John Koetsier is a journalist and analyst. He's a senior contributor at Forbes and hosts our Growth Masterminds podcast as well as the TechFirst podcast. At Singular, he serves as VP, Insights.

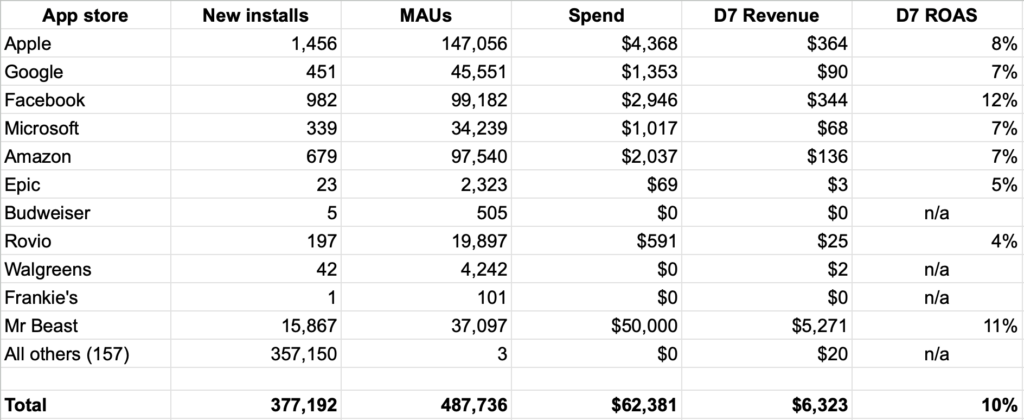

It’s 2025. Welcome to the multiverse of marketing on iOS with multiple app stores, perhaps even too many to count. You had close to 400,000 reported new installs — most of which are fake — across 167 different app stores that you bother to track and better than expected D7 ROAS of 10% across all marketing efforts.

Some highlights:

Mr Beast is roaring A recent $50K activation on Mr Beast’s app store is showing real promise with strong pick-up and outstanding D7 revenue

The original App Store is king The original Apple App Store is still your major source of monthly average users

Facebook loves data Working on 100% first-party data, Facebook returns to ROAS supremacy

157 flavors of fraud Over a hundred app stores are telling you they’ve supplied you with over 350,000 new installs and want your ad dollars to make it even more. But your MAUs with these fly-by-nights total just a miniscule 3.

A brave new world of mobile app advertising

We’ve talked about it before. The European Union’s Digital Markets Act is an attempt to open up competition in app stores, and it’s likely to be just an early warning wave in a coming tsunami of global legislation demanding the same from both Apple and Google.

Google has plenty of experience with third-party app stores thanks to China, India, and global competitors like Samsung and Amazon.

Apple, not so much. There are third-party app stores for iOS like BuildStore, AltStore, EonHub, CokernutX, Cydia, Xabsi, and more. But none of these app stores have really hit the bigtime. None of them are top of mind for a significant number of iPhone owners. And many of them, like iOS Haven, offer “tweaked, modded, and covert” apps. In other words, games that don’t require payment for IAPs, apps that do things their designers and developers never intended, and — most importantly — apps that can’t really be fully trusted by end users.

But by 2025, we’re likely to have multiple legally available and commercially interesting app stores.

Amazon is a no-brainer. So are Facebook and Google, who can take advertising, sales, and analytics all in-house, completely removing the sting of App Tracking Transparency and operating on their own rules in an earned and owned first party data platform.

All of it means much more opportunity for mobile advertisers to take advantage of, along with much more complexity for mobile advertisers to manage. Amazon has a different audience than Facebook. Massive influencers have their own demographics, and a Mr Beast is big enough to spin up an influencer-focused white label of an app store platform that rabid fans would likely embrace.

Just think: the Mr Beast lifestyle, the Mr Beast app for this, the Mr Beast app for that. Other big brands — think sports leagues like the NFL or NHL — already have “official” brand partnerships. Their own app stores would be just one step farther. This new world really starts to make sense when you go global, and you work with a big brand in Germany versus one in Nigeria versus one in South Korea and yet another in Australia.

Now marketers have the option to target specific audiences based on their affiliations.

But now marketers also have to gather data from dozens or even hundreds of different platforms to get a holistic picture of their global performance.

Multiple app stores: A brave new world of mobile app management

Of course, it’s not just marketers who get all the fun. Developers will get more than their share as well.

Different app stores will have different requirements. Different approval processes, both automated and manual. Some might sign lucrative partnerships that privilege one specific app or game in a category, and potentially even prohibit competitors from publishing their apps on the same store.

They’ll have different marketing strategies, ASO opportunities, search and discovery pathways. They’ll have different commissions, costs, and internal ad networks for promotion.

And shocker: they’ll also have different reporting.

Being able to assemble data from all these different outlets will seem familiar to old-school marketers in physical retail or multiple digital storefronts, but that won’t lessen the pain of aggregating and normalizing and standardizing all the different data points.

Developers won’t have to just navigate app submission requirements, but also updates, payments, notifications, refunds, reviews, and more. It will be a significant effort for each new app store, potentially, and it won’t be limited to app stores you choose. Many upstart app stores will look to grab apps and games off other stores and add them to their virtual shelves to bolster their own value proposition and revenue opportunities … and they won’t stop to ask permission.

Multiverse of madness: app fraud in so many new ways

App marketers know all about ad fraud that steals their ad dollars and shaves their ROAS margins, but it’s mostly Android developers who feel the special pain of hijacked or stolen apps marketed under different names in small, regional, or underground app markets.

Not to mention the blame they get when a hacked app does something nasty to an end user who then blames the original publisher.

With multiple app stores, iOS will join that party, and publishers will need some form of the always-popular (yes, this is sarcasm) digital rights management to ensure their apps aren’t stolen, altered, or hijacked in any way. Nothing they use for this, of course, will be 100% effective.

Multiverse of marketing: MMPs for sanity

All with aggregating all the various types of data from each platform, MMPs will also need to support and build integrations with app stores that matter.

Which, of course, could number in the dozens or hundreds, and which might implement their own type of digital advertising identifier, or provide no means for any marketing measurement whatsoever. And which, also of course, will need to operate in an iOS environment where Apple grudgingly tolerates them for legal reasons, if at all, and locks down iOS in new ways to protect against a more open (and more vulnerable) ecosystem.

Which will make MMPs even more essential.

MMPs already have to integrate with thousands of ad partners, but they’ve only had to connect with two major app stores. Now, likely, the ad-mediated nexus between consumer demand for apps and platform supply of those apps likely becomes much more balanced, with hundreds of app stores taking up the role of supply ads for iPhones. (And, of course, Android as well.)

A big question: consumer uptake

The current system is simple. It’s trusted. It’s safe: one place to get apps, no thinking, no pre-installing of a new store, no wondering if you trust a new app store with your credit card, and all payments coming from one brand.

So it’ll be a big change for iOS users (and most Android users) to get apps from multiple places.

Once they start, though, it might just open the floodgates. And that will be a massive change to an industry that’s already gone through ATT and will have just made the GAID to Privacy Sandbox for Android switch.

It’s the new multiverse of marketing, and it won’t be easy.

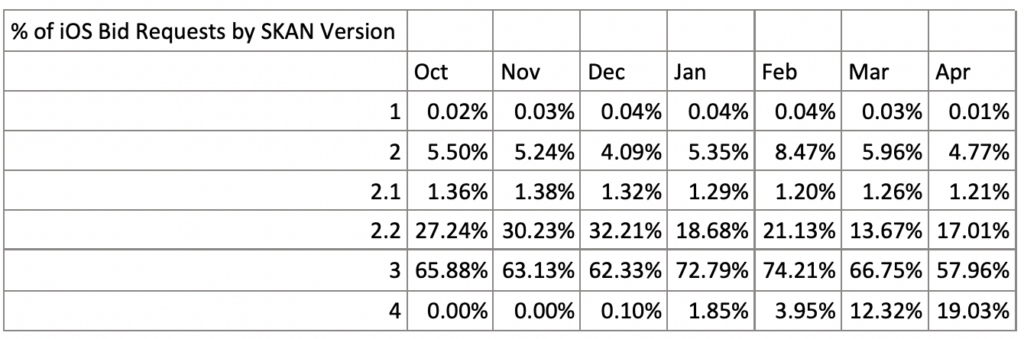

The SKAN 4.0 transition is definitely starting, but perhaps not yet at Formula 1 pace. Fewer than 1% of all iOS postbacks are SKAN 4 postbacks right now. And only 7 of the thousands of ad networks and platforms that Singular measures are actively adopting SKAN 4 at this point in time.

SKAN 4 is going to only see increased adoption: bid requests are hitting almost 20% and growing fast

Let’s see what’s happening on the technical side …

SKAN 4 transition: what’s happening

Most ad networks and platforms are testing the last version of SKAdNetwork for their ad inventory. That’s why Inmobi’s DSP is seeing over 19% of bid requests come in as SKAN 4 compatible as of April 2023 … a massive change from less than 2% just 4 months ago.

Some data that Sara Camden, InMobi’s head of product marketing, shared with me:

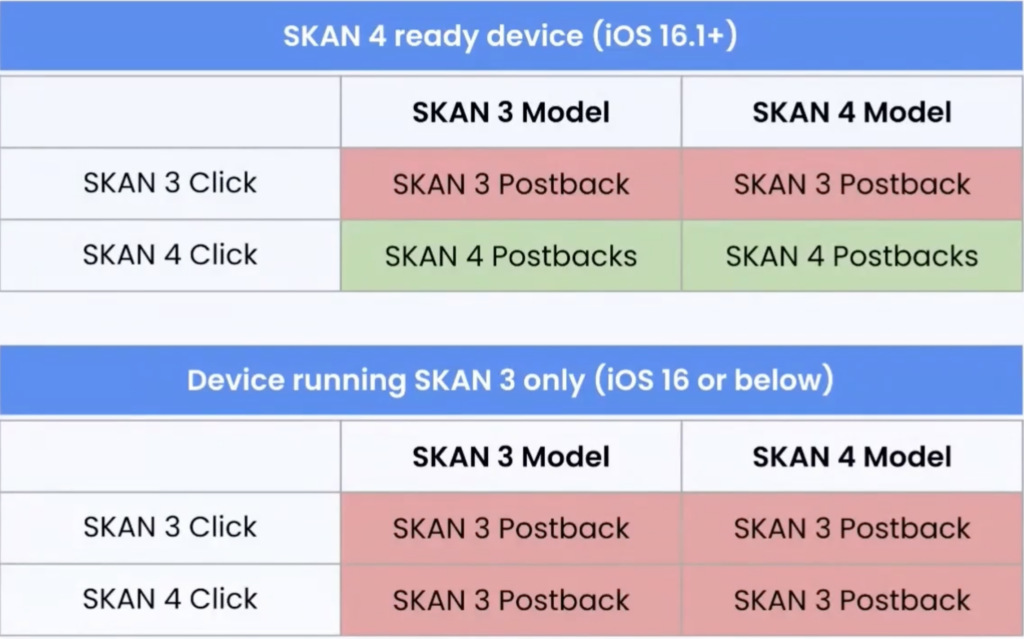

But it’s worth reminding ourselves what’s required to get a SKAN 4 conversion.

A SKAN 4 click, which requires the ad network’s set-up

Miss one of the required elements, and you get SKAN 3 postbacks. (Note: you can get SKAN 4 postbacks without having set up a SKAN 4 conversion model, but you’ll only see the first postback because SKAN 4’s second and third postback won’t have been set up.)

So the ad networks are (mostly) setting up, testing, and preparing. But now we need advertisers to also start setting up, testing, and preparing … which of course they haven’t been able to do until very, very recently.

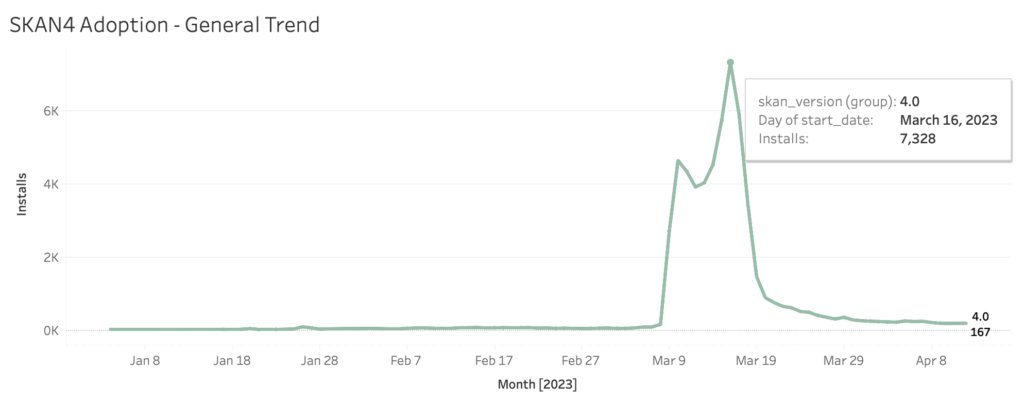

Low numbers of SKAN 4 postbacks so far …

The result is predictable: very low numbers of SKAN 4 postbacks, with a few spikes as ad networks ramp, evaluate, and then pause testing efforts.

This is Singular data from January to the first week of April:

Currently, SKAN 4 is seeing a .2% adoption rate when we look at all the variables: a SKAN 4 capable device with a recent iOS version, a SKAN 4 click from an ad network, and an active SKAN 4 conversion model from an advertiser. The spike in the graph above drives the percentage temporarily to almost 2% as one large ad network ramped up testing.

SKAN 4 transition: Time to pick up steam?

What we essentially see now is that many ad networks are starting to get ready. Ad networks that we see testing SKAN 4 recently include ironSource, Moloco, Smadex, Unity Ads, Appier, and Google AdWords. We’re also seeing “ad networks” that are essentially large publishers’ internal cross-promotion efforts testing SKAN 4 capability, boosting the SKAN 4 transition numbers.

Interestingly, the ad network that caused the spike in the chart above ran 86% SKAN 3 clicks and 11% SKAN 4 clicks in the second week of March (plus a few SKAN 2 and some null SKAN models to make up the 100%). By the beginning of April, that ad network was 97% SKAN 3.

In other words: there’s testing, evaluation of results, and then a pause. But also, ad networks need advertisers to jump on the SKAN 4 train and get conversion models set up so that they can evaluate the entire loop and advertisers can provide feedback on the results.

One reason to set up your SKAN 4 conversion model today is that it doesn’t impact any active SKAN 3 campaigns, as long as your SKAN 4 first postback conversion model is aligned with your only SKAN 3 postback conversion model. Additionally, as there’s increased ad network adoption of SKAN 4, you’ll start seeing the extra data from postbacks 2 and 3 show up in your dashboard … data that you’ll miss out on if you only have a SKAN 3 conversion model active.

Need some help getting up to speed?

You’re in luck. We’ve put together a complete SKAN 4 transition guide that highlights the changes, lists the strategic decisions you’ll need to make, and gives you a suggested plan for how to set up your SKAN 4 conversion models.

Singular has launched SKAN 4 conversion models so mobile marketers can begin collecting SKAN 4 data from ad campaigns: fine and coarse conversion values, postbacks 1, 2, and 3, and the extra source identifier data that Apple’s newest version of SKAdNetwork can now deliver.

But don’t panic: you don’t have to set up SKAN 4 campaigns immediately.

“This is here for people when they’re ready,” says Singular product marketing manager Kelsey Lee. “Just because it’s ready doesn’t mean people need to panic … this is just trying to get people in a state of mind of, oh: we should start testing. We should start having those important conversations with our network partners and thinking about how we want to think about postback 2, postback 3, and those coarse conversion values.”

That’s an important caveat.

SKAN 4 postbacks are definitely live in the wild right now, but they’re also a tiny fraction of all SKAdNetwork postbacks right now. Essentially, ad networks are testing their capability, building their SKAN 4 technology, and preparing to optimize campaigns with extra data. SKAN 4 is not currently fully operational and the default standard for any ad network just yet.

So what is currently available?

SKAN 4 conversion models

“What we have live is SKAN 4 conversion models,” says Singular VP of product Evyatar Ram. “You can go to your Singular dashboard, and you can create conversion models that are SKAN 4 specific, meaning they have P1, P2, P3. You’re setting up three different postbacks, meaning that you are setting up the coarse conversion values as well as the fine conversion values.”

SKAN 4 conversion models for revenue and events and live right now; other conversion model types are coming “very soon,” Ram says.

Here’s a quick overview of how it works:

Instant upgrades for SKAN 3 models

Existing SKAN 3 models can be instantly upgraded.

There’s a simple user interface for selecting the values you want for each of the 3 postbacks in SKAN 4, and you can set up your fine and coarse conversion models for postback 1. The coarse values that you’ll receive for postback 1 if you don’t achieve enough crowd anonymity for a specific campaign are aligned with the fine values, so your campaign optimization and future investment decisions won’t be impaired by incompatible data.

And while coarse values won’t be as informative as fine conversion values, they do beat getting null data on so many postbacks, Lee says. So while most marketers will try to optimize for getting the greatest number of fine postbacks, coarse values are not the end of the world.

An important point for marketers who aren’t even thinking too much about SKAN 4 right now: all SKAdNetwork 4 models are backwards compatible with SKAdNetwork 3.

So it just makes sense to create a SKAN 4 model in case some of your ad partners start using SKAN 4: you’ll capture data that would otherwise just simply be lost. And you won’t compromise any ongoing campaigns.

Plus, it’ll get you thinking about SKAN 4 and what’s possible in the new world of iOS attribution.

Is this a big easy button in the cloud for SKAN 4?

How easy is it to start using SKAN 4 with Singular?

“I think it’s as easy as it gets for having such a complicated framework to deal with,” Lee says. “I think Singular has done a really good job with making the UI as intuitive as possible.”

But there’s more coming soon.

Singular’s SKAN Advanced Analytics already models for missing SKAN 3 data to provide much more accurate revenue and cohort data. Singular is updating SKAN Advanced Analytics for SKAN 4, which will add more accurate, longer cohorts, and better modeling.

“So even if you don’t pass crowd anonymity, we’re filling in those gaps for you,” Lee says. “I don’t think it’s a big fat easy button … but I think we’ve done the best we can with all the limitations and restrictions.”

All the SKAN 4 conversion models details in the Growth Masterminds podcast

Watch the video above, and subscribe to the podcast on your on favorite podcasting platform: Apple Podcasts, Spotify, Google, or pretty much any other major podcasting platform.

How can you find super-valuable data on user acquisition cost benchmarks (and so much more) from top competitors in your space? That’s exactly what we chatted about with Clement Favier, Chief Operating Officer at Adikteev, in our latest Growth Masterminds podcast.

Some of the information he shared:

17% to 25% of social casino MAUs are going to be DAUs

2% to 5% of DAUs will be payers

SciPlay and PlayStudios grew over 10% last quarter

Average spend on user acquisition is 24% to 28% of revenue

Modern Times Group spent 39% of revenue on UA

How does he know all this? Read on …

User acquisition cost benchmarks: publicly available information

It’s publicly available information, and Clement Favier, Chief Operating Officer at Adikteev, has compiled it all from each company’s annual reports. They’re public companies, and as such have to share a significant amount of data about their operations, their costs, their revenue, and much more.

“Some will label it as advertising cost, some will label it as user acquisition spend,” says Favier. “It’s pretty much aligned on how much those companies are actually spending on marketing … I would say a rough average would probably be between 25 to 28%, and it goes from 24% of revenue that is actually allocated to a user acquisition span — that’s the case for Play Studios and CyPlay — and it goes up to 39% for Modern Times Group, for instance.”

It’s a novel way of looking at marketing comparables and finding user acquisition cost benchmarks. Most of the time mobile marketers are probably looking at owned data, looking at any shared data they can get — see Singular’s Ad Benchmarks, for example — looking at insights adtech company reports share, plus a few other ad intelligence sources.

So checking public company records for user acquisition cost benchmarks is a bit different.

The most likely reason: mobile’s pretty new, and before the last few years, there hasn’t been a lot of time for gaming companies to mature, IPO, and get on a stock exchange.

Now, thanks to growth, consolidation, acquisitions, and more, that’s changed.

Apply a grain of salt!

Of course, as Favier notes, all data insights have to be taken with a grain of salt and a hefty dose of context.

One key piece of context is the phase of the company: growth companies will naturally spend more, while companies that are consolidating and taking profits will naturally spend less. There’s a balance here too: while larger established players with known IP probably enjoy higher efficiency than relative unknowns, they may already have occupied their easiest niches, grabbed all the low-hanging fruit, and now have to jump or build ladders to get to the next tier of potential players.

But a marketing spend of 24% to 26% of revenues seems sustainable, Favier says.

“For those companies I mentioned earlier, I think that all of them are profitable with a positive EBITDA margin, so basically profitable,” he told me.

“So you could say that they’re all growing obviously, but also in a mature stage. So they think they’re not overspending and those are really considering their user budget very carefully and looking for profitable user acquisition. So this benchmark of 24 to 26% of revenue allocated to user acquisition seems to be really something that’s sustainable over the long term and that can be taken as a good proxy.”

All-in costs: user acquisition and team and tech and …

The good news about calculating marketing spend from public filings of traded companies?

It’s all-in.

Marketing spend isn’t just the $4-5 you spend for an install or the $20-50 you spend for a paying subscriber. It’s also your tech costs, your human costs, your creative costs … your infrastructure costs.

“When they report their cost, those companies actually have two layers of cost related to marketing,” Favier says. “The first one is just overall marketing cost, which actually includes UA spend, but also the cost of the team, etc. And this figure is also reported. It’s obviously higher than the user acquisition spend because it embeds it. So that’s also a way to assess a little bit, probably either the size or the cost of your team as compared to your revenue.”

Also: retention benchmarks

One other benchmark that is interesting for mobile marketers: MAU to DAU ratios. This is a good way to evaluate the stickiness or retention of your app, Favier suggests. In the social casino space, that’s typically 17-25%, so out of every 100 monthly average users, 17 to 25 of them are also daily average users.

Higher, of course, is better, but having these numbers are a guide can be valuable when setting goals for your app.

There’s more, too.

“When it comes to monetization, they disclose two very interesting figures,” Favier says. “The first one is the average revenue per DAU. So how much revenue do you generate per DAU, which is a very good KPI to look at. And they also disclose their daily paying users. So by comparing the daily paying users to the daily active users, you can know their payers’ rates. And that’s going to help you know which companies are super profitable.”

One final thing: this isn’t just relevant to the social casino space.

Any mobile gaming or mobile app space with a number of larger players who are public can be treated the exact same way: check the financial reports, summarize the data, and compare to your own internal data to benchmark your marketing efficiency. That’s available for user acquisition cost benchmarks and — as we’ve seen — much more.

Much more in the podcast

As always, there’s much more in the full podcast. Watch it above, or subscribe to Growth Masterminds on any of the podcast platforms you love, including:

Full transcript: user acquisition cost benchmarks (and much more) with Adikteev COO Clement Favier

Note: this transcript is AI-generated and lightly edited. It may contain transcription errors.

John Koetsier:

What can publicly traded gaming companies tell us about the mobile ecosystem? And can they help benchmark your user acquisition spend? Hello and welcome to Growth Masterminds. My name is John Koetsier.

There’s so much data in mobile. Most of it is your own, right? There’s a lot of ecosystem data, but there’s also super interesting insights in publicly traded mobile gaming companies. And they might reveal something about UA benchmarks and maybe optimal UA spend. That would be helpful for all mobile marketers.

Our guest today has studied this in some detail and he’s a massive industry insider. He’s a chief operating officer of Adikteev. His name is Clement Favier. Maybe I’ve got that right.

Welcome, Clement.

Clement Favier:

Thanks for having me and you got it right. I’m Clément.

John Koetsier:

Okay. Or else you’re too polite to tell me I got it wrong! So it’s all good. No worries. Excellent.

Give us a 30 second bio. Who are you?

Clement Favier:

Sure, so I’m Clément, I’m 36, father of a little daughter. And regarding app marketing, I joined the ecosystem, I would say eight to nine years ago. Pretty much when I joined Adeptive and I’ve been working with the company since then. So focusing a lot on app retargeting, which is definitely what we do at Adeptive. I started actually as a developer data analyst and the fact that I quite like to dig into data in general. Then moved to Berlin for three years when we acquired a company named TradMob which is actually the core of our retargeting DSP. And in the last couple of months I’ve been working more on new business initiatives at Additive. So we’re working on a cross promotion product and we’re working closely with

John Koetsier:

Nice, nice, nice, nice. Now I can tell that you are a former analyst because the way we sort of got connected and this kind of started is you were posting some really interesting insights to your LinkedIn about some analysis that you were doing about publicly traded mobile gaming companies. When did you start looking into this?

Clement Favier:

Well, I’ve always, let’s say, personally been a bit curious about the information you can get from public listed companies. I also have a little bit of a background in finance and the fact that I’m totally okay with looking at annual reports and getting insights into that. But that’s also something we integrated within Adikteev.

We have a corporate analyst who is working with us now. And we think it’s very helpful to basically bring knowledge to the whole company in the market, analyze the trends and basically say see what kind of insights we can extract either from public earnings of companies but also from generic market reports that you can get from a Singular, AppsFlyer, or whatever company who is releasing great insights on the either gaming or app tech market.

John Koetsier:

I’m impressed because I delve into significant quantities of data, you know, and do a bit of analysis here and there in what I do for some of my reports and stuff like that, but spreadsheets for finance and financial data … I’m like, what the heck is this? I don’t get it. I don’t understand it. I hate it and I stay away from it, but thank you for looking at it for us. What companies did you look into?

Clement Favier:

So our scope of research, let’s say, is mostly focused on gaming and mobile gaming companies, which is actually interesting because if you look at overall, you would probably say there’s about 50 companies that could be associated with gaming in general, even more than that, but I’m quoting, you know, what some banks can tell you when they send you reports report and things like that. So it’s a probe, yeah, approximately 15 total. But the question then is, is everything interesting for me? And probably not, especially if we’re talking about app growth. So for instance, companies like Electronic Arts or Activision Blizzard in general, you might think it’s relevant for your market.

But for instance, for EA, only 15% of the revenue is mobile. So it’s probably not a great proxy for looking at the app market. For Activision it’s a bit more, it’s like one third approximately. But that’s definitely something you need to look at. And if you want to dig into what is our peer set or the comparable companies that we think are more mobile focused, I would say it’s between 10 to 12 companies.

John Koetsier:

And give us some names?

Clement Favier:

Yes indeed. So you would have quite a lot of casino companies, Social Casino. So you have Huuuge Games, Wgames, Playstudios, Sciplay. There’s also Aristocrat with its division, Pixel United, which is the mother company of Product Madness and Big Fish. And there are also some other suspects like not in the social casino but more traditional gaming like Rovio, Modern Times Group which is like play simple, Stillfront, also BigBig Studios obviously, and Netmarble for instance.

John Koetsier:

So it’s very cool because as I said off the top, there’s a ton of data in mobile gaming, but you don’t — for private companies — have access to a lot of data on how much they are spending on marketing? What is their overall revenue? What’s their profitability? Other things like that. And metrics like that in different forms and different ways are usually available for publicly traded companies. So what did you see? What did you find?

Clement Favier:

Yes indeed, it’s very interesting. There are different ways to look at the data. And I would say what we definitely look at is, first of all, revenue trends, which gives you a good proxy of how the market is evolving overall. So the latest information we get is actually from Q4, because you know there’s usually a little bit of a delay like one, two months before they publish their results. In terms of the revenue, it’ll just depend on each company. But overall, in Q4, they actually grew slightly. Those companies, as compared to one year ago. So that’s actually interesting to see. For instance, SciPlay or PlayStudios, they grew over 10% in Q4 2022 versus the prior. Playtika was the only one in the social casino space that actually decreased in terms of revenue … minus 3%. And yeah, that’s one way we look at those data.

Another way to look at it, which is quite important, is user acquisition spend, because we’re a mobile marketer, and that’s something we’re very interested in. So first of all, not all companies disclose their US spend.

Some do, some don’t. You don’t necessarily know exactly how it’s computed.

Some will label it as advertising cost, some will label it as user acquisition spend. So you usually get in those reports a definition, so you assume it’s definitely mostly money that is spent on getting installs and probably a bit of retargeting as well. Here it’s pretty much aligned on how much those companies are actually spending on marketing, I would say a rough average would probably be between 25 to 28%. And it goes from 24% of revenue that is actually allocated to a user acquisition span. That’s the case for Play Studios and CyPlay. And it goes up to 39% for Modern Times Group, for instance.

But this one seems to be a bit of an outlier. All other companies are in a very close range between 24 to 26 percent.

John Koetsier:

It’s interesting, interesting, interesting to hear that data, right? And you have to apply some wisdom to that as well, because companies are in different stages. For instance, I’ve seen some companies, I think that the Calm, Headspace type of meditation space was, is an example of that where they went crazy on UA spend for a couple of years and then they went into now we’re going to take profits … and we’re not spending so heavily on user acquisition, and we’re actually just taking in a lot of revenue and banking a lot of profit. So you can have that mechanic going on.

You can also have the mechanic going on where maybe you’ve got younger, smaller gaming startups that are spending like 100% of revenue or something like, because they’re just in the growth mode, growth phase, they have some capital, some VC capital, and they’ve got to get to a certain level.

And then you might have some really established players, maybe a Supercell comes to mind. You know, let’s say, you know what? We have all the growth we want organically or most of it. And we have this amazing player base that just never leaves. We can’t kick them out, right? And so we don’t have to spend the same amount.

Talk a little bit about your thoughts around that. You know, what is the optimal spend and how that relates to maybe the life cycle of a company in mobile gaming.

Clement Favier:

Yes indeed, that’s a very good point. And I would say that for those companies I mentioned earlier, I think that all of them are profitable with a positive EBITDA margin, so basically profitable. So you could say that they’re all growing obviously, but also in a mature stage. So they think they’re not overspending and those are really considering their user budget very carefully and looking for profitable user acquisition. So this benchmark of 24 to 26% of revenue allocated to user acquisition seems to be really something that’s sustainable over the long term and that can be taken as a good proxy.

Obviously, if you are very new with your first to squeeze a little bit your profit margin at the beginning. We know that it usually takes time to beat the game and obviously get returns out of that. So to make your game known, increasing the store ranking, et cetera, you might have a bit of an overspend at the beginning. But I think that most gaming marketers would always look at profitable user acquisition spending which probably might be a little less the case in some other verticals where branding is definitely a bit more of a hot topic.

John Koetsier:

One thing I like about your analysis is, despite not knowing exactly in every case what is bundled into marketing spend and user acquisition spend, there’s a sense in which it’s a truer measure.

Because if you just look at UA spend in terms of CPI or something like that, right, that’s probably the bulk of it. But you have people. You’ve got infrastructure. You’ve got data costs, you’ve got tools that cost as well, and all of that layers on top of what you might spend, $3, $4, $5 for a person to actually click a button and install your game. So that sounds super, super interesting.

Anything else that you found that might be instructive for other UA managers in gaming or elsewhere about doing their jobs?

Clement Favier:

I think what you just said is actually a very good point because when they report their cost, those companies actually have two layers of cost related to marketing. The first one is just overall marketing cost, which actually includes UA spend, but also the cost of the team, etc. And this figure is also reported. It’s obviously higher than the user acquisition spend because it embeds it. So that’s also a way to assess a little bit, probably either the size or the cost of your team as compared to your revenue.

So basically, every marketing cost that’s not spend as a percentage of revenue, would probably also be a metric you could look at in order to benchmark your company against others. Again here, little accounting tricks because you don’t know exactly people are counted in marketing team, et cetera, et cetera. So it’s always, but that’s every benchmark should be taken with a grain of salt for sure. But that’s also something that’s very interesting.

Other KPIs that I find interesting as well from those public statements … you can get a few insights on retention as well as monetization of those games. So they do usually disclose a couple number of additional KPIs, which can be useful in order to assess that. They would usually disclose the number of daily active users and monthly active users. So just, you know, the DAU to MAU ratio would probably be a good proxy for either stickiness or retention.

For instance, here for social casino, if you’re in a range of 17 to 25% of the DAU to MAU ratio, you’re probably in a good spot.

And when it comes to monetization, they disclose two very interesting figures. The first one is the average revenue per DAU. So how much revenue do you generate per DAU, which is a very good KPI to look at. And they also disclose their daily paying users. So by comparing the daily paying users to the daily active users, you can know their payers’ rates. And that’s going to help you know which companies are super profitable.

And if they are profitable by getting a very high number of payers in proportion of total, or if they are actually managing to milk, let’s say in a way, the maximum amount of money of each payer. So is it coming from the value or is it coming more from a good conversion rate and a big payers base? So that’s actually quite interesting to look at in order to understand a little bit the dynamic.

And then as a mobile marketer, you could say, okay, so if I want to know how to maybe increase my payers conversion rate, maybe I should look more at this company because they seem to be the best at it. to look at how to increase my average order value. I should probably look more and benchmark these companies because they seem to be the best at it. So those are additional sides that I think are quite useful in order to educate which company you should research or which topic.

John Koetsier:

I love that. I love that because I mean, they have to disclose a certain amount of data. They also want to disclose a certain amount of data because they want investors to be excited about their company. Look at the number of users we have. Look at the number of paying users we have. So, you know, they need investors to be excited about their company because they want their stock price to go up. So they’re releasing that data, then you can look at the results that they’re getting, then you can play the game. You can get engaged and you can see, okay, how they do it. What do they do? What are the mechanics? How does it work? All that stuff … and see what’s going on there.

When you said daily paying users, is that daily users who pay or is it daily users who pay every day?

Clement Favier:

It’s daily users who pay. Usually they would disclose the exact definition in their annual report. So I would probably circle back and give you a more accurate answer. But usually it’s average daily users who pay.

John Koetsier:

Interesting because I was thinking wow if they pay every day I’m like whoa I don’t do that in my mobile game I’m like …

Clement Favier:

No, no, definitely not, definitely not. And just to give you an example of this conversion rate of daily paying users, again, daily active users, again, for social casino, it would be in a range of 2.5% to close to 5% for the best in class.

John Koetsier:

Okay, okay, so let’s capture those KPIs just for a second here. One of the ones that you mentioned earlier was MAUs, monthly average users to DAUs, and that was about 17 to one.

Clement Favier:

So yes, the ratio of DAU to MAU, I would say you’re in a very good spot if you are at 25% on at least on social casino, but a range would be 17% to 25%.

John Koetsier:

MAUs, so 25% of your MAUs are DAUs. That’s awesome. And then what was the ratio again for DAUs, daily active users who are payers? Was that about two to 5%?

Clement Favier:

Exactly, 2 to 5% here. Again, this is mostly for social casinos, which is where we have the most public companies. But it gives an indication for sure. It would be very different, obviously, from one genre to the other.

John Koetsier:

Right, right. Okay, so when are you gonna do all the genres?

Clement Favier:

Yes, because we’re liking our public listed companies, right?

John Koetsier:

And Clement is quite like, I don’t have all that kind of time. I have a company to run. But what you’ve done at least is you’ve shown the way that a significant company that’s interested in benchmarking themselves in ways that they can’t do with generally publicly available data from private companies, they can take this approach, they can look for companies that they care about and they can look for that and they can get that data and they can apply it to their own and see how they match up.

Clement Favier:

Exactly, exactly. And I would probably add a little caveat is that those are obviously only indicators to be taken with a grain of salt.

And I believe that probably one of the best benchmarks is your historical data and try to be improving. To that list, you know that’s 100% comparable. You know your scope. So obviously your number one driver should always be better than your previous iteration. But yeah, again, to get a sense of probably where you get the biggest opportunities to improve is definitely a good thing to look at.

John Koetsier:

Wonderful. Clement, thank you so much for sharing this.

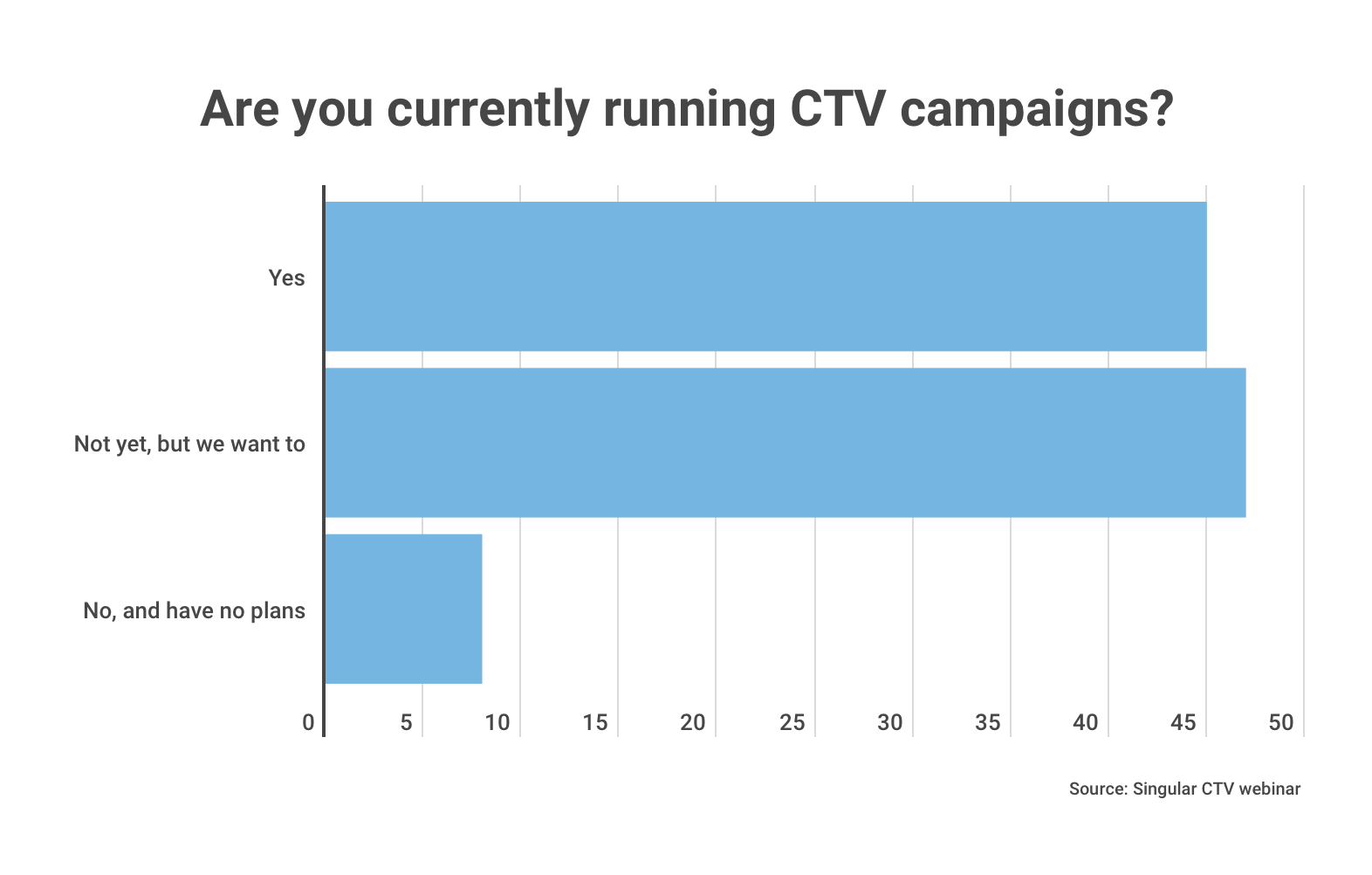

Most mobile marketers are interested in running ads for their apps on CTV. In fact, in our recent CTV-focused webinar, 45% of mobile marketers said they were already running user acquisition CTV campaigns. Another 47% said they weren’t yet but wanted to. You don’t have to know much calculus or trigonometry to infer that 92% of the marketers we asked are deeply interested in CTV ads for mobile UA, while only 8% are not.

So what are the biggest blockers for the 47% who want to run UA on CTV, but haven’t?

Cracking the code on CTV: the experts

Our recent webinar included experts from InnoGames, tvScientific, M&C Saatchi, and Moloco sharing details on the growth of CTV and how mobile marketers are using connected TV advertising to grow their apps. They are:

Bridget Hall Group Account Director at M&C Saatchi

Jake Richardson Head of CTV Strategy and Partnerships at Moloco

Ashley Parducci VP Client Success at tvScientific

Sidra Sattar Senior Marketing Manager at InnoGames

Evyatar Ram VP Product at Singular

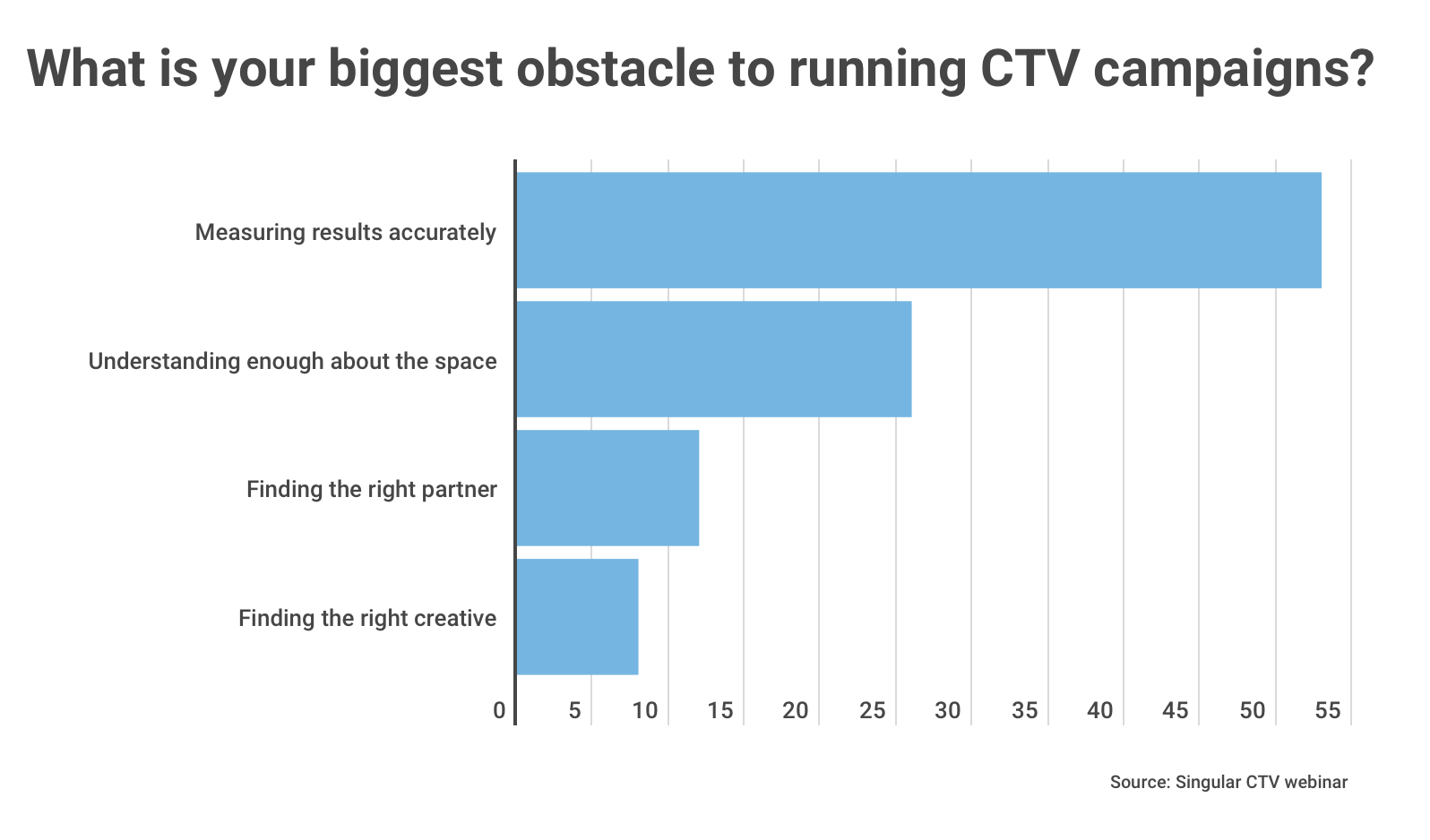

One of the first questions we asked the hundreds of attendees: what are your core challenges with running mobile user acquisition on CTV? Here are the four answers they gave:

Measuring results accurately

Understanding enough about the space

Finding the right partner

Finding the right creative

Clearly and unsurprisingly, measurement is the biggest challenge for CTV and user acquisition campaigns. But a second and also major factor is simply acquiring a level of understanding about the space.

Let’s look at each one in detail …

Measurement: measuring CTV-assisted user acquisition is hard

CTV is inherently difficult to measure because it’s typically cross-device, says Singular’s Evyatar Ram: the ad is on the big screen, the app you install is on the little one.

Most people are aware of that — and aware that CTV attribution is typically probabilistic based on IP addresses — but most aren’t aware that there’s a major difference between the user journey via mobile app ads on mobile and mobile app ads on CTV.

“I think the second challenge is that oftentimes the CTV touchpoint … will not be the last touchpoint that that user went through,” Ram says. “It’s very typical that you see the ad on your TV and then you go to your phone and you probably search for it and it’s pretty likely that … you’ll actually interact with another ad on the way to that install.”

So last-click or last touch measurement isn’t necessarily going to accurately reflect the value of a mobile app publisher’s ads on a streaming service, meaning more sophisticated measurement is required.

Understanding: learning a whole new universe is hard

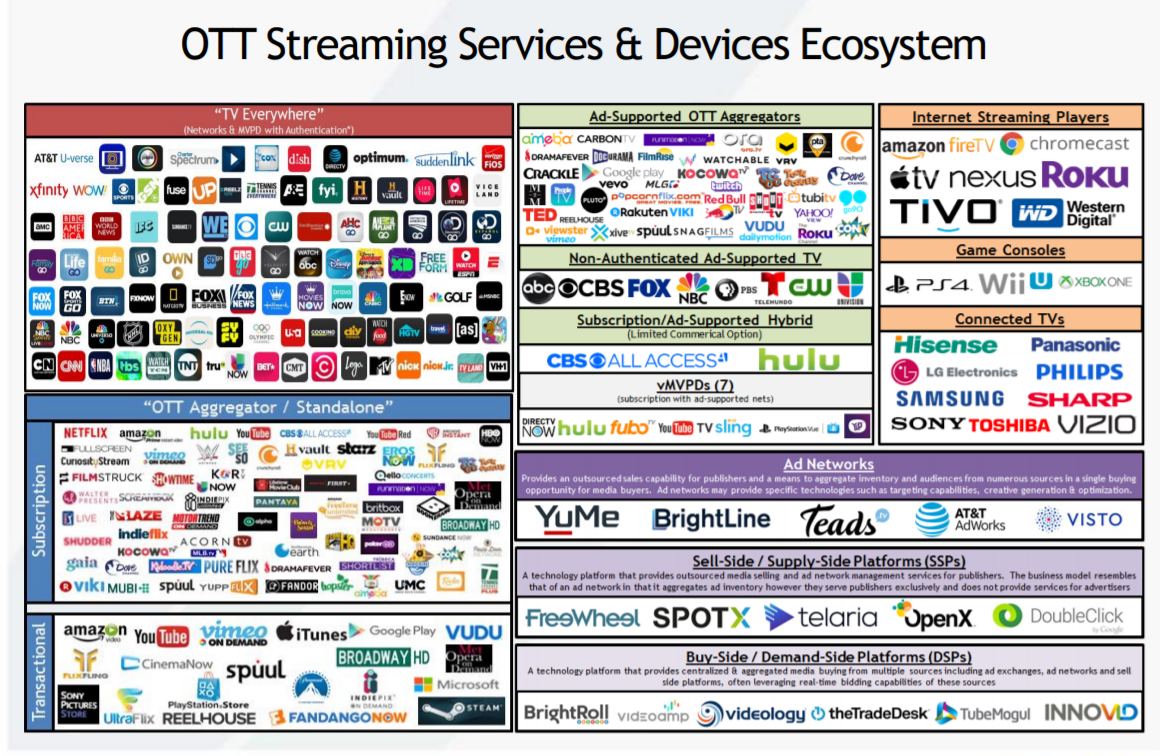

Mobile marketers are used to change, used to acronyms, and used to needing to re-learn their entire jobs 10% at a time pretty much all the time. But CTV is a whole new universe.

There’s CTV, there’s streaming, there’s SVOD, there’s AVOD, there’s TVOD, OTT, and that’s just the beginning.

To make it worse, it’s not always simple: what’s a streaming service versus a channel versus a platform? What’s hardware? Which are software? And which are two or all of the above all at once? Another major change: mobile marketing has calcified around just two global mobile operating systems, and just two global app stores. (That could be about to change, thanks to the Digital Markets Act.) CTV has many platforms, many players, and complex interactions.

Here’s just one market map of the space, with scores of logos:

Ad load is different too: from pretty heavy in mobile apps to pretty light — a few slots an hour — on CTV and streaming.

Buying follows some familiar models, but is also not identical.

“There are really two main ways of buying CTV inventory,” says M&C Saatchi’s Bridget Hall. “Programmatic is a more automated approach … Roku, Amazon Fire TV, they will have a bucket of their inventory that is offered on an open exchange and then they might have other premium placements that you can only transact or buy from if you’re working with them direct.”

In general, programmatic is good and helps you focus more on audience discovery, Hall says, while direct only targets a very specific audience (though it might offer better first-party data). Targeting is very different: with geographical data on subscribers, “when you go to CTV, if you really wanted, you could buy one household,” says Moloco’s Jake Richardson.

Also new: spend requirements.

Some experts recommend a minimum $25,000 monthly spend, which puts CTV advertising in the hands of only a few very massive mobile publishers. Others say you can start with a more modest budget to test the waters and check for incrementality.

Right partner: doing user acquisition on CTV requires good advice

Finding the right partners is always a challenge.

“We have existing partnerships … we are going to talk to them first,” says InnoGames Sidra Sattar. “And they are always the partners that approach us first whenever there’s something that’s coming down the line, a first to market, first to test when it comes to alphas and betas. That is a great place to jump in.”

If you don’t have partners that specialize in CTV, the partners on this webinar including M&C Saatchi, Moloco, and tvScientific are a good place to start.

The best partners, as always, start with the client’s needs, not their own capabilities.

“Where I always start with a client is to understand what the goal is and that can take some time,” says tvScientific’s Ashley Parducci. “It might start as a performance goal but then it turns out it’s actually an incrementality goal.”

Right creative: always hard

Of course, finding the right creative is not just a challenge for CTV-focused user acquisition campaigns. It’s hard in any ad campaign. But CTV creative and mobile app creative don’t often mix well.

Ad formats are all video, of course, but range in length from 15 seconds to 30 seconds to even longer. And it’s not clear your videos from in-app video ads will play well here.

“Think big screen,” says Sattar. “If you are a mobile-first advertiser, what you’re doing on mobile ads may not translate.”

One funky oddity about QR codes, which have been kind-of-a-thing-while-not-a-thing since Coinbase’s Super Bowl commercial that was “so popular it crashed the app” …

They don’t work

They work

Moloco’s Jake Richardson explains:

“QR codes definitely work, but if you treat them as a clickthrough, they do not work because the studies have shown it’s less than 0.5% of people who actually get their phone out on time, scan the QR code, and get to the website … but for some reason, strangely, if you treat it as a view through attribution, a QR code increases engagement: people see the ad and they think, ‘Oh, interesting. This is a legitimate company. They’ve got a site that I can land on. I’ll go search for it. I may not use the QR code. I’ll go search for it.’ And that increases engagement with your brand.”

In other words, they don’t work for direct marketing or performance marketing, in a sense, but they do work for brand.

But if you don’t measure them in the right way, you’ll never know it.

Of course … much more in the full webinar

While the survey we mentioned off the top that indicates over 90% of mobile marketers are doing or interested in doing CTV ads is clearly not a representative sample — it was a webinar, after all, about CTV — it’s yet another example of a groundswell of interest in CTV ads.

89% of households are currently active streamers, Hall says. And that’s growing year over year. Ad spend is also up: about 27% annually.

That the mobile growth industry is hooked on growth is not shocking. Water, in breaking news, is also wet. But how gaming user acquisition experts recruit new players for their games is evolving in 2023, and I had a chat with Mistplay chief growth officer Jason Heller about what user acquisition for mobile games looks like from his perspective.

“User acquisition is a drug that we’re all hooked on,” Heller says in the latest Growth Masterminds episode. “The dirty secret in gaming is significant churn, right? So you have to keep feeding the beast.”

Feeding the beast is, of course, spending more and more money every single month to fill the top of a very leaky user acquisition bucket to replace players who churn. All good, except that less churn and more retention would result in higher LTV and better profitability. In additional utterly shocking news, the less game publishers have to spend on UA the more they can pocket.

Mobile game growth options

So what do you do?

Try to boost engagement and retention (like everyone else)

Cross-promote games across your studio’s titles to change external churn to internal churn

Buy smaller studios to acquire their players and then work on #1 and #2

Make something so amazingly good the whole world just downloads it on general principle, plays it every day, and never leaves (just a little hard and requires just a smidge of luck … but keep trying)

Build a rockstar ASO and SEO and influencer strategy to funnel 99.753% of all even semi-related online interest directly to your app

And … keep paying the piper (AKA the user acquisition ad tax)

There’s value in all answers, but industry experts know: advertising exists for a reason.

Breaking through the avalanche of information dumped on Humanus Digitalis in 2023 is hard. Awesome ads in excellent contexts delivered via smart technology have a shot.

Given you’re still going to need to boost user acquisition for mobile games with ads, what does Heller think works this year? I wanted to specifically ask him, because Mistplay (which is about .01% the size of a Meta or a Google … don’t fact-check me on that) did surprisingly well in this year’s Singular ROI Index. As in: 14 mentions in the total document. And, a staggering 9 rankings in various top network lists, including perhaps the most important ranking of all: the top overall list for all-round excellence by a mobile ad partner.

How does a small ad network compete?

And, more importantly, do so well?

Briefly, in Jason Heller’s words, by play-to-earn, by loyalty, and by community.

Yeah, play to earn. But not that kind of play to earn

A good chunk of Mistplay’s success might be attributed to play to earn, which Heller is trying to reclaim from the web3 crowd:

“I’ve stopped using that phrase as much as I would like, just because the web3 companies have kind of hijacked it a little bit and it’s a very really different kind of beast, right?” Heller says. “There is a movement of play to earn in web3, but it’s a speculative crypto/NFT kind of market. It’s not what we do, which is help game publishers reach users who actually want to play their games, spend time and money in those games, and earn based on the time and money they spend in games. So it’s a totally different beast, but that is what we do: we are a play to earn platform, and that’s the value prop to the user.”

Rewards, in other words, matter in user acquisition for mobile games. And, of course, for retention. But building the community side is equally important in a privacy-first SKAdNetwork era on iOS, and Privacy Sandbox on Android.

First-person data driving user acquisition for mobile games

Mistplay develops a first-person relationship with gamers that persists over time and throughout their gameplay in multiple mobile games. That first-person relationship means that gamers earn rewards for their gameplay in multiple games — a strategy I’m baffled that more studios don’t adopt internally — and means that Mistplay has strong privacy-safe data on what games individual players like.

And which ones they buy digital goodies in.

“The interesting thing about being a UA source with a ton of first party data — because we’re not a network, we’re a community — we get a little bit of luxury that not everybody enjoys,” Heller says. “We can follow a user along their journey. We can re-engage somebody when they stop playing a game on behalf of a client.”

That’s important right now because in the middle of our 3 to 5 year ATT and Privacy Sandbox transition, mobile game publishers are also faced with a double whammy courtesy of a declining economy. The challenge is a profitability squeeze as CPIs are going up while ROAS is going down, mostly due to declining in-app purchases.

Live ops for “retained revenue”

Interestingly, Mistplay is planning to release a live ops tool in the next 6 to 12 months that will leverage what Heller says is the platform’s “uncanny” ability to predict D7 revenue and in-app spending to serve UA clients better.

And to drive long-term value.

Not D7. Not D30. Think months, even years of “retained revenue.”

“We’ve got massive aspirations,” Heller says. “If you look at the games that really are driving what I would call retained revenue: how much revenue is retained without having to go out and spend tens of millions of dollars on user acquisition … like Roblox, right? If you look at the day 30 retention trend of a Roblox versus let’s just use a Coin Master, or another great, amazing, high grossing IAP game, the difference is not day 30. The difference is day 180, day 360 and probably multi-year cohort life cycle. It’s amazing how they retain users over the long term.”

Not everyone can be a Roblox or a Minecraft or a Fortnite or a Clash of Clans, of course, as Heller readily acknowledges.

But that’s the standard he’s aiming for: retained revenue via smart user acquisition and — even more so — great gameplay and community and value in an experience that players rarely churn from.

Much more in the podcast!

As always, there’s much more in the full podcast. Watch it above, or subscribe to Growth Masterminds on any of the podcast platforms you love, including:

Three-quarters of marketers still rely heavily on third-party cookies, according to a new Adobe study. And 64% of marketers plan to increase spending on cookies this year: a technology we know is going away relatively soon. But next-generation marketing measurement and first-party data are big parts of the solution to the deprecation of all marketing identifiers: third-party cookies, IDFAs, and GAIDs.

We don’t tend to talk a lot about third-party cookies on the Singular blog, mostly because mobile marketers have traditionally focused on in-app advertising to grow their own mobile apps.

However, modern mobile marketers are looking everywhere for audiences and impressions and conversions, including CTV and the web. So measuring cross-platform marketing and mastering cross-device attribution is important … and understanding where the third-party cookie stands starts to matter.

“Two out of five leaders are not placing a priority on preparing for a cookieless future over the next,” says Ryan Fleisch, Adobe head of product marketing for real-time CDP and Audience Manager. “Obviously the flip side of that equation: it is great to hear that, you know, roughly 60% plus are … but we’ve been doing various research reports on this for the past few years and we haven’t really seen that much of an increase of readiness.”

Who’s still using third-party cookies?

The nearly 2,700 marketers Adobe surveyed are in 8 countries: the United States, United Kingdom, Germany, France, Australia, New Zealand, Japan, and India. 75% still use third-party cookies extensively, and 45% of marketers are spending at least half their budgets on cookie-based activations, Adobe says.

In New Zealand and India, there’s an even higher reliance on third-party cookies: 82%.

It’s not like marketers don’t know this is a problem: they know third-party cookies are going away at some point.

And they’re very concerned about it. Globally:

16% say this will “devastate” their business

23% say they’ll be significantly harmed

37% say there will be a moderate negative impact

It’s even worse in some regions. In APAC countries, minus Japan, 80% of marketers say third-party cookie deprecation will harm their businesses while 34% say it will devastate them.

Consequences of losing third-party cookies

What will happen when third-party cookies go away? To put it briefly: higher spend and lower return.

“I think [you’re] going to have to spend more to recognize the same results if you don’t have the right mechanisms in place,” Fleisch says. “The good news is … with the right technology in place, with the right first party data strategy and with the right measurement. that can largely be solved for. But if brands aren’t prepared, they can expect to see a big drop off from what they would’ve previously expected in performance.”

First-party data is one of the biggest weapons marketers have in the post-identifier marketing ecosystem, Fleisch says.

That, of course, is not something marketers haven’t heard before. But — as Fleisch acknowledges — it’s also easier said than done. It’s also not an instant solution, and just to make it a bit tougher, it’s exponentially harder for smaller companies, start-ups, and app publishers who are just starting than it is for larger brands.

Once that data is collected in privacy-safe ways, however, it’s also a matter of storing it, structuring it, and making it available for action. That’s where customer data platforms come into play, Fleisch says.

“To me it really comes down to the CDP at the center … the CDP is the core of the functionality, but with a massive importance on making sure that that doesn’t create another silo in and of itself, and is actually connected to the engagement systems and the insight systems that you’d be looking to use to make a virtuous circle.”

Another weapon he cites: consent-based lists.

But there’s also better measurement …

The third tool Fleisch says can help fight the degradation of ad effectiveness due to loss of third-party cookies is better measurement. And as we’ve seen at Singular, that’s perhaps the tool that is right in the middle of the most change and innovation right now.

“The third piece then is around measurement,” Fleisch says. “So if I’m spending dollars on Facebook or Meta, Google, TikTok, Snapchat … I call them walled garden environments … how am I actually recognizing that spend being attached to the conversions that are happening on my site?”

Or in my app, of course.

Fleisch is right: measurement is critical. But not your daddy’s measurement.

The measurement of the future is much richer, more nuanced, much more varied in data sources than old-school IDFAs, GAIDs, and third-party cookies. And much richer and more nuanced than just SKAdNetwork and (eventually) Privacy Sandbox for Android alone. Instead, think SKAN and first-party and Privacy Sandbox and cost/spend data and delivery data (CTR/impressions, viewability, etc) and IDFA and cookies (where available and permitted), and CTV and cross-device and console and PCA (private click measurement) … all together.

Multiple datapoints. Multiple measurement methodologies, including deterministic (SKAN) and probabilistic (MMM), granular (IDFA) and aggregate (Privacy Sandbox for Android). Multiple ways of modeling. Multiple ways of estimating reality with as high fidelity as possible.

From our CEO Gadi Eliashiv’s recent blog post on this:

“Instead of relying on a single view of performance (which already today is not really a possibility given the data fragmentation in iOS), there will be multiple views that employ multiple methodologies using all the data mentioned above, and serving different purposes.”

That’s complicated, but it’s actually good news if you’re a mobile app publisher or a startup business. Because you probably can’t really compete on the basis of first-party data. Maybe you don’t have enough of it. Possibly, you don’t want to collect all of it. Plus, there’s also some inherent risk in storing it, and new hassles of having to delete it upon request as per GDPR or other legal requirements.

So new forms of measurement solving the problems of losing advertising identifiers is a ray of hope.

How performant are new solutions?

The biggest question, of course, is how performant new advertising measurement solutions will be after third-party cookies join IDFA and GAID in the recycle bin of marketing history.

For Fleisch, it’s not necessarily worse. Just different.

“I think it really comes down to a trade off in quantity versus quality,” he says. “I’ve gone on before [to third-party cookie data vendors’ sites] and seen that I’ve fallen into three different simultaneous age groups and 20 different interests that I would’ve never considered … so I think in a lot of cases there’s not always the pinpoint accuracy that marketers would look for. So I think as we look to a world without cookies, yes, you’re not going to have the same volume of data, but you can rest assured that the quality of that data is gonna be higher … and you know that you’re marketing to someone with their consent, with their preferences at the forefront.”

That’s great, in the case of permissions and first-party data.

I also tend to think that better measurement using all available signals and multiple methodologies can actually outperform old-school last-click single-data-source measurement. That’s perhaps making a virtue of a necessity, but using so many more diverse datapoints and methodologies should help model a better version of reality.

And that’s a strong comfort to brands, companies, and app publishers who don’t have — and maybe don’t want — the massive volume of first-party data that enterprise brands might enjoy.

If you’re not great at Apple Search Ads, you’re missing a significant amount of high-quality traffic and major growth opportunities, says Splitmetrics CMO Olga Noha in a recent Growth Masterminds podcast. Even more, you’re potentially missing out on massive organic uplift: Noha says that Apple Search Ads can boost App Store optimization by up to 4X.

“Before going for Apple Search Ads, the game ranked in the top 10 for 24 keywords,” Noha says about a customer’s game. “After launching the Apple Search Ads campaign, it started to rank in the top 10 for 112 keywords.”

While of course your mileage may vary, what’s happening here is that as people download and install an app or game based on relevant keywords — even those driven by paid ads — the conversions for those keywords grows. And that drives better position in organic search results, Noha says.

The bonus?

You can target ASA campaigns to your best users. Or build conquest campaigns to win players over from another game. Or scoop customers most likely to convert. Since you can then potentially achieve high clickthrough, install, and engagement rates, you’re sending signals to the App Store ranking algorithms about the quality of your app … and where the store algorithms might want to rank your game in search results for various keywords.

That’s one reason Noha says being good at Apple Search Ads is “absolutely crucial” for mobile marketers. And that pairing ASO and ASA is an integral part of a holistic mobile growth plan. When aligned, apps see improved visibility, increased organic installs, optimized conversion rates, and lower blended user acquisition costs.

That’s likely one of the reasons why Apple Search Ads ranked second in iOS ad spend capture for Singular clients, as seen in our latest Singular ROI Index.

Custom product pages: also critical

Another big driver of success in the App Store (and Google Play) is custom product pages, or app listings that are intentionally aligned to a specific target audience, or a specific feature or characteristic or use case of an app or game.

One app, Violin Lessons, built a custom product page to highlight a very specific use case: tuning your violin.

“The results they got were astonishing,” says Noha. “For the U.S. market, TTR [tap-through rate] increased almost twice, installs grew 2.5X, and the number of purchases boosted by 3.75X.”

Another client, PicsArt, used custom product pages to target specific audiences and segments with specific value propositions and messaging. The result: their best CPPs saw a 52% increase in conversion rates and a 153% increase in users entering free trials. At the same time, costs per trial decreased by 50%.

In other words, mobile marketers can’t NOT use custom product pages. They’re essential. And aligning them with ad campaigns, creative, and offers for specific audiences is a no-brainer.

Apple Search Ads: new placements

Apple Search Ads currently offers 4 different types of ad placement opportunities:

Today tab (ads on the screen everyone sees when they open the App Store app)

Search tab (ads on the Search tab before actually searching)

Search results (ads mixed in with search results after searching)

App listing pages (ads at the bottom of other app listing pages)

Today tab ads get a lot of exposure, as do ads on the search tab and those mixed in with search results. But I personally haven’t been super-excited by ads on app listing pages. There’s of course the competitive concerns — my competitors can advertise on my app listing pages — but more importantly, I’ve thought … who scrolls that far down the screen?

Turns out, I’m probably wrong about that.

“What is important about these placements is that they drive highly engaged users who are already considering which app to download,” says Noha. “For some reason, they haven’t downloaded the specific app that they were looking at, and that is your chance as a developer to drive their attention to your app because the intent is there.”

They’re looking for an app like the one they’re on the listing page for, Noha explains. But they haven’t actually downloaded that one just yet. Maybe it doesn’t quite seem like it will meet their needs? Maybe it doesn’t seem like quite the right game?

Whatever the situation: here’s your chance to present your case that your app or game is a better option.

“This high intent and high quality of the users is key for me with this type of placements,” Noha says.

Apple Search Ads and pre-orders

I’ve talked to literally hundreds, if not thousands of app marketers. I’ve never talked — or heard them speak — about app pre-orders. But, it turns out, app pre-orders can be a great way to get your app off to a running start right at launch.

When chatting about where to use ASA in the lifecycle of an app, Noha says that before launching is a good option. And that’s one time, I’m betting, that most marketers don’t think about.

“We all know the case of using Apple Search Ads to scale apps,” Noha says. “But we also have cases of helping customers work with ASA at the pre-order stage.”

One app publisher in the photo and video category wanted to launch with a bang, so Splitmetrics identified 400 keywords that matched, launched an ASA campaign, and generated 2,000 app pre-orders. On launch day, that’s 2,000 phones that received the game automatically

“That basically helped to make the release day much bigger and also, eventually it helped to get promoted to a top one position in the App Store,” Noha says.

Much more in the podcast

As always, there’s much more in the full podcast. Watch it above, or subscribe to Growth Masterminds on any of the podcast platforms you love, including:

If you can’t measure organic lift and social metrics, you’re not getting a complete picture of marketing results. And you’re also unaware of how you are either boosting or impairing future ad reach, engagement, and results.

Recently I chatted with Aidan Quest, the CEO of influencer marketing network JetFuel, now Liftoff Influence. We talked about organic impact on TikTok specifically, where I learned that sometimes the best influencer-made ads get millions of views organically on the For You page.

As in, for free.

Social metrics, now in the Singular dashboard

That’s one reason Singular has recently added social metrics to Singular analytics.

“Every marketer wants all the data they can get for each campaign, and that includes organic multipliers and knock-on impact of your ad campaigns,” says product marketing manager Kelsey Lee. “This is a big step towards providing a more holistic picture of the organic benefits of paid advertising.”

To start, the social metrics available in the Singular dashboard will include data from:

Facebook

Instagram

Twitter

TikTok

For now, social metrics in Singular reports will be focused on 2 things:

Social engagement metrics: your organic results for follows, likes, shares, comments, and post saves generated as a result of your ads

Reach and average frequency metrics: details on the reach and frequency of your ads … so a total for how many people who saw your ads at least once, and the average number of times each person saw your ads

Available in the Metrics section in Reports & Pivots, the social metrics reports will show how many new followers you’ve achieved as a result of your ads on Twitter and TikTok. On Facebook, Instagram, Twitter, and TikTok, you’ll get post reactions and/or likes, number of comments or replies, number of shares or retweets, and the number of post saves reported by each platform.

Why social results of paid ads are not just vanity metrics

Here’s why this is not just interesting or nice-to-have data.

Research actually shows that the more engaging your social media advertising is and the more positive consumer’s attitudes to your brand are, the more likely people are to purchase. That is not a surprise. What the research also shows is that the degree to which social media advertising successfully engages its target audience also drives how likely people are to engage with your content in the future.

So social metrics in the Singular dashboard now provides a simple way to measure how impactful your paid advertising is not just in driving immediate performance, but also longer-term brand impact. In other words, now you have more ways to measure success than just immediate impact on sales.

Those sales, of course, are critically important.

But they are not the full story.

Because each time an ad campaign captures attention and engages potential customers, users, or players in a positive way, you’re literally improving future advertising performance. For brands that intend to be around for a while and who are looking beyond an immediate sale, this is important. And every ad campaign that doesn’t engage its target audience doesn’t just fail today, it reduces both future impact and future reach.

So success and failure have dual results, once today, and once in the future. Conversions today like installs, sign-ups, or revenue is great. But so is boosting future attention and action.

Social metrics, now in the Singular dashboard, reveal progress toward that goal.

A year and a half after the introduction of SKAdNetwork in iOS 14.5, most mobile marketers are still not comfortable with SKAN. But if you want to maximize your growth opportunities on the most lucrative mobile platform, getting good at optimizing ad campaigns via the data you can derive from SKAdNetwork is not optional. The key to getting there might just be the right SKAdNetwork tips from the right growth leaders.

That’s why we recently hosted the How not to suck at SKAN webinar, with experts from GameLoft, LinkedIn, Liftoff, Kayzen, and Singular.

Our panelists included:

Matthew Ellinwood, director of product management at Liftoff

Puneet Gupta, co-founder and CPO at Kayzen

Sandy Shen, mobile marketing lead at LinkedIn

Shannon Fishman, senior manager and paid mobile labs lead at LinkedIn

Vassil Georgiev, user acquisition team lead at Gameloft

Here’s a summary of some of the top SKAdNetwork tips that we learned …

What’s the hardest part of SKAdNetwork?

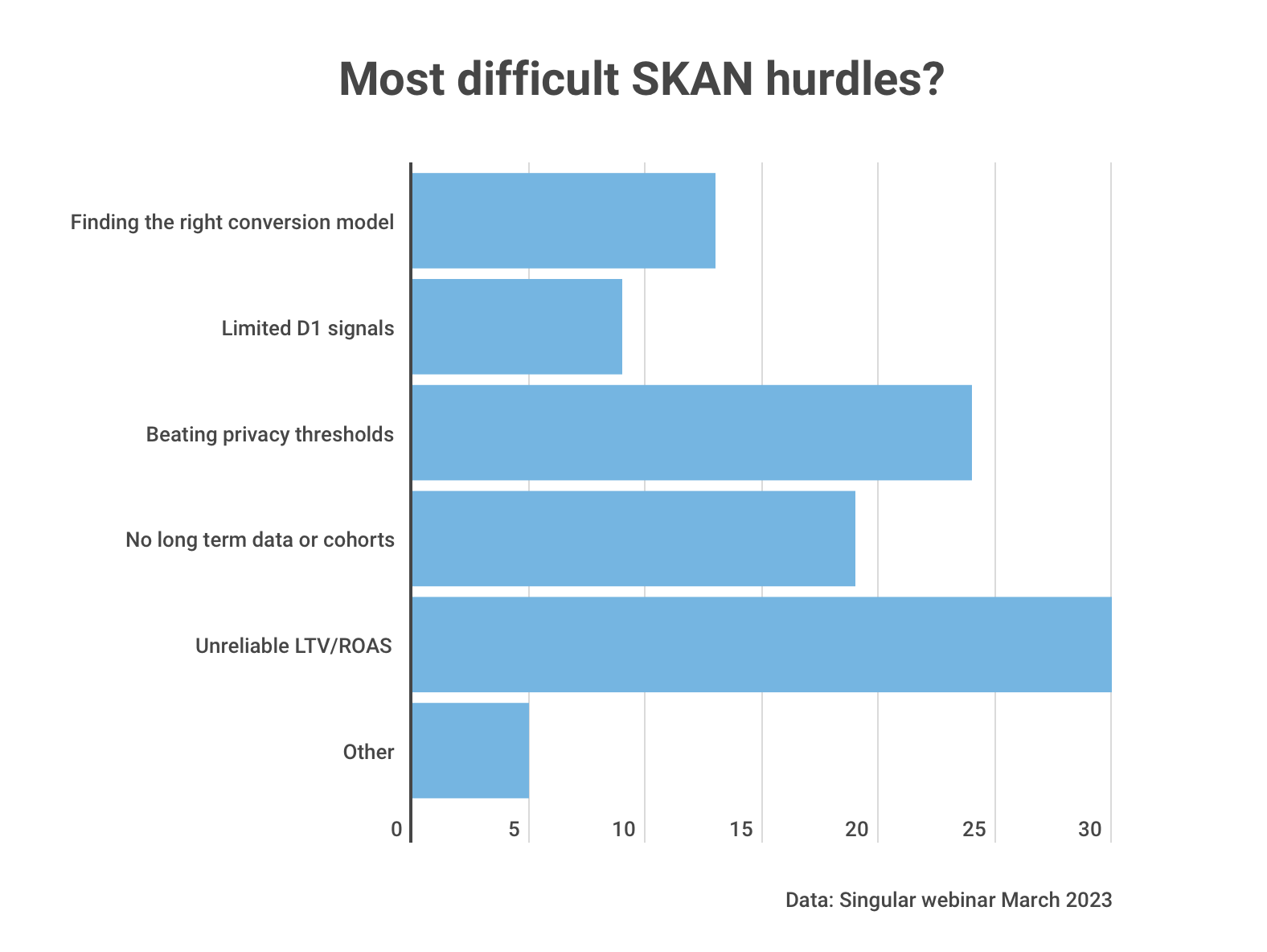

Achieving accuracy in LTV and ROAS predictions is the hardest part of SKAdNetwork, according to hundreds of growth marketers who attended the webinar. The second hardest part, not accidentally, is completely related: getting enough measurement data despite SKAN’s privacy thresholds.

In order of the most severe, the top five challenges with SKAN are:

Unreliable LTV/ROAS: 30%

Beating privacy thresholds: 24%

Finding the right conversion model: 13%

No long term data or cohorts: 19%

Limited D1 signals: 9%

As most user acquisition experts will agree, they’re pretty much all related. It’s hard to get reliable LTV or ROAS when you don’t have enough data, when the conversion model you’ve chosen isn’t predictive, and when you only have a very brief window of insight.

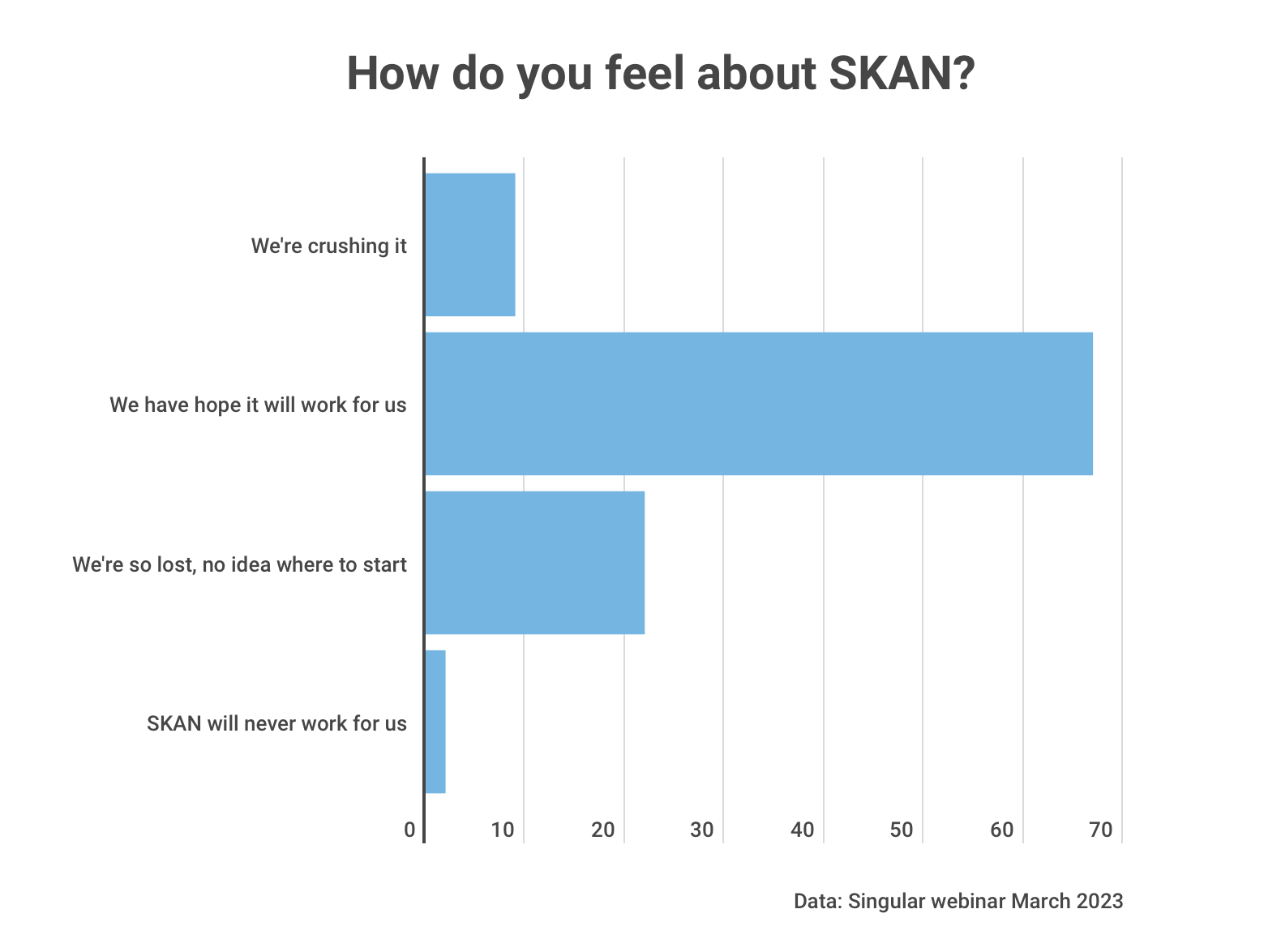

How do you feel about SKAN?

Unsurprisingly, that’s led to some emotional responses to SKAdNetwork, including some despair and some anger. We also asked How not to suck at SKAN webinar participants to tell us how they feel about SKAN.

A very small number of marketers feel like they are “crushing” SKAN. A fifth feel like they are lost, with no idea where to start. A small number — very small, fortunately — feel like there is no hope at all: SKAN will never work for them and their apps.

But a significant majority at least has hope:

We have hope it will work for us: 67%

We’re so lost, no idea where to start: 22%

We’re crushing it: 9%

SKAN will never work for us: 2%

I don’t have prior data, but I’m willing to go out on a limb: two thirds of marketers having hope that SKAN will work for them, that SKAN can be made performant for their user acquisition efforts … that’s significantly up from where it was a year ago or even 6 months ago. Which means that with the right SKAdNetwork tips, there’s a chance we can get the majority of mobile marketers feeling confident about their ability to grow their apps.

Feeding the hope: 15 SKAdNetwork tips from experts

1. Start with the right mindset

The old way you used to grow apps is over. IDFA availability is running around 20-25%, and it’s not going back to the 70-80% you had before App Tracking Transparency.

Understand that. Accept that. Lean into that. Get the right SKAdNetwork tips to make it work for you.

Then apply the resources you need to figure SKAN out, says LinkedIn’s Shannon Fishman:

“I think the biggest way that we have succeeded is by constantly testing and never giving up the hope that we can accomplish success with SKAN. I think part of that comes from really releasing the shackles of pre-SKAN mindsets and making sure that you have the right measurement, engineering, resources, and budget allocation to push forward your program goals.”

Release the shackles.

2. Zoom in to your app. It’s not just about marketing metrics

Marketing is all about the metrics, right?

No.

It’s also about knowing your app. Knowing your user journey. Knowing your players or customers, and knowing how they live in your app.

This has been a core change for Gameloft since SKAN, says team lead Vassil Georgiev:

“On the micro level, I can definitely tell you that my team has been zoomed out quite a lot from the user profile and persona as a whole. And right now, they are quite more zoomed into the user journey. And on a macro level, in terms of crisis, it definitely brought the different key stakeholders around the company like growth data science, the growth managers, and the game designers closer than ever.”

Understanding your app and what people do inside it to a very deep level helps you understand what’s core about your growth loops, what’s critical to measure in SKAN conversion models, and what features and fun to focus on in your ads.

3. Get the full team on board, not just marketers

Marketing metrics is a marketing-only problem, right?

Wrong.

It never really was, but especially in the era of scarce data from SKAN and soon Privacy Sandbox, it’s more important than ever to engage the entire team. Especially when you’re starting out and need to do some brain surgery to start making SKAN performant.

From Sandy Shen, mobile marketing lead at LinkedIn:

“We connect two sides of engineering to ensure everything looks correct … helping us avoid back-and-forth investigation between integration or campaign setup when there are no conversion values coming in. So it did take us a while to see conversions show up. But we can focus more on brainstorming campaign setup.”

Get all hands on deck: product, engineering, data, and marketers. Stay on deck through the implementation and testing process. Brainstorm together. It’s everyone’s job to figure it out and land the plane.

4. Be patient

I know it’s the least favorite thing for mobile marketers to hear. You’re in tech, which is fast-paced, and you’re in mobile, which is perhaps the fastest-paced part of tech.

But patience is critical.

From Sandy Shen again:

“Be patient, let your new campaign run for at least two weeks.”

When you’re testing new conversion models you need to let the old data flush out of the ecosystem to get a clean comparison. So you might have to restrict spend for a period of a month or more when you’re first implementing SKAdNetwork. Test on a fraction of your spend — while spending enough with the channels you select to surpass privacy thresholds — and go though some iterations.

When you’re happy with your results and can spend confidently, open the spigots back up.

5. Model conversions to fix missing data

When too much of your data is censored due to privacy thresholds, conversions and installs look very expensive: more spend spread over fewer events.

One of the most important SKAdNetwork tips, therefore, is to use tech like Singular’s SKAN Advanced Analytics to model missing data. Now your conversions and installs return to expected levels.

From Singular CTO Eran Friedman, speaking about a customer he worked with:

“What really helped them is the use of our SKAN advanced analytics product, which focuses on modeling conversions to basically eliminate the privacy thresholds and provide longer cohorts, seven-day runs essentially. And that finally showed them equivalent performance for the SKAN campaigns as what they were used to.”

This particular customer paused spending because the results were unpredictable. Metrics were unreliable. CPIs were off the charts. Using modeled metrics that lean on first-party data to provide estimated performance within specified confidence intervals changed everything.

6. Know what matters most

With free IDFAs for all, mobile marketers could measure almost anything and everything, and frequently did. And you could measure retroactively, to see what metrics might be more powerful.

Those days are gone. Now you have to pick specific events and/or revenue and use just a few data points to predict overall results.

From Sandy Shen at LinkedIn:

“On the LinkedIn side, we understand what matters most important to us …”

Before you can understand what matters most, you have to (see #2 above) know what people do in your app. Then study that and see what events have the most predictive power. Now you can start setting up conversion models.

This will get somewhat easier in SKAN 4, with more data. But it will come at the cost of significant added complexity.

7. KISS: keep it simple …

SKAN is already complex, and getting more so in version 4.

So keep it simple.

Again from Sandy at LinkedIn:

“After SKAN, we started to prioritize our existing metrics, and only kept a few. Because as we know, the more metrics you want to track, the longer delay you will see in your SKAN reporting.”

Pick the most important. Use SKAN Advanced Analytics to hedge your bets a little with mixed models so you get a few events and some revenue data. But don’t boil the ocean and try to every everything instantly.

8. Leverage Android visibility

There are some things you can learn on Android that might help on iOS. The obvious benefit: you still have full advertising ID visibility in the full scope of the customer journey with GAID.