Content

- Top 100 fintech apps 2026

- Top fintech apps 2026: top categories

- The fastest-growing fintech apps in 2026

- Top fintech apps 2026: top countries

- The standout movers in 2026

- The future of fintech: 2026 and beyond

- Fintech is older than you think … literally over 100 years old

- Categories and sub-verticals within fintech

- Big Tech and fintech: Apple, Google, Amazon

- The challenge for 2026 growth marketers

- Singular can help you grow

Stay up to date on the latest happenings in digital marketing

Summary

-

Diversification of Services: Fintech apps are increasingly expanding from niche offerings (like payments) to comprehensive banking services, including loans, investments, and digital wallets. Marketing professionals should emphasize cross-selling opportunities to enhance customer retention and increase revenue streams.

-

Mobile-First Strategy: With mobile apps central to consumer interactions in fintech, brands must prioritize mobile optimization and user experience. Leveraging data-driven insights to personalize services can significantly enhance user engagement and loyalty.

-

Competitive Landscape Awareness: The fintech space is becoming increasingly crowded with over 26,000 startups globally. To thrive, marketers must focus on efficient customer acquisition strategies and optimize return on ad spend (ROAS) to compete against well-funded rivals, ensuring every marketing dollar delivers measurable results.

Fintech is eating banking. Every traditional bank wants to be a digital bank, and every payments app, wallet app, and other kind of fintech app wants to be a neobank. But who’s winning? And what fintech apps are leading in 2026?

I looked at the top 100 fintech apps in the world right now, ranked by worldwide downloads across both iOS and Android over the 12 months through early June 2026. Each app is listed with the publisher’s country of origin and the category it belongs in.

The short version: PhonePe leads the world, followed by Navi, PayPal, Paytm, and Google Wallet. India puts 30 apps in the top 100, more than any other country. And lending apps are the fastest-rising category in fintech.

One more thing stands out before we get into the list. The Finance app category generated approximately 6.75 billion downloads in the 12 months through late 2025, but monthly downloads declined 4.6% year over year while revenue grew 10.2%. That’s not a warning sign. It’s a maturation signal: the market is shifting from pure user acquisition to deeper engagement and monetization. Keep that in mind as you read the rankings.

Top 100 fintech apps 2026

| Rank | App name | Country | Category |

|---|---|---|---|

| 1 | PhonePe: UPI, Payment, Recharge | India | Payments |

| 2 | Navi: UPI, Payments, Insurance | India | Loans |

| 3 | PayPal – Pay, Send, Save | United States | Payments |

| 4 | Paytm: Secure UPI Payments | India | Payments |

| 5 | Google Wallet | United States | Digital wallet |

| 6 | DANA Dompet Digital Indonesia | Indonesia | Digital wallet |

| 7 | ShopeePay | Thailand | Payments |

| 8 | Google Pay | United States | Payments |

| 9 | Mercado Pago | Argentina | Bank |

| 10 | Nubank: conta, cartão e mais | Brazil | Bank |

| 11 | Bajaj Finserv: Loans, UPI & FD | India | Loans |

| 12 | Revolut: Send, spend and save | United Kingdom | Bank |

| 13 | UnionPay APP | China | Payments |

| 14 | Binance: Buy Bitcoin & Crypto | Singapore | Cryptocurrency |

| 15 | super.money – UPI by Flipkart | India | Payments |

| 16 | Kotak Bank: 811 Mobile App | India | Bank |

| 17 | HDFC Bank App: Banking & Cards | India | Bank |

| 18 | GoPay: Transfer, Bayar, QRIS | Indonesia | Payments |

| 19 | YONO SBI: Banking & Lifestyle | India | Bank |

| 20 | BHIM Bharat’s Own Payments App | India | Payments |

| 21 | Klarna: Smarter everyday money | Sweden | BNPL |

| 22 | MariBank (SeaBank) | Indonesia | Bank |

| 23 | Freecash: Earn Money | Lithuania | Earning |

| 24 | Electronic Taxation Bureau | China | Taxes |

| 25 | OPay | Nigeria | Bank |

| 26 | Groww | India | Investments |

| 27 | bKash | Bangladesh | Digital wallet |

| 28 | Santander | Spain | Bank |

| 29 | easypaisa: a digital bank | Pakistan | Bank |

| 30 | GoodScore: Build Credit Score | India | Loans |

| 31 | Banco PicPay: Cartão, Pix e + | Brazil | Bank |

| 32 | IPPB Mobile Banking | India | Bank |

| 33 | FamApp by Trio: UPI & Card | India | Payments |

| 34 | Personal Income Tax | China | Taxes |

| 35 | Moneyview: UPI, Personal Loans | India | Loans |

| 36 | Jar: Save Money in Digital Gold | India | Investments |

| 37 | KreditBee: Personal Loan App | India | Loans |

| 38 | Gocrypto: Crypto Trading | Cyprus | Cryptocurrency |

| 39 | Cash App | United States | Bank |

| 40 | Agricultural Bank of China | China | Bank |

| 41 | Angel One: Stocks, Mutual Fund | India | Investments |

| 42 | CAIXA | Brazil | Bank |

| 43 | ICBC Mobile Banking | China | Bank |

| 44 | Wise: International Transfers | United Kingdom | Payments |

| 45 | Wave – Mobile Money | United States | Digital wallet |

| 46 | JazzCash – Your Mobile Account | Pakistan | Digital wallet |

| 47 | InfinitePay Tap, Conta, Cartão | Brazil | Payments |

| 48 | CAIXA Tem | Brazil | Bank |

| 49 | TradingView: Track All Markets | United States | Investments |

| 50 | Inter – Send Money | Brazil | Bank |

| 51 | BRImo | Indonesia | Bank |

| 52 | Serasa: Consulta CPF e Score | Brazil | Loans |

| 53 | MoMo | South Africa | Digital wallet |

| 54 | MetaTrader 5: Forex, Stocks | Cyprus | Investments |

| 55 | FGTS | Brazil | Insurance |

| 56 | Banco Itaú: Conta, Cartão e + | Brazil | Bank |

| 57 | BBVA | Spain | Bank |

| 58 | CCB Mobile App | China | Bank |

| 59 | Branch Instant Personal Loan | United States | Loans |

| 60 | Pocket Broker | Russia | Investments |

| 61 | 0% EMI Shopping App | India | BNPL |

| 62 | GCash | Philippines | Payments |

| 63 | China Merchants Bank | China | Bank |

| 64 | Livin’ by Mandiri | Indonesia | Bank |

| 65 | mPokket: Instant Loan App | India | Loans |

| 66 | Banco Bradesco | Brazil | Bank |

| 67 | Kissht: Instant Personal Loans | India | Loans |

| 68 | Venmo | United States | Payments |

| 69 | Moniepoint Personal Banking | United Kingdom | Bank |

| 70 | Capital One Mobile | United States | Bank |

| 71 | Nagad | Bangladesh | Digital wallet |

| 72 | slice: UPI credit card & bank | India | Bank |

| 73 | World App – Real Human Network | United States | Cryptocurrency |

| 74 | BB: Banco, Conta, Pix, Cartão | Brazil | Bank |

| 75 | Bank of China | China | Bank |

| 76 | POP: Pay, Earn & Shop | India | Payments |

| 77 | JD Finance | China | Investments |

| 78 | Nequi | Colombia | Bank |

| 79 | Chime: Mobile Banking | United States | Bank |

| 80 | MobiKwik: Loans, UPI & Wallet | India | Digital wallet |

| 81 | IDFC FIRST Bank: MobileBanking | India | Bank |

| 82 | TrueMoney – Pay & Earn Coins | Thailand | Digital wallet |

| 83 | RING by Kissht: Personal Loan | India | Loans |

| 84 | wondr by BNI | Indonesia | Bank |

| 85 | True Balance – Loan App & UPI | India | Loans |

| 86 | OKash: Safe and reliable loan | Nigeria | Loans |

| 87 | Remitly: Transfer Money Abroad | United States | Payments |

| 88 | Kredivo | Vietnam | BNPL |

| 89 | Paytm for Business | India | Payments |

| 90 | Paotang | Thailand | Digital wallet |

| 91 | Olymptrade: Trading online | Cyprus | Investments |

| 92 | PNB ONE | India | Bank |

| 93 | JMO (Jamsostek Mobile) | Indonesia | Insurance |

| 94 | Banco PagBank | Brazil | Bank |

| 95 | Intuit Credit Karma | United States | Loans |

| 96 | IndSMART IndianBank Mobile App | India | Bank |

| 97 | JioFinance: For your life! | India | Loans |

| 98 | OVO | Indonesia | Digital wallet |

| 99 | OnePay – Mobile Banking | United States | Bank |

| 100 | SuperQi | Iraq | Payments |

Note: country of origin reflects the publisher’s home market, not necessarily where the app is most used. Categories are estimates, since many of these apps span multiple verticals. Chinese app names are translated to English.

Looking beyond fintech? Don’t miss our roundup of the top finance apps.

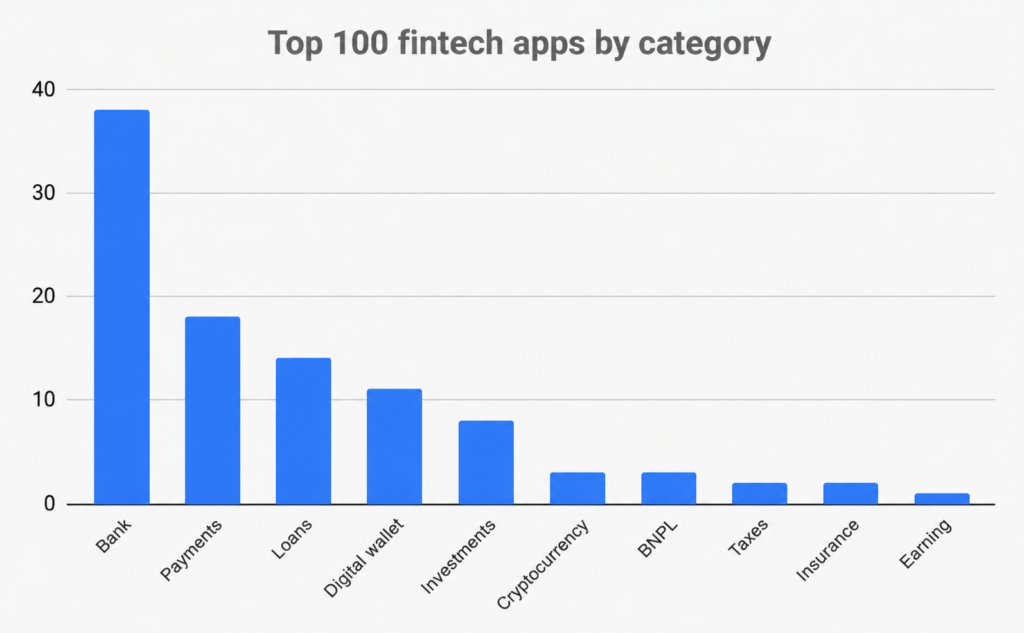

Top fintech apps 2026: top categories

The first thing you notice in this list: almost everything wants to be a bank. The land and expand playbook is alive and well. Get customers for one thing, then offer them everything else.

Here’s how the top 100 break down:

- Bank: 38

- Payments: 18

- Loans: 14

- Digital wallet: 11

- Investments: 8

- Cryptocurrency: 3

- BNPL: 3

- Taxes: 2

- Insurance: 2

- Earning: 1

Banks and payments dominating? No surprise there. The surprises are further down the list.

Lending apps nearly tripled, from 5 last year to 14 now. Most of that is India. Navi, Bajaj Finserv, KreditBee, Moneyview, Kissht, mPokket, and a whole wave of similar apps are serving credit demand that traditional banks never reached. Lending is quietly becoming fintech’s hottest download category.

And crypto? Crypto fell off a cliff.

Last year, 15 crypto apps made the top 100. This year: 3. Binance, Gocrypto, and World App. That’s it. Coinbase, Phantom, Trust, and OKX are all still big businesses. They’re just not download machines anymore. The speculative trading boom cooled, and crypto’s action moved to payments infrastructure like stablecoins instead.

Digital wallets are the other quiet winner, up from 4 to 11. Credit mobile money for that: bKash, Nagad, JazzCash, MoMo, Wave. For hundreds of millions of people across South Asia and Africa, these apps are banking. No bank account required.

The fastest-growing fintech apps in 2026

The title of this post promises who’s growing, so let’s deliver. Here are the 10 fastest-growing apps within the top 100, by year-over-year download growth:

| App | Country | Category | YoY download growth |

|---|---|---|---|

| HDFC Bank App: Banking & Cards | India | Bank | +3,929% |

| Paotang | Thailand | Digital wallet | +272% |

| MoMo | South Africa | Digital wallet | +229% |

| Freecash: Earn Money | Lithuania | Earning | +192% |

| JioFinance: For your life! | India | Loans | +148% |

| Jar: Save Money in Digital Gold | India | Investments | +134% |

| Navi: UPI, Payments, Insurance | India | Loans | +124% |

| 0% EMI Shopping App (Snapmint) | India | BNPL | +110% |

| BHIM Bharat’s Own Payments App | India | Payments | +108% |

| Gocrypto: Crypto Trading | Cyprus | Cryptocurrency | +106% |

Six of the ten are Indian.

HDFC Bank’s number looks like a typo. It isn’t. Downloads grew almost 40x year over year, the kind of jump that usually comes with a major app relaunch or migration push, and it vaulted India’s largest private bank to #17 on the global list.

The more interesting story is Navi. It’s already #2 in the world by downloads, and it has more than doubled year over year. Growing that fast at that scale is rare in any app category.

And BHIM deserves a mention: India’s government-backed UPI app more than doubled its downloads eight years after launch. Government fintech apps growing like startups is very 2026.

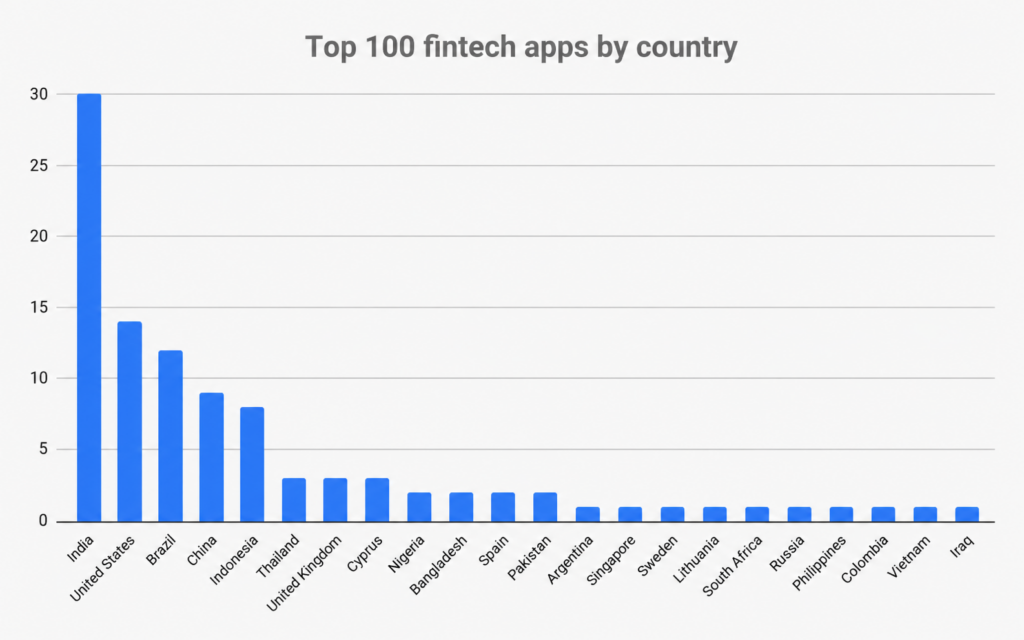

Top fintech apps 2026: top countries

The geographic spread keeps widening. Four or five years ago, this list was basically the US, China, and India. Now:

- India: 30

- United States: 14

- Brazil: 12

- China: 9

- Indonesia: 8

- Thailand: 3

- United Kingdom: 3

- Cyprus: 3

- Nigeria, Bangladesh, Spain, Pakistan: 2 each

- Argentina, Singapore, Sweden, Lithuania, South Africa, Russia, Philippines, Colombia, Vietnam, Iraq: 1 each

India isn’t just leading. 3 in 10 of the world’s most-downloaded fintech apps are Indian. UPI made digital payments free and instant, and an entire ecosystem of payments, lending, and investment apps grew on top of it.

The US still leads on familiar names: PayPal, Cash App, Venmo, Chime, Capital One. But volume from population-scale markets defines this list now. India, Brazil, China, and Indonesia are large, mobile-first populations that skipped branch banking and went straight to phones.

The long tail is the part worth watching. Nigeria (OPay, OKash), Bangladesh (bKash, Nagad), Pakistan (easypaisa, JazzCash), Iraq (SuperQi), and Colombia (Nequi) all put apps on this list. Fintech’s next growth markets aren’t hypothetical anymore. They’re charting.

The standout movers in 2026

A few apps deserve a closer look this year.

Revolut is the clearest breakout story in Western fintech. It passed 70 million customers globally in January 2026, up from 50 million in November 2024, and it’s the only European neobank in the global top 15 by downloads. The snackable product model keeps compounding: users come for one feature like currency exchange or travel spend, then gradually adopt more.

Klarna went public in September 2025 (NYSE: KLAR), and the app’s pivot is visible right in its name. It’s now “Klarna: Smarter everyday money,” not “Shop now. Pay later.” BNPL was the wedge. The ambition is the whole wallet. Its downloads dipped 16% year over year, which says less about Klarna and more about BNPL maturing as a category.

Mercado Pago keeps quietly compounding. Downloads grew 16% year over year, it sits at #9 in the world, and it’s the financial backbone for a huge slice of Latin American commerce.

Nubank, meanwhile, shows what the maturation phase looks like: downloads were basically flat, but that’s because most of its home market already has the app. The growth fight has moved from installs to engagement.

The future of fintech: 2026 and beyond

The macro context for fintech in 2026 is more constructive than it’s been in three years. Investment is recovering from the 2023 and 2024 lull, and the sector is still projected to reach $1.5 trillion in revenue by 2030.

Four structural trends are shaping what comes next.

1. AI is moving from support to action

In 2025, AI in fintech apps was mostly chatbots and fraud alerts. In 2026, it’s infrastructure. According to J.P. Morgan’s 2026 fintech trends report, AI-enabled fintechs now account for nearly half of all fintech deals, up from about a quarter two years ago.

On the product side, AI shows up as short contextual explanations and one-tap next steps: adjust a budget, move funds to avoid an overdraft, flag a recurring charge. Practical, not conversational. Behind the scenes, it’s running underwriting, fraud detection, and compliance.

2. Real-time payments are becoming table stakes

Real-time payment rails keep spreading. More banks are joining networks like RTP and FedNow in the US, and instant rails are already the default in markets like India (UPI), Brazil (Pix), and Thailand (PromptPay).

For fintech apps, this raises the baseline. Instant settlement is no longer a differentiator. It’s expected.

3. Privacy and regulation are reshaping acquisition

The regulatory environment around data and consent is tightening fast. PSD3 is rolling out across the EU. MiCA has made the EU the first major market with comprehensive crypto regulation. BNPL rules now require credit checks in a growing list of countries, and financial regulators keep issuing AI-specific guidance.

For growth marketers, this is the part that matters. Attribution complexity is growing, not shrinking. iOS ATT opt-in rates in the finance category remain low, which makes accurate mobile attribution increasingly critical for understanding what’s actually driving installs and activations.

4. Neobanks are winning the customer relationship

The neobank model has proven out, with hundreds of millions of users worldwide. And the race isn’t for the sign-up anymore. It’s for primary banking status.

That’s an LTV problem, not a CAC problem, and it’s forcing neobanks to invest heavily in retention, engagement, and cross-sell rather than raw acquisition.

Fintech is older than you think … literally over 100 years old

Fintech didn’t get its start when Apple invented the iPhone. If we define financial technology as digital or electronic means of dealing with money, fintech has roots over a hundred years ago.

In 1918, the U.S. Federal Reserve built the Fedwire Funds Service, which still exists today. Using Morse code on public telegraph circuits, the Fed ensured the U.S. dollar was worth the same amount in Pittsburgh as in Poughkeepsie, and that interbank transfers could happen without risky transfers of cash or gold.

Much later, in 1995, Wells Fargo made the first online checking account available.

And on May 22, 2010, a day remembered as Bitcoin Pizza Day, Laszlo Hanyecz became the first person to spend cryptocurrency on a physical item: a Papa John’s pizza. He spent 10,000 Bitcoin, worth roughly $600 million at mid-2026 prices. Probably the most expensive pizza in history.

When we think of fintech today, though, we think of mobile apps that manage, send, invest, store, and maximize money, with AI increasingly doing the heavy lifting underneath.

Categories and sub-verticals within fintech

There are likely as many categorizations of fintech as people thinking about the category, but here’s an overview that captures where things stand.

| Fintech category | Examples & top players |

|---|---|

| Banking | Nubank, Mercado Pago, Revolut, Chime, Monzo, N26, OPay |

| Budgeting | Rocket Money, PocketGuard, YNAB, Monarch Money, Copilot |

| Buy now, pay later (BNPL) | Klarna, Affirm, Afterpay, Snapmint, Kredivo, Sezzle |

| Credit history & monitoring | Credit Karma, Experian, Credit Sesame, MyFICO, GoodScore |

| Cryptocurrency & DeFi | Coinbase, Binance, Phantom, MetaMask, OKX, Bybit, Crypto.com |

| Education | Zogo, Investmate, NerdWallet, Penny |

| Insurance | FGTS (Brazil), Lemonade, Root, Jerry.ai |

| Investment | TradingView, Robinhood, Groww, Acorns, Public, SoFi, eToro |

| Loans | Navi, Bajaj Finserv, Branch, mPokket, KreditBee, Kissht, Dave |

| Neobanks | Revolut, Chime, N26, Monzo, Current, Starling Bank |

| Payments | PhonePe, PayPal, Apple Pay, Google Pay, Venmo, Zelle, GCash |

| Tax | TurboTax, TaxAct, H&R Block, Electronic Taxation Bureau (China) |

| Transfers | Remitly, Wise, Western Union, MoneyGram, Cash App |

| Stablecoins & tokenization | Emerging category; Circle (USDC) and PayPal’s PYUSD gaining traction |

The stablecoins row is new. A year ago I wouldn’t have included it. Now I have to. Monthly stablecoin transaction volume approached $1 trillion in 2025, according to J.P. Morgan. This is no longer theoretical infrastructure. It’s real payment volume.

Big Tech and fintech: Apple, Google, Amazon

Apple Pay doesn’t show up high in download rankings because it’s a default in iOS. My iPhone told me almost every day that device setup was incomplete until I finally loaded in my credit cards.

But Apple Pay’s footprint is massive:

- Apple Pay is accepted at over 90% of U.S. retailers

- It handled 1.8 billion transactions last year, up 40%

- And yet more than 90% of iPhone users who could use Apple Pay in stores still default to traditional payment methods

That last stat is the one I keep coming back to. Apple has the distribution. The behavior change is still in progress.

Google’s split strategy is working better on one side than the other. Google Wallet (contactless payments and stored passes) grew 13% year over year and sits at #5 worldwide. Google Pay (UPI and peer-to-peer) fell 17%, squeezed in India by PhonePe and Paytm. Both are still in the global top 10, which no other Big Tech company can claim in fintech.

The rest of Big Tech is active too. Amazon has offered Amazon Pay since 2007 and keeps expanding its fintech footprint. Meta’s payments inside WhatsApp keep growing quietly in Brazil and India.

The challenge for 2026 growth marketers

COVID normalized digital banking, and fintech app usage exploded. That growth has now settled into something harder: a competitive, monetization-focused market where downloads are flat or declining in mature segments, CAC is rising, and privacy restrictions make it harder to see which channels work.

So what matters most?

- Move beyond installs. The market has shifted from acquisition to retention and LTV. Install data alone misses most of what determines a fintech app’s success. You need full-funnel visibility, from ad click to account activation to first transaction to multi-product adoption.

- Attribution is harder, not easier. Between iOS ATT, the Android Privacy Sandbox, and new EU rules under PSD3, the signals available to fintech marketers are getting noisier. The winners will be the teams with the most accurate, unified measurement.

- Emerging markets are the volume engine. 7 of the 10 most-downloaded fintech apps come from publishers outside the US and Western Europe. If your growth strategy is purely US and Europe focused, you’re playing a low-growth game.

It won’t be easy. But for well-instrumented fintech apps, this market is still wide open.

Singular can help you grow

If you’re a fintech app looking for marketing intelligence that drives growth and measurement that provides the best insights for ROI optimization, we should talk.

Grab a slot here, and let’s chat. We’ll listen more than we talk, understand your business and your needs, and share what we can do to help.

Amey Kulkarni

Amey is a marketing practitioner with hands-on experience across the martech space, and Senior Marketing Manager at Singular. He writes about AI, analytics, and growth - with a focus on what's actually changing for practitioners, not just what's trending