

Featuring insights from Jonathan Reich, Stephanie Pilon, Tomas Yacachury, Ben Collins Jones, and Ashwin Shekhar, this user acquisition 2025 webinar will equip you with the insights you want to outperform your competitors this year.

Game analytics is hard. Retention curves are hard. Calculating LTV can be hard, and knowing how many DAU you’ll have after 7 months of growth campaigns is also hard. Fortunately, there are some new free tools to help you figure it all out without knowing Python, without having to write complex scripts, and without even having to do some complicated spreadsheet work.

It’s called Professor Arpdau, and it’s a suite of (mostly) free online tools designed to help game developers and marketers predict user retention and lifetime value (LTV), plus optimize pricing for different global markets.

It’s from Russell Ovans. If that name rings a bell, it’s because he wrote a massive book on analytics for mobile games called Game Analytics: Retention and Monetization in Free-to-Play Mobile Games. The book is great, but it has some parts with lots of math and code, and Ovans wanted to make game analytics “stupid simple.”

I recently had a chat and got a demo from Ovans.

Click play to check it out:

Engineering mobile growth via game analytics

Ovans is an entrepreneur, software engineer, and computer scientist. He’s also the former director of analytics for East Side Games, makers of Star Trek, The Office, and Trailer Park Boys games, among others. He’s still on the board there.

So he knows a bit about mobile growth and game analytics.

And he knows what’s key to your app growing.

Things like retention, where tiny improvements in D7 or D30 metrics can have a huge impact on revenue.

And pricing strategy, where just letting Google or Apple set your global prices based on exchange rates will result in much lower sales and profitability than you might think.

Or live ops investment, because games with good retention (8%+ at D90) typically invest in events, new content, and player engagement.

And LTV forecasting, because by understanding expected revenue per player, UA managers can bid confidently on new installs.

But calculating retention, LTV, and expected DAU over time are challenging. And implementing a global pricing strategy on Google Play, for instance, is tedious and painful.

So he built some tools to make it easier, and is releasing them for free.

Free tools for game analytics: retention, LTV, DAU predictor

There are 3 free tools in the Professor ARPDAU game analytics collection:

Retention Curve Creator This tool helps game developers predict long-term retention by inputting early retention numbers (D1, D3, D7). The model fits a curve to the data to estimate D30, D90, and even D365 retention. Retention curves are the foundation for all other game revenue and performance predictions, so this is critical.

LTV Predictor The LTV Predictor uses the retention curve that you’ve just built, plus your ARPDAU (Average Revenue Per Daily Active User) to forecast customer lifetime value over time. It provides D7 ROAS (Return on Ad Spend) targets to help UA managers determine if an ad campaign is on track to break even, providing insights like break-even timeframes. For example, if D7 ROAS is 29% of CPI (Cost Per Install), you can expect to break even by Day 90.

DAU Predictor The DAU Predictor estimates how many DAUs and revenue a game will generate based on your retention curve and daily installs, which helps marketers forecast how big a game will get and whether their retention strategy is working. For example, with 2,500 installs per day and a retention curve of r(n) = 0.33 * n -0.238, the DAU Predictor estimates you’ll have 95,000 DAU after a year with daily revenue approaching $150,000.

This is super-helpful for the non-technical mobile marketer, but it’s also super-helpful for technical marketers. The reason: it’s incredibly simple to pop in different numbers and check what a different retention curve might do for your break-even period. Or what slightly increased UA might do for your daily revenue numbers in a year’s time.

It’s “stupid simple” game analytics, which means it’s also really really fast. And speed is just as important as ease.

1 paid tool: country-specific pricing

There is 1 paid tool as well for country specific pricing.

The reason is that if you have 20 different items that can be purchased, implementing a price for each in each geo you’re releasing the game is almost impossible. It’s tedious and time-consuming. And many games have 50 or a hundred items players can buy. Multiply that by 150 countries, and you’ve got a recipe for a wasted week.

So you let Google Play do it automatically.

The problem: it doesn’t understand the Big Mac index. In other words, it just does a straight conversion between currencies without taking into account affordability.

The result is lost revenue.

“Professor ARPDAU not only uses current exchange rates and understands which countries have a value added tax or goods and services tax that must be included in the price, it will go through and adjust all of your prices using the Big Mac index or purchasing power parity, whatever it has data available for, to try to come up with a price that’s more comparable in the 100 other countries that your game may be available in,” says Ovans.

It then gives you a CSV file with all the right pricing to upload to Google Play: updating all your pricing all at once.

Ovans learned of this problem when seeing lack of profitability for East Side Games in Mexico, where automatic currency conversions resulted in prices that were unaffordable for locals.

After adjustment, revenue went up significantly, as did profitability.

AI-driven large language model (LLM) search engines are going to completely change the way we find information, answer questions, search for products, and make purchase decisions. So it’s past time that we take a look at the emerging LLM search advertising landscape.

A visual overview of the LLM search advertising landscape

LLMs that matter: ChatGPT and more

As I write this, LLMs are growing super-fast, even if the LLM search advertising space is still incredibly young.

Here’s the ones that we can get data on:

ChatGPT by OpenAI: 400M weekly users

Ernie Bot by Baidu: 300M users (no details on MAU, DAU or WAU)

Gemini by Google: 250M weekly users

Llama by Meta: 200M weekly users

Claude by Anthropic: 50M weekly users

Perplexity AI: 15M weekly users

(Sources: BI, Reuters, Gemini estimate based on 106M app downloads plus 275M monthly visits plus integration into Google tools such as Gmail and Meet: 9M organizations, Llama estimate based on Mark Zuckerberg’s recent statement that Llama was serving 600M users monthly, Claude extrapolation from SimilarWeb, plus app usage, FT)

ChatGPT leads, hitting around 1% of global search volume by some measures. That seems small until you realize that with all the resources of Microsoft behind it Bing worked for a decade to capture share from Google and is still only under 4% of global share.

Gemini, Perplexity, and Copilot are also players in search, though with less usage. DeepSeek is a recent challenger.

And Llama by Meta might be a sleeper here: it’s not a standalone product or service like many of the others, and so much of its use might go unreported by analytics engines that detect traffic on the open web. Meta has embedded Llama in pretty much every significant product, so it could have a massive share that we’re just not seeing.

LLM search advertising versus traditional search engines

Of course, LLMs are much more than search engines. In fact, they’re vastly different than search engines. And that difference shows us what will change in an LLM search advertising platform.

Search engines are exactly that: focused on SEARCH.

That’s actually a bad metaphor for what we wanted to accomplish in 1995 when we fired up Yahoo to look for something on the brand-spanking-new World Wide Web. And it’s a bad metaphor for what we want from Google and Baidu and Bing today.

We don’t want to search.

We want to FIND.

More than that, we want to know. To understand. Maybe, to make a decision. Perhaps to make a purchase.

Traditionally, a search engine provides links to sources — it retrieves and ranks web pages, leaving users to sift through results. In contrast, an LLM like ChatGPT delivers direct answers. It synthesizes information into a conversational, coherent response without requiring users to browse multiple sources. Search engines excel at finding specific web content, while LLMs focus on understanding context and generating responses tailored to user intent.

Of course, search engines have been changing over the years to offer more and more on-site zero-click answers, but LLMs take this to a new and vastly higher level.

Traffic from LLMs

We’ve seen the massive growth in LLM traffic here at Singular. As we reported in our latest Quarterly Trends Report, ChatGPT has become a top source of traffic for Singular customers without even offering an LLM search advertising platform.

The growth here has been astounding from 1 quarter to the next: 8,400%.

Q3 2024: 1 Singular customer

Q4 2024: 85 Singular customers

In Q3, just 1 Singular customer received traffic from ChatGPT. In Q4, that ballooned to 85, and the growth per customer increased massively as well.

And ChatGPT doesn’t even have an advertising platform yet: this is just pure organic traffic measured by 1 of the simplest and oldest of open web analytics solutions: UTM parameters: “utm_source=chatgpt.com” at the end of referrer links.

The ad networks are coming

LLMs are monetizing primarily via subscriptions right now, and that will continue for premium customers. But advertising always comes in to expand TAM and market share to those who won’t pay, and it is already partly here.

LLMs that have active ad platforms right now include:

Gemini by Google Ads with answers

Llama by Meta (Ads surrounding Llama)

LLMs that are planning or preparing their ad platforms include:

ChatGPT

Perplexity

Claude

Expect every significant and open-to-the-public LLM to offer an ad network within the next 18 months or so. It’s essentially a requirement to capture value from all users, not just paying subscribers.

Ads for LLM search engines will be different

Ads will work differently on LLMs. And LLM search advertising platforms will be astly different than Google or Bing or Baidu.

How different we’ll find out over the next few years, but here’s some clues:

Targeting options:

Untargeted brand ads Everyone needs soap. Big brands with broad targeting could adopt a mass media approach.

Contextual targeting Someone searching for things to do in Tahiti might not have their flight yet..

Behavioral targeting ChatGPT gets a pretty good sense of who you are as you use it, and that’s first-party data which could be used to create interesting audiences..

Broad keyword matching Exact keywords won’t be necessary: LLMs understand language and can provide broad matching out of the box that is likely better than exact match keywords

Placement options:

Answers are different than search results..

Ads will be separate from answers..

Formats:

Initial LLM ads have been text, and we’ll continue to see that

We’ll also see some image+text ads, especially for sponsored product results

We may see video ads playing side-by-side with the question-answer interface

We’ll probably also see a much lower ad load. Google, for example, often has dozens of ads per page. LLMs may not exactly have pages per se, and are likely to have single-digit numbers of ads per screen, at least initially.

Query uniqueness may go up as well: search engine queries have been getting longer and more conversational over time. Where we might once have typed “best pizza NYC” we’re more likely to ask “Where can I get the best pizza in New York City?”

That’s only accelerated with Alexa and Siri and Google Assistant, and now particularly with LLMs. In fact, I often use voice — even on my laptop — with ChatGPT to enter a phrase, sentence, or even paragraph of inquiry, which the LLM search engine then uses to find a very precise, specific, and contextualized answer.

Taste of the future

We’re only getting a taste of the future right now.

LLM search advertising measurement will come too, with programs for MMPs like Singular, and this will all get more sophisticated.

“This is only a taste of the future,” says Singular CMO Stephanie Pilon. “Perplexity has already set up ads on its LLM , and we’re seeing movement from Google’s Gemini as well. We expect LLMs like ChatGPT to be much more significant in marketers’ and advertisers’ plans in 2025.”

Of course, you already know: incrementality testing helps determine whether your ad spend is truly driving new user growth … or merely capturing users who would have installed your app anyway.

But how important is incrementality testing?

And how can you do it relatively painlessly?

In a recent Growth Masterminds I chatted with Jonathan Reich, the CEO of an app publisher with 750 million app installs: how they think of incrementality, how they measure incrementality, and tips for how you can do the same. The publisher is Zedge, which specializes in phone personalization with offerings like wallpapers, ringtones, and AI-powered customization tools so people can create their own one-off phone customizations.

Their flagship Zedge app has been installed over 750 million times, with 25+ million active users and 15 million reviews (!!). It’s primarily ad supported, so smart arbitrage on user acquisition is critical.

Which makes incrementality testing also critical.

Check out our chat here:

Why Zedge started incrementality testing

Initially Zedge grew organically.

It’s in a cool niche — young smartphone owners are particularly interested in customization — and had such an early start from even before the smartphone era started that millions and millions of users just naturally downloaded the app and used it, thanks to strong ASO as well as SEO.

Eventually, however, Zedge started paid user acquisition in order to accelerate growth even more.

And it clearly worked.

But there was always a nagging question …

“At first, wow, we’re seeing return on ad spend through the ceiling,” Reich told me. “But then the question that came up was, hold on a second … if we were to stop advertising, would we generate those installs and that revenue accordingly?”

And that’s where incrementality testing comes into the picture.

How Zedge does incrementality testing

There are a ton of different approaches to incrementality testing:

Zedge primarily manages checking ad partners and campaigns for incrementality in 4 ways: