Available in: English, Portuguese, Spanish, Korean and Chinese

Introduction and TLDR

Q3 2025 was the quarter of On-demand.

Ad spend surged again, and so did mobile acquisition prices. CPI soared, especially on iOS where impressions dropped, and iOS once again proved it’s the platform where marketers both pay more and earn more.

Utilities and On-Demand apps continued their breakout runs, especially Utilities on Android, while On-Demand apps grew fast on both platforms, and were the most in demand on both iOS and Android.

In Q3, Entertainment, Retail, and Education cooled off, but the Retail story is more complex than that.

Retail’s case showcases how user acquisition pros can plan growth efforts when installs are cheaper, prepping them for big holiday quarters like Q4. Given that Retail installs were the most expensive of all across both iOS and Android this past quarter, that turned out to be a pretty smart strategy.

Highlights and key takeaways

- Global ad spend jumped +24% on both iOS and Android as marketers ramped up for holiday seasonality

- iOS CPIs spiked +44%, the biggest increase in over a year, with more dollars chasing fewer impressions

- Retail remains the most expensive vertical, with iOS install costs up +61% QoQ

- Utilities are a massive growth engine with installs up 110% on Android

- On-Demand dominates app installs, leading all non-gaming verticals in installs on both platforms while also seeing an additional 14% growth

- Gaming rebounded, led by Simulation, Match, and Word genres posting double and triple-digit growth

- TikTok’s share of ad revenue grew faster than any other platform or ad network

- The monetization gap in some verticals widened as iOS drove 70–95% of revenue across most verticals, even with less than 25% of installs

- Health & Fitness is the most skewed vertical: installs split 50/50, but iOS drives 94% of revenue

- Utilities and Entertainment are the exceptions where Android leads both installs and revenue

The big story:

Mobile marketers are paying more to acquire fewer, higher-value users — especially on iOS. Android continues to deliver scale, but revenue growth is coming from Apple’s ecosystem, where high-LTV users justify soaring CPIs.

As always, data in this report is based on a significant slice of Singular’s data:

Author: John Koetsier

Data scientist: Gaston Laterza

Global ad spend trends

Global ad spend as measured by Singular is up again after being up 45% quarter-over-quarter in Q2. The biggest reason: seasonal spending.

In Q3, we’re ramping up for the end-of-year holiday season:

Ad spend up by 24.4%

Interestingly, while ad spend was up proportionately higher on iOS last quarter, this quarter is almost dead even:

- iOS: ad spend jumped 24.3%

- Android: ad spend jumped 24.8%

Ad impressions, however, were a different story, as the share of impressions on Android rose from 43.32% in Q2 to 56.68% in Q3.

- iOS: ad impressions dropped 3.4%

- Android: ad impressions jumped 30.9%

That means more spend is chasing fewer impressions, and — as you’ll see in the CPI data — driving prices higher.

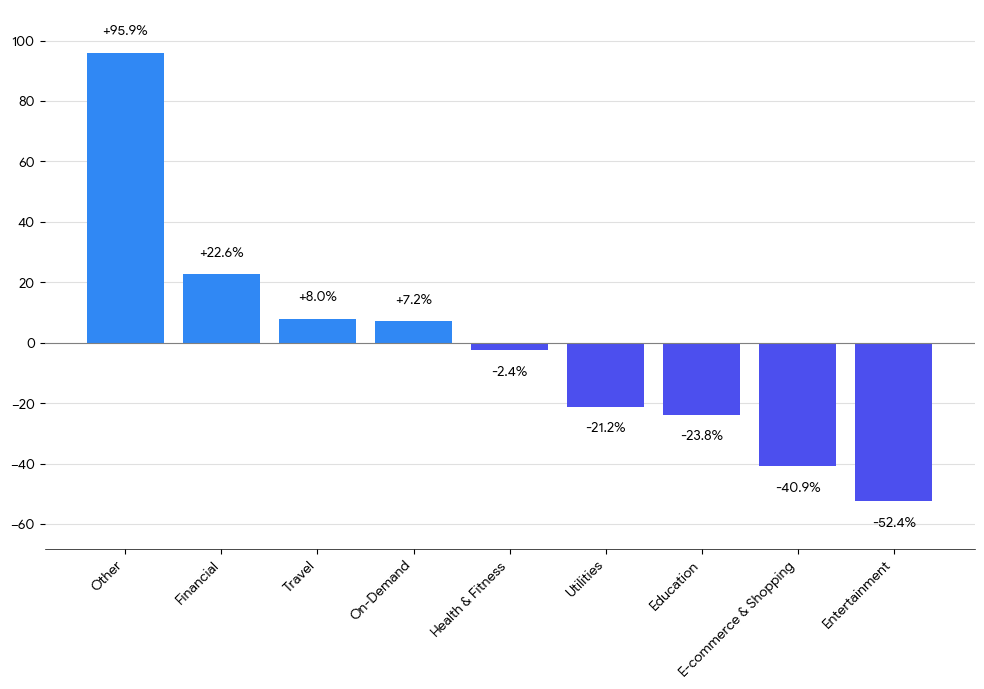

Ad spend by vertical

Ad spend was not up across the board, however.

Global ad spend change by vertical

")

Travel, financial and gaming were significantly up, with travel growing the most of all at 58.9%. That makes sense: while Q3 is at or near the end of the summer travel season, it’s also the time to plan year-end holiday travel.

Shopping was down slightly, while Entertainment and Education were down 17.4% and 20.8% respectively.

You’d expect Shopping and Retail to be up ahead of the big holiday Q4, but growth markets could have front-loaded their acquisition campaigns in the previous quarter.

Ad spend by region

Every single global region was up in ad spend from Q2 to Q3:

Global ad spend change by geo

Ad spend measured by Singular exploded in China (the caveat is that this is on a smaller base than many of the other regions, as Singular is fairly new in China).

Eastern regions in general were up, however, as Tier 1 East, which includes Korea, and Tier 2 East, which includes Taiwan, Indonesia, Turkey, Thailand, and the Philippines, were both up over 30%.

The U.S. was up 21.2%, and while that might seem small looking at the other numbers, it’s actually hugely significant as it is growth on top of a truly massive base.

ATT and IDFA availability

ATT opt-in rates actually jumped 10.2% in Q3 2025.

Global Opt-In (July 2025, August 2025, September 2025)

That’s positive news for mobile marketers who care about measurement, of course, but realistically it’s almost immaterial, as initial opt-in rates are still only 9.1%, marginally up from 8.26% in Q2.

Eventual ATT acceptance rates will be slightly higher than this, of course. This number is measured at first open after install, and not all apps ask for ATT permission instantly.

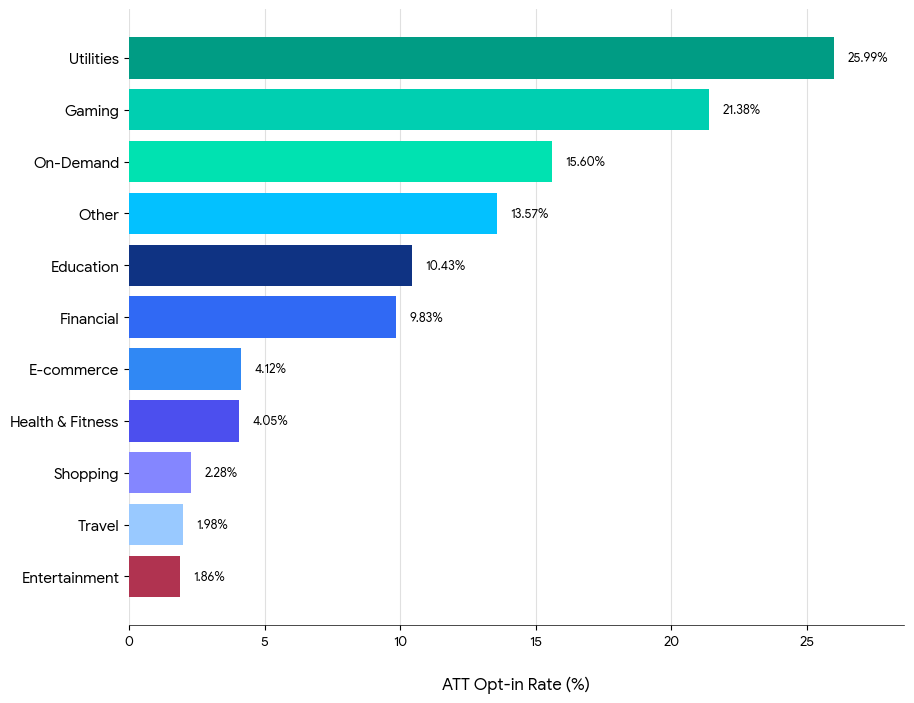

ATT acceptance by vertical

Once again, Utilities and Gaming led all verticals in ATT acceptance.

In these verticals, users see tangible value connected to allowing measurement, whether that’s personalization or core features that are tied to tracking.

ATT opt-in rates by vertical

On-demand verticals in delivery also get high opt-in rates, while Shopping, Travel, and Entertainment see the lowest rates of acceptance.

That’s surprising when the Shopping and Travel category could see tremendous benefits from IDFA visibility … perhaps marketers in these areas need to study Utilities and Games to look for new tactics to generate higher levels of opt-ins.

Global metrics: big picture

Everything was up last quarter: cost, clicks, ad revenue, and installs per thousand ad impressions.

This quarter, almost everything is up, with installs per thousand impressions the lone outlier.

The biggest change: cost per install.

* Note: I’ve taken iOS Gaming out as it was skewing the CTR metrics last Quarterly Trends Report. CTR in iOS Gaming has been super-high thanks to compound rewarded ad units that trigger multiple SKOverlays.

CPI deep dive: geos, verticals, genres

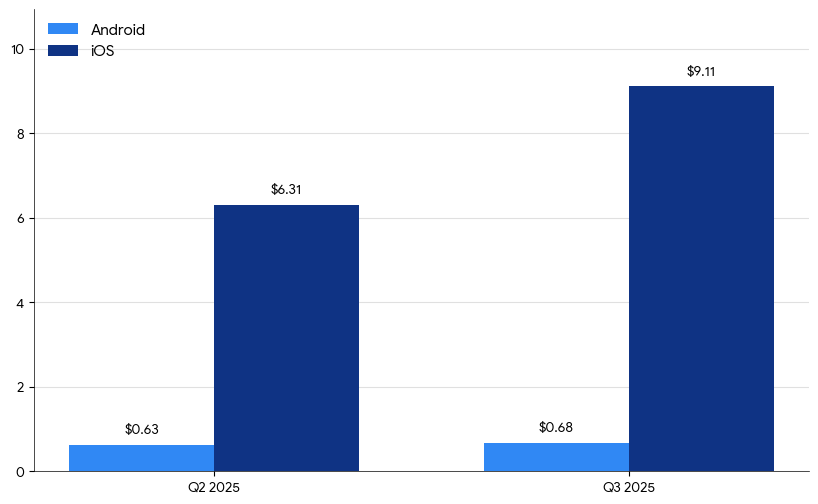

Global CPI by platform

Overall CPI was relatively stable for Android but up significantly on iOS:

- Android: $0.68, up 7.9%

- iOS: $9.11, up 44.4%

Why?

Partly because advertisers have confidence on iOS after years of recapturing data post-ATT. And partly because Q3 is ramping up to Q4, and advertisers are kicking off Q4 pipeline building ahead of holiday seasonality.

A bigger reason however, was that more dollars were chasing fewer ad impressions, as we saw earlier. The natural result: higher prices.

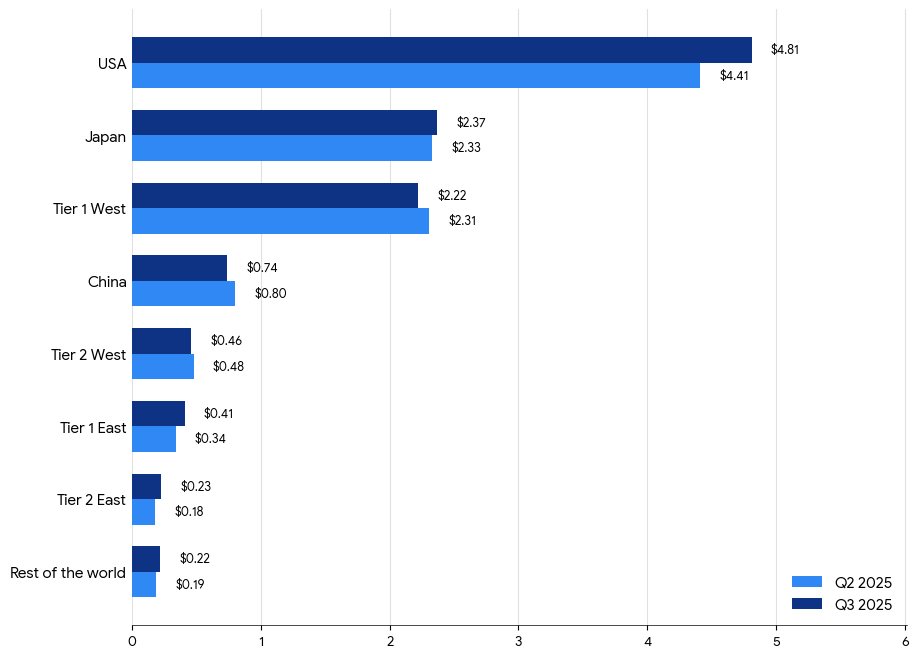

CPI by region

Here’s Android data for CPI by region (thanks to the GAID, location data is more accurate on Android than iOS).

Android CPI mostly rose slightly or stayed flat, except Tier 2 West (down 3%) and China (down 8%). As expected, CPIs in the U.S. are highest, while emerging regions (Tier 2 East, Tier 1 East, RoW) saw notable CPI increases, suggesting stronger advertiser interest outside core Western markets.

CPI by vertical

On Android, we saw modest increases in CPI for Travel, On-Demand, Financial, and Entertainment, with a drop in Utilities and a flat Gaming.

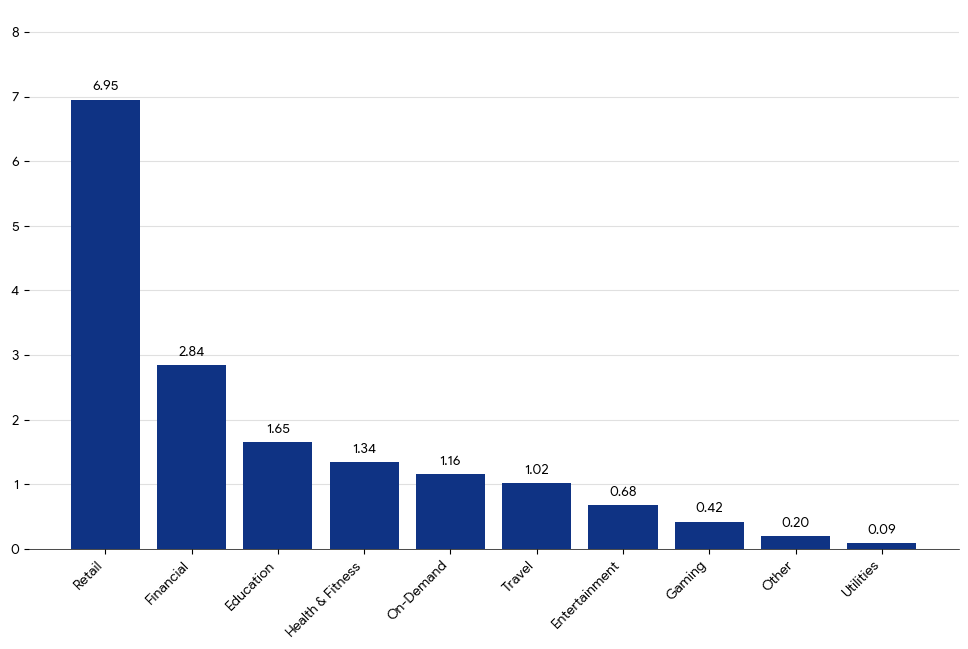

Heading into the holiday quarter, Retail is the most expensive category:

CPI by vertical

On iOS we saw some big jumps in key verticals that rely heavily on high-LTV users:

- Gaming (+128%)

- E-commerce (+61%)

- Travel (+55%)

Retail app installs are the most expensive right now, with Financial and other categories trailing.

CPI by vertical iOS

Android CPI prices were more stable, partly because many Android-heavy countries don’t have the same traditional holiday and buying season as Europe and North America.

On both iOS and Android, Utilities CPIs are very low.

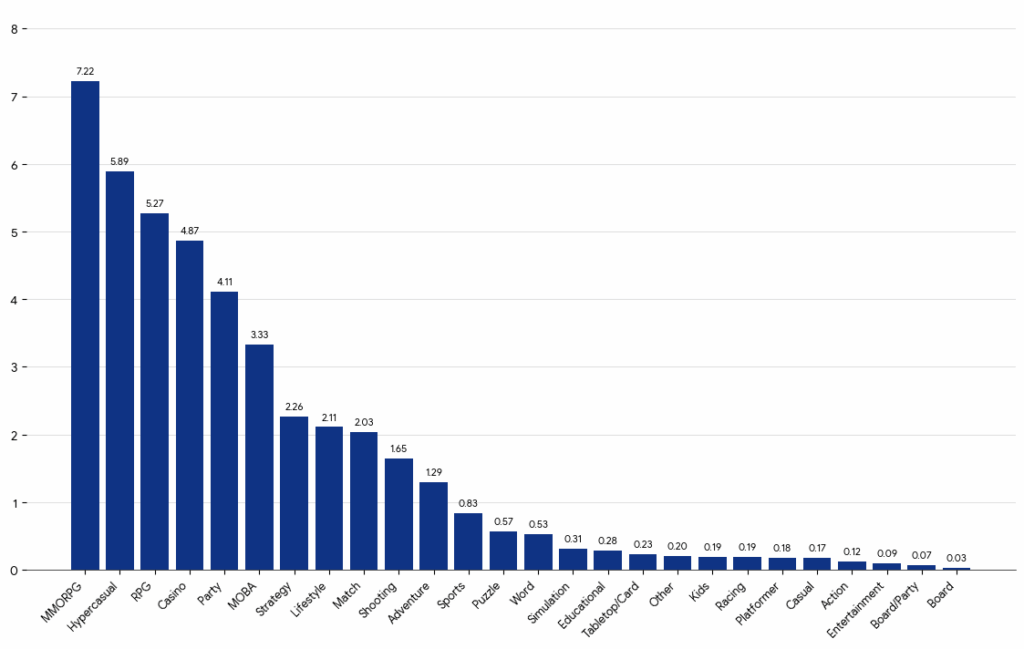

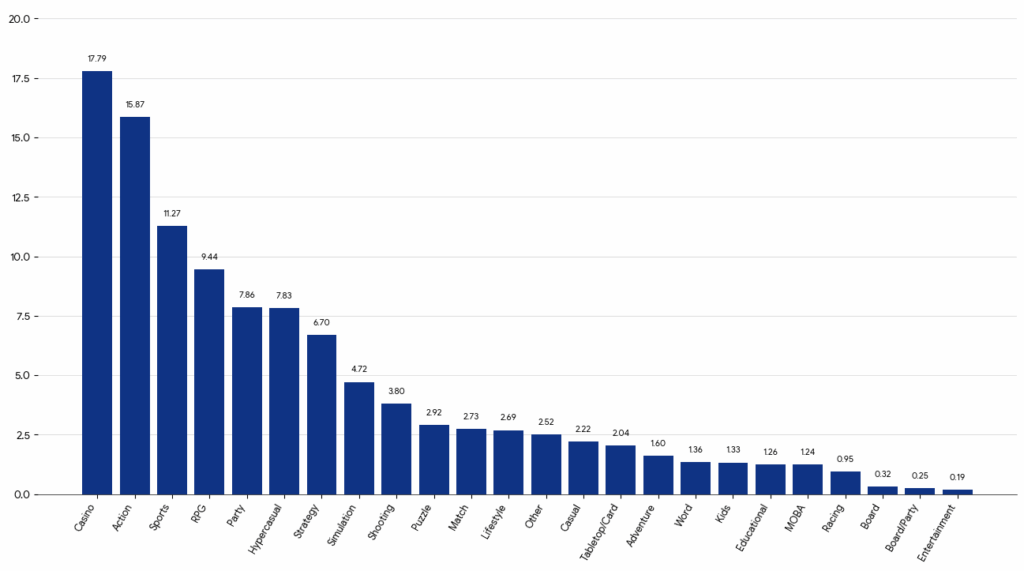

CPI by game genre

Genres where players need to spend money (Casino, RPG, Strategy) or where deep engagement is required (Action, Sports) have the highest CPIs. Low-engagement, ad-monetized genres like Hypercasual, Puzzle, and Casual are much cheaper, especially on Android.

Android games have lower CPIs, roughly 3X-4X below iOS:

CPI by game genre Android

The top CPIs on iOS are in Casino, Action, Sports, and RPG … all genres where high LTVs can justify big bids. These are genres with strong IAP economies and whales, where UA teams can profitably spend heavily.

CPI by game genre iOS

Even “cheap” iOS categories often cost more than Android’s mid-tier genres, reflecting iOS’s high-value player base.

There are, however, genres like Tabletop/Card, Educational, and Board/Party that hover near $1 or less. The caveat is that these genres are consistent with limited monetization and smaller, more niche audiences.

Key metrics by country tier and vertical

At Singular, we look at data by regions:

Here’s the data:

Key regional insights

Let’s look at the highlights in each market segment …

United States

- Expensive traffic

- High monetization potential

- High variance by vertical

- Smart optimization pays off

China

- Huge scale but fragmented ecosystem

- Ultra-efficient installs with very low CPIs

- High CTRs and strong conversion rates

- Low CPMs

- Excellent for Gaming, Entertainment, and Utilities

Japan

- High-intent, high-value, high-cost market

- Behaves more like the U.S. than the rest of APAC

- Lower CTR but strong CVR and retention

- Ideal for Gaming, Finance, and Subscription apps

- Creative localization is essential for success

Tier 1 West

- Much cheaper than the U.S.

- Huge IPM jump in verticals like Utilities

- Slightly lower CTR overall

- Strong CVR and IPM make installs efficient

- Excellent balance of cost and quality; strong region for scaling

Tier 1 East

- Combines premium audience quality with better cost efficiency

- Sweet spot for global brands seeking scale without U.S.-level CPIs

- Gaming and Travel perform exceptionally well

- High engagement and solid retention

- Ideal for performance campaigns across high-value APAC markets

Tier 2 West

- Cost-efficient scale region

- Cheap installs, high CTR, and decent CVR

- Monetization per user may lag

- Great for soft launches, experimentation, and volume scaling

- Strong performance in Utilities and Gaming verticals

Tier 2 East

- Massive install volume at bargain CPIs

- Excellent for top-funnel growth and rapid testing

- Requires localized creative and cultural relevance

- High CTRs but inconsistent CVR

- Best for Utilities and Casual Gaming

Rest of World

- Cheap reach but questionable user quality

- Excellent for awareness or early-stage app seeding

- Low ROAS without strong optimization

- Needs heavy filtering and retargeting to achieve profitability

- Best for low-cost content or utility apps

Or, if you prefer a simple chart

Key vertical insights

Here are some of the insights we can draw from a vertical perspective …

Education

- Moderate CPI and strong CVR: users often install with clear intent

- Most profitable in Tier 1 East (premium audiences, efficient performance)

- Most expensive in the United States (high CPM)

- Intent-driven installs and strong user quality

- Performs best in high-engagement, low-CPI markets

Entertainment

- Moderate CPI with good CTR and CVR

- Strong IPM in Tier 1 West and Tier 2 West (cost-efficient installs)

- Most profitable in Tier 1 West and Tier 2 West

- Most expensive in the United States (premium streaming/OTT competition)

- Balanced vertical: scalable, high engagement, and global appeal

Financial

- Highest CPI overall: easily $10+ in the United States and 2–3X other verticals

- Low IPM and CTR due to friction and compliance hurdles

- Most profitable in the United States (LTV justifies spend)

- Expensive everywhere … rarely cheap in any market

- Competitive but profitable where lifetime value is extremely high

Gaming

- Mid-range CPI that varies massively by genre

- Strong IPM in Tier 2 East and Tier 1 West

- CPI spikes on iOS in high-value regions like Japan and the United States

- Most profitable in Tier 2 East (huge scale, cheap installs)

- Most expensive in Japan and the United States

- High-volume category: cheap in emerging regions, premium in Japan/U.S., strong global ROI potential

Health & Fitness

- Moderate CPI, typically between $2–$5 in higher-tier markets

- Strong CVR: intent-driven installs; users act quickly post-click

- Mid-range IPM

- Most profitable in Tier 1 East (balanced cost and engaged users)

- Most expensive in the United States and Japan

- Quality users but higher costs: great vertical for ROI-focused optimization

On-Demand

- High CPI everywhere, especially in the United States and Japan

- Low IPM and CTR, limited conversion efficiency: tough vertical

- Most profitable in Tier 1 West (better cost/performance ratio)

- Competitive category: unit economics depend on LTV, not CPI

Retail

- CPI rising fastest across all verticals (up ~40% on Android, +61% on iOS quarter over quarter)

- Highest iOS CPIs globally, especially in the United States and Japan

- Strong CTR, but expensive CPM drives up acquisition cost

- Most profitable in Tier 1 East and Tier 2 West (cost-efficient buyers)

- Most expensive in the United States (holiday ad competition)

- Enormous demand and competition: requires precise bidding and real-time optimization

Travel

- CPI varies widely: very high in the United States, more efficient in Tier 1 East and Tier 1 West

- CTR and CVR are solid: visually engaging creatives work well globally

- IPM decent, though not as high as Utilities

- Most profitable in Tier 1 West and Tier 1 East (premium users, moderate CPIs)

- Most expensive in the United States (competition for affluent travelers)

- Performs best in premium but efficient regions

- Heavily influenced by seasonality

Utilities

- Cheapest CPI across almost every region, especially Tier 2 East and Tier 1 West

- Highest IPM globally (24+ in some Tier 1 West data)

- Strong CTR and CVR: utilities have universal appeal and low friction to install

- Most profitable in Tier 1 West and Tier 2 East (mass scale and low CPI)

- Most expensive in the United States and Japan, but still efficient

- Performance powerhouse: high efficiency, low cost, easy to scale

Hottest genres: apps and games

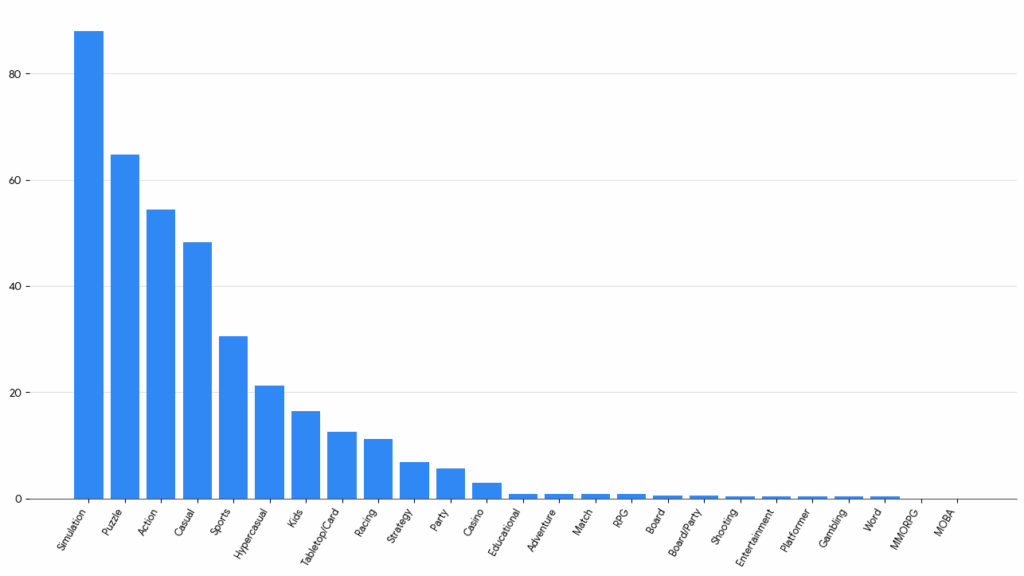

Games: most installs, fastest growing

Sim games are booming, with both the highest number of installs and the largest growth over the past quarter.

Highlights:

- Simulation, Puzzle, and Action

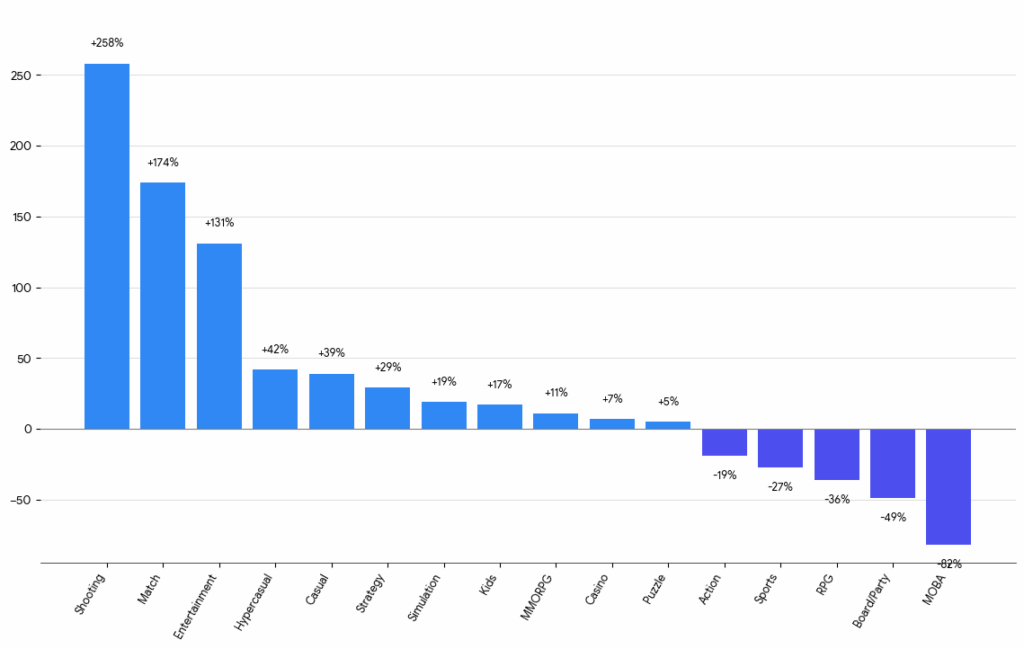

These genres dominate in total installs, capturing over half of all gaming downloads - Shooting and Match

Breakout performers with triple-digit growth, signaling renewed advertiser focus - Casual and Hypercasual

These remain consistent growth drivers, aided by broad appeal and ad-monetized models - Strategy and Simulation

Sustainable expansion: high retention, moderate CPI, good ROI - RPG, MOBA, and Board/Party

These genres contracted sharply, perhaps reflecting saturation

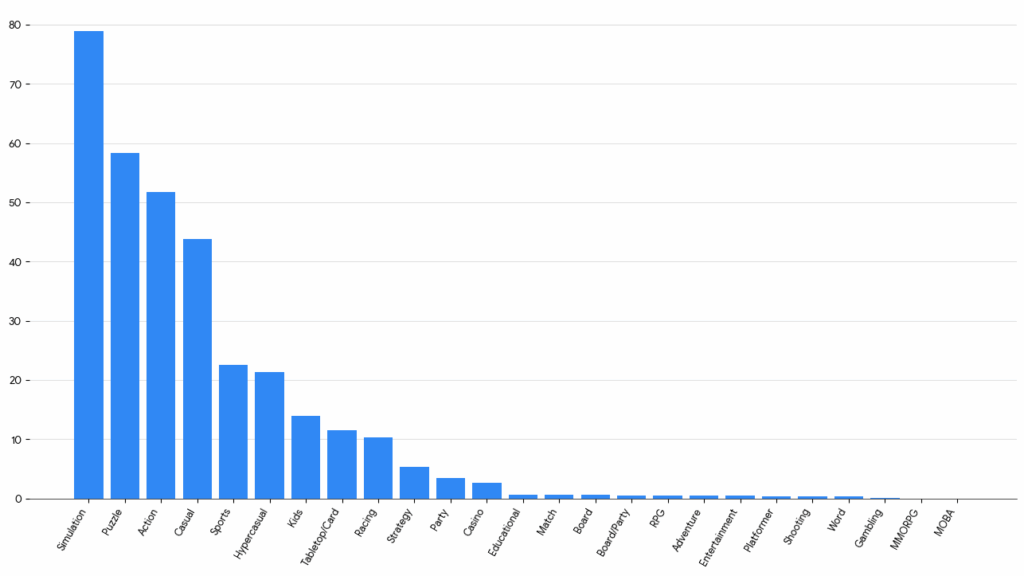

Most downloads, all platforms

Game installs by genre

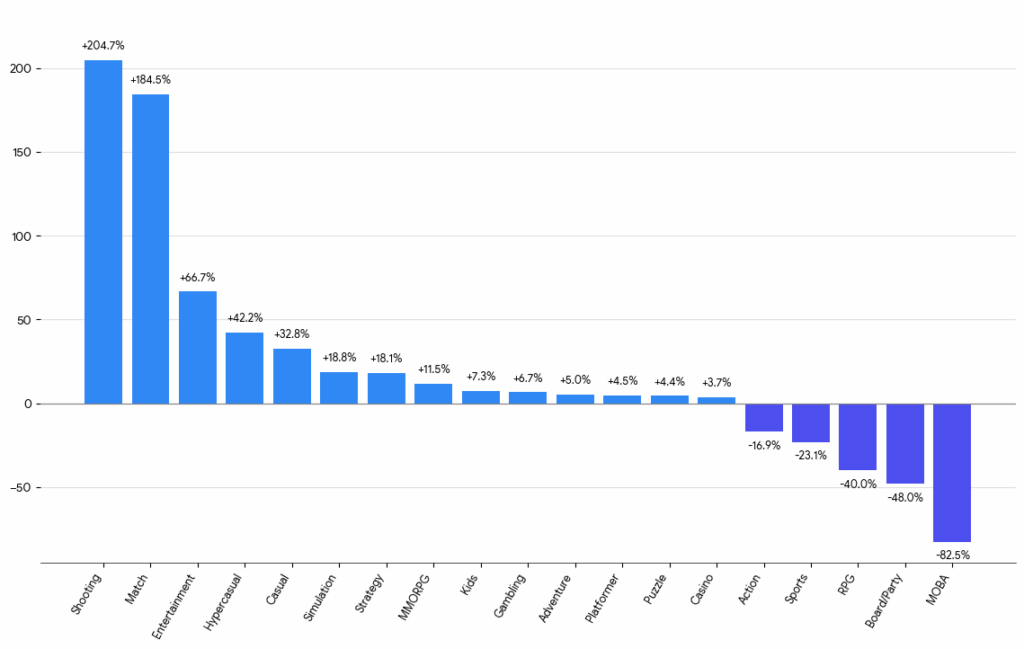

Most growth in percentage, all platforms

Game growth by genre

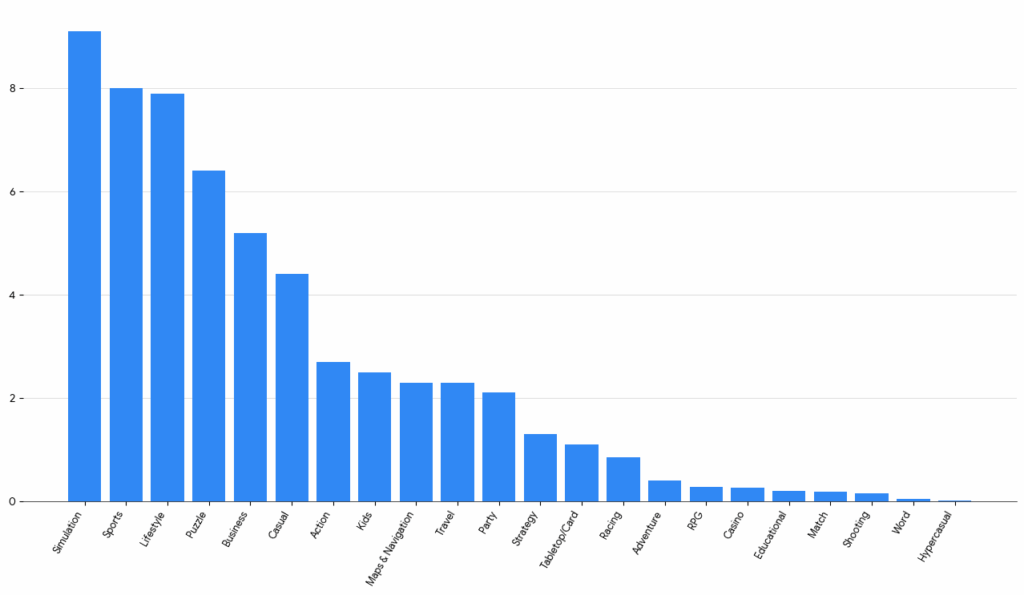

Android games: most downloaded, most growth

Game installs: Android

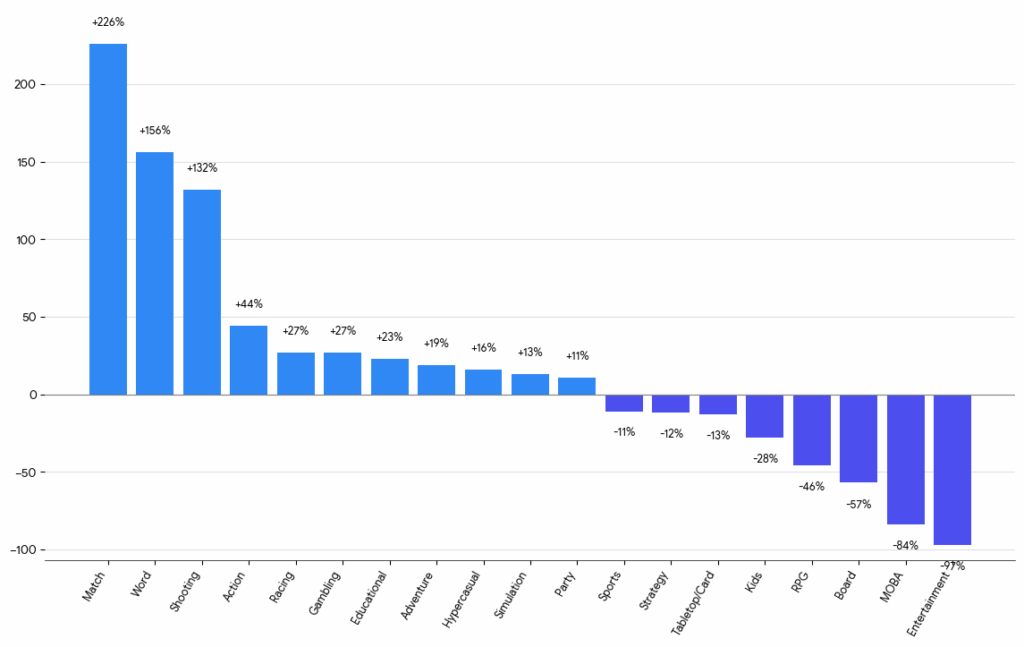

Game growth: Android

Key insights:

- Shooting and Match exploded

Both genres posted triple-digit growth, with Shooting up +258% and Match up +174%

- Ad-driven genres thrived

Hypercasual and Casual titles continued to scale rapidly (+42% and +39%), showing that Android remains the top platform for broad reach and cost-efficient UA

- Simulation stable and massive

Simulation led all genres in total installs (78.9M) and still grew +19%, proving its staying power and appeal across both performance and organic channels

- Core and sports titles softened

Action and Sports declined (–19% and –27%), indicating maturity and possibly shifting ad spend toward higher-yield genres like Casual and Match

- Android shows greater volatility

Compared to iOS, Android genres demonstrate bigger swings in growth rates and larger total volumes, reflecting its global scale, lower CPIs, and broader user base

iOS games: most downloaded, most growth

Game installs: iOS

Game growth: iOS

Key insights:

- Casual genres surged

Match and Word games were breakout stars on iOS, each doubling or tripling installs, suggesting strong ad pushes and viral titles - Action and Shooting rebounded

Mid-core categories showing renewed UA focus, likely driven by new releases and stronger monetization confidence - Simulation steady but mature

Still the largest category on iOS with solid +13% growth … Simulation continues its broad appeal in both paid and ad-supported models - Traditional hardcore genres declined

RPG, MOBA, and Board games saw major drops, possibly due to market saturation or limited new launches

- The iOS market remains top-heavy

A handful of casual and hybrid-casual genres capture nearly all growth momentum, while deep-core titles stagnate

Apps: most installs, fastest growing

On-demand apps are the clear stars of the non-gaming mobile universe right now.

Highlights:

- On-demand

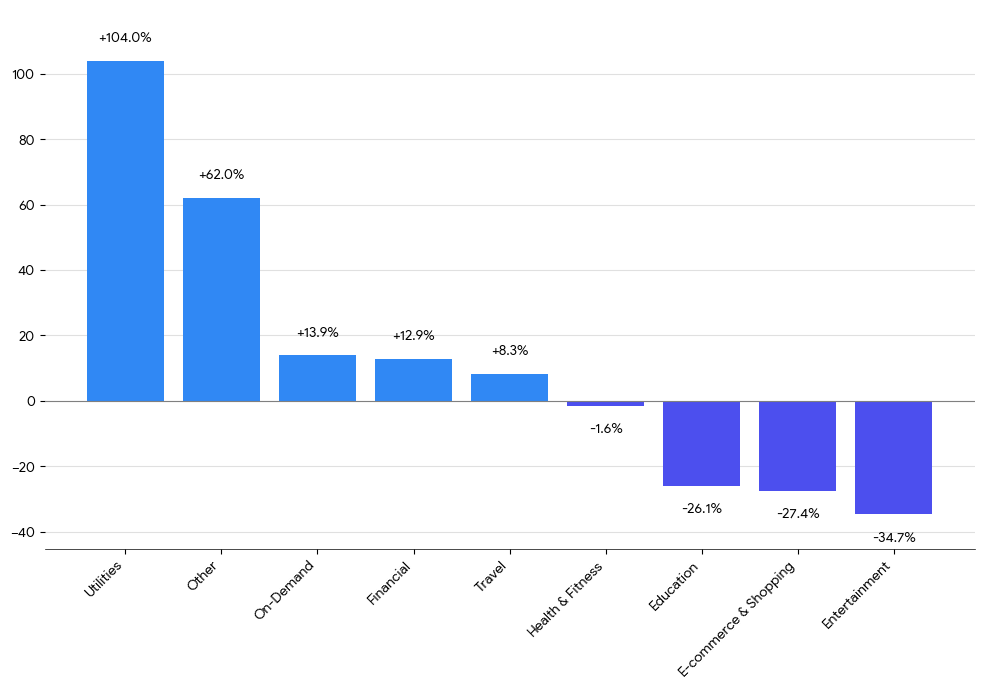

Top non-gaming vertical with 14% growth … there’s strong ongoing demand for delivery and gig apps - Utilities

Surged 104%, the fastest-growing category - Financial, Travel, and Health

Moderate 8–13% growth, indicating maturity and consistent engagement - Entertainment, Retail, and Education

These categories declined, reflecting reduced ad spend or content fatigue

App installs

App growth

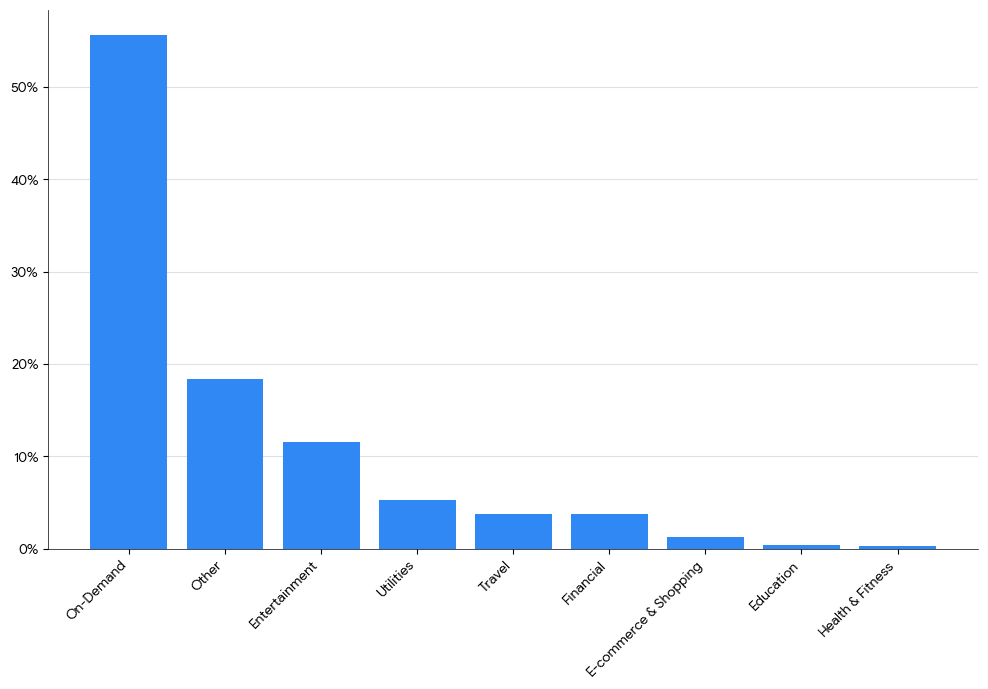

Android apps: most downloaded, most growth

App installs: Android

App growth: Android

Key insights:

- On-demand

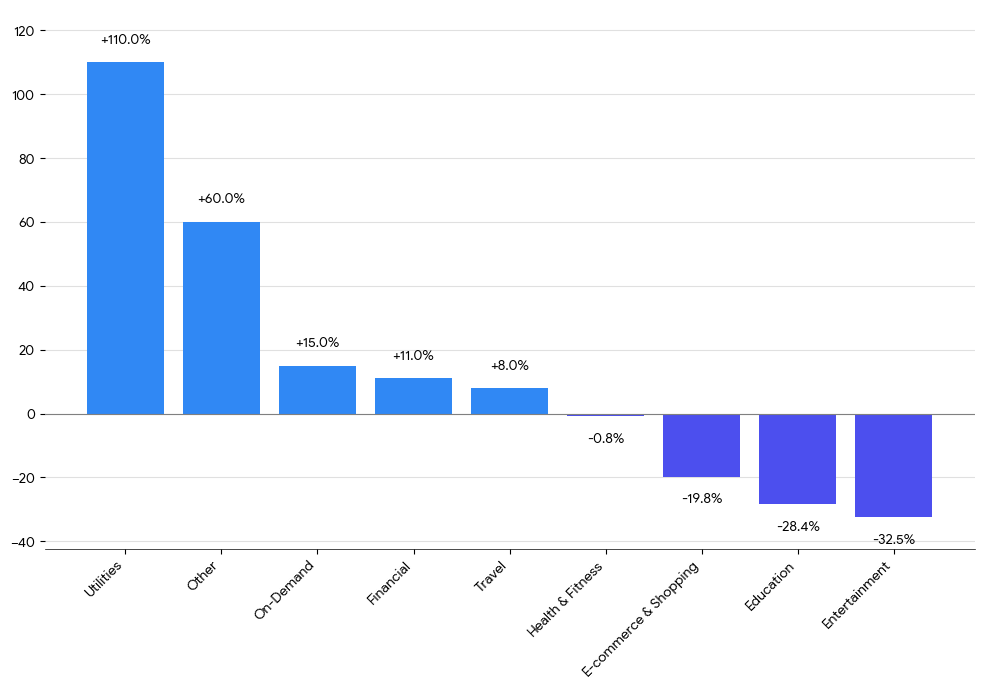

Largest Android vertical with steady 15% growth, driven by delivery and gig apps - Utilities

Doubled installs (+110%) as viral tools and AI helpers surged in popularity - Financial and Travel

Moderate 8–11% gains, reflecting steady seasonal demand - Entertainment, Education, and Retail

Declined, signaling budget shifts and weaker engagement

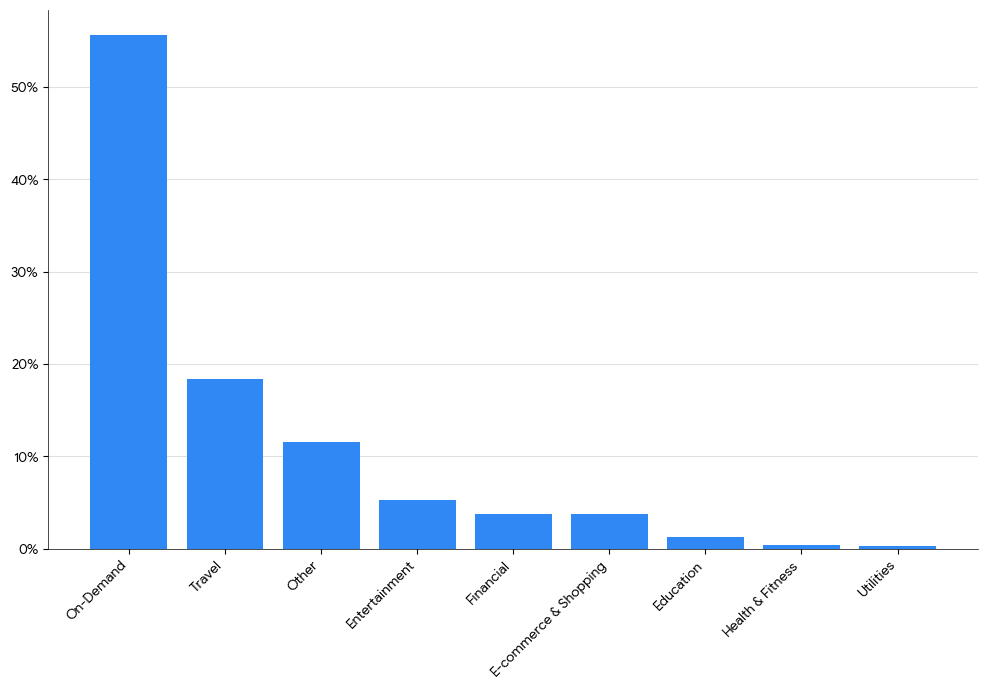

iOS apps: most downloaded, most growth

App installs: iOS

App growth: iOS

Key insights:

- On-demand

As on Android, On-demand leads all categories in installs with steady 7% growth - Financial

App installs rose 23%, signaling strong interest in fintech and budgeting tools - Travel continued moderate recovery with 8% growth post-summer

- Entertainment and Retail

Installs dropped significantly, showing major UA pullbacks - Utilities and Education

Installs dropped here too, suggesting reduced ad focus and seasonal slowdowns

Monetization trends

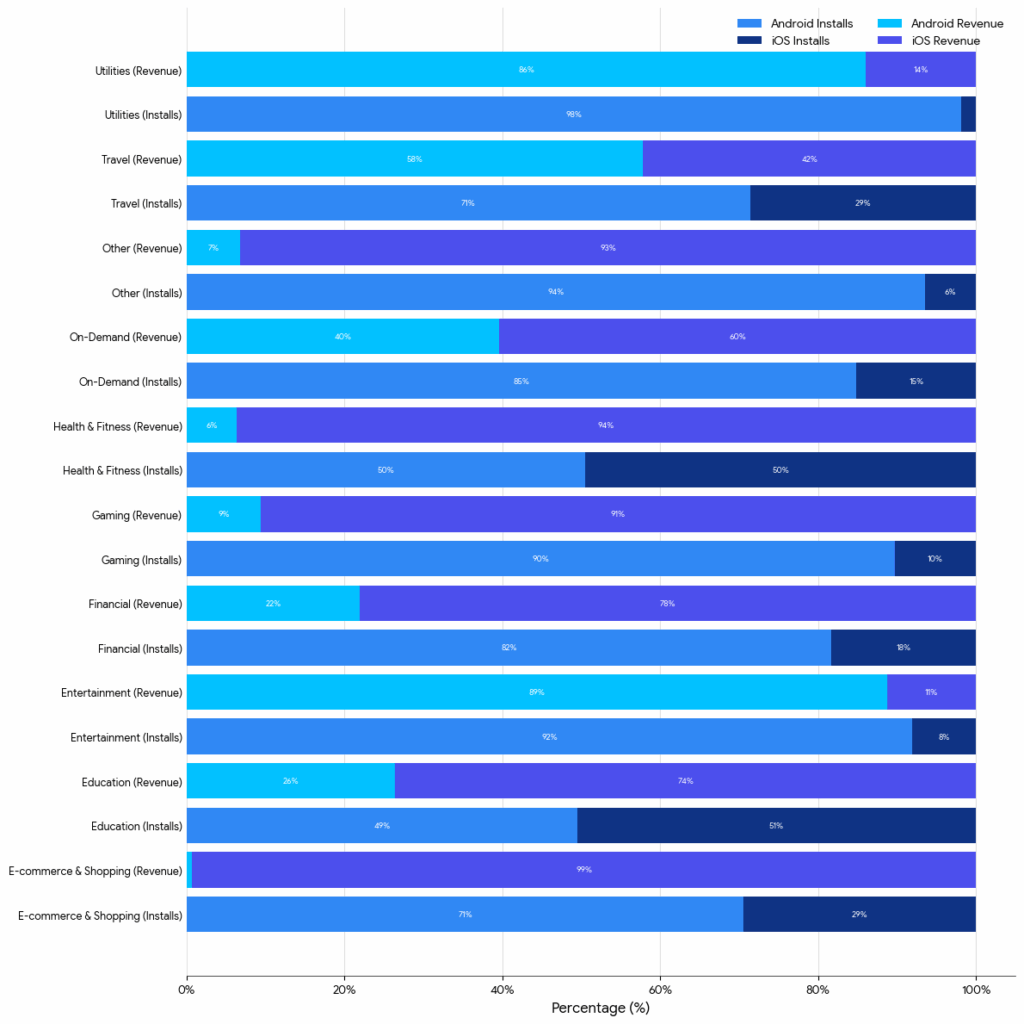

Android = volume and iOS = value?

Mostly true, but not totally.

Sure, Android dominates installs across nearly all categories, getting usually 70–95% of total installs. And yes, iOS dominates revenue: in most verticals, iOS generates 70–95% of total revenue, even when its install share is small. So you do see the classic split.

But not everywhere. Not Utilities, for example.

And not Entertainment.

Installs vs Revenue

Key insights by vertical:

- Financial

Android drives 82% of installs but only 22% of revenue, showing iOS users are far more valuable - On-Demand

Again, Android has 85% of installs, but iOS contributes 60% of revenue, a strong monetization skew - Travel

Travel is much more balanced: 71% of installs on Android and 58% of revenue, so both platforms perform relatively evenly - Utilities

Utilities are where Android wins everything: 98% installs and 86% of revenue, mostly because Apple locks iOS down much tighter - Health & Fitness

Installs are split 50/50, but iOS drives 94% of revenue … one of the most extreme differences - Entertainment

Android leads both installs and revenue, but the revenue gap is smaller than other categories - Education

Here we see roughly balanced installs (50/50) but iOS captures 74% of revenue, showing higher paid adoption - Retail

Android gets 71% installs but iOS captures a whopping 99% of the revenue, the biggest disparity in the dataset

Ad network share of spend: biggest winners

I’m not sure if I thought it was possible, but TikTok’s growth is kind of exploding. TikTok captured the most new revenue of any ad network, and it really wasn’t very close, as well as the most new advertisers.

Search and high intent platforms are still big, however, as both Google and Apple Ads saw significant gains.

Of course, Meta never loses: it’s also growing in both advertisers and dollars.

There is also growth at the edges, however.

Networks like Jampp, RevX, and Remerge are showing large revenue growth, indicating that DSPs and re-engagement platforms are doing well. (Check our recent re-engagement and retargeting report, by the way.) Companies like Mintegral, Moloco, Mobon, and Bigo are seeing gains in both spend and advertisers, pointing at more global campaign expansion spending. And the growth by Unity Ads, AppLovin, Appier, and Reddit highlights how marketers are not relying solely on Meta, Google, Apple, and TikTok.

All platforms combined

Ad spend gained

Advertisers gained

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Gainers by platform

As you’d expect, TikTok is high on both the iOS and Android sides: TikTok has become a cross-platform essential for UA teams.

Google’s doing well, especially on the Android side, and Apple Ads continues to grow.

Cross-platform DSPs like Unity, AppLovin, Moloco, and Mintegral are seeing growth across both OSes, while Jampp and Remerge saw major iOS gains.

Last quarter was all about rewarded ad networks, names like Exmox, Adjoe, Kashkick, Adlmedia, Benjamin, MAF, and TyrAds. They’re still seeing growth, but as we approach the holiday season, some of the more traditional platforms and players are seeing more growth.

Android

Ad spend gained

Advertisers gained

1

2

3

4

5

6

7

8

9

10

iOS

Ad spend gained

Advertisers gained

1

2

3

4

5

6

7

8

9

10

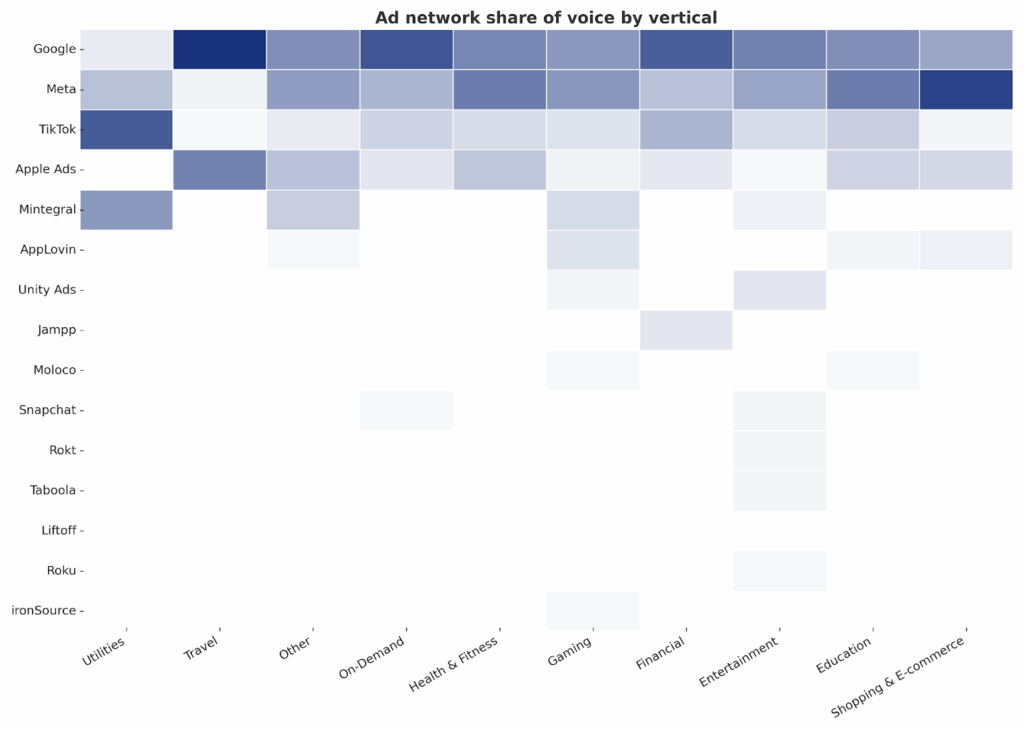

Ad network share of voice by vertical

It’s interesting to look at ad network share of spend by vertical.

In this heatmap, color intensity reflects how important or dominant that ad network is within that vertical. Darker colors indicate strong presence; lighter colors show less share.

Here’s another way to look at the data: top 5 ad networks by vertical in a table format.

Important note: Google and Meta are tops in almost everything, so I’m excluding them from this list. As you see each list of ad networks, just mentally add Meta and Google to each.

Top networks by installs (beside Google & Meta)

Top networks by spend (beside Google & Meta)

Key findings:

- Meta and Google are dominant in almost every area, so add the above caveat to the below insights …

- TikTok is impressive almost everywhere

- And it’s absolutely huge for the Utilities vertical

- Top 2 in Financial, On-Demand, Education, and shows up for E-commerce too

- Apple Ads is also huge, but only on iOS of course

- #1 or #2 in Education, Travel, Shopping & E-commerce, Health & Fitness, and Financial

- Many DSPs are successful in a few key verticals, especially Gaming

- Mintegral, though it also performs well in Utilities and Other

- Unity Ads and AppLovin own gaming when you take the giant platforms out

- AppLovin also shows up across Entertainment, On-Demand, and Education

- Liftoff shows up in Health & Fitness, Financial, and Shopping & E-commerce

- Moloco is present across Gaming, Utilities, Education, Health & Fitness

- Remerge makes appearances in Shopping & E-commerce and Financial, reinforcing its position as a retargeting specialist

- Other ad networks or platforms also have fairly specific specialties:

- Roku shows up for Entertainment, as you’d expect

- Taboola pops up in Entertainment too, though you should expect to see it in News verticals as well

- Kakao is present in Shopping & E-commerce spend, highlighting its relevance in Korea/APAC-driven user acquisition

- Adjoe surfaces in Health & Fitness and Entertainment

- X still gets spend in Financial and On-Demand

Partner insights

Beyond Google and Meta: Where real ROAS growth is happening

1. There is Striking ROAS Lift from Diversifying Beyond Google/Meta

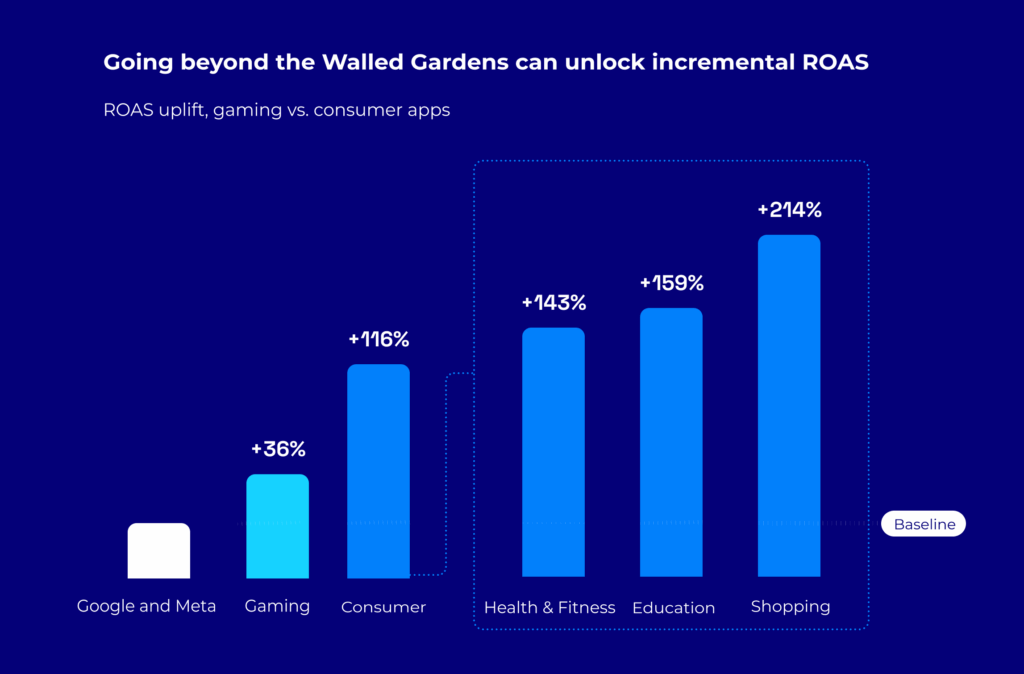

As people spend more time across more apps, there’s tremendous upside for marketers who expand their mix and reach people where they are. Almost 50% of the time people spend in mobile apps happens outside of Google and Meta, and consumer app marketers who diversified their ad spend beyond Google and Meta saw an average 116% increase in Day 30 ROAS, with some categories (shopping, education, health & fitness) seeing lifts even higher. Gaming apps are an interesting comparison here. Gaming marketers have consistently seen a lot of success diversifying their mix, and their lifts are lower (48%)!

What to consider: Consumer app marketers are leaving significant growth opportunities on the table when they stick exclusively to walled gardens.

2. Finding High-Value Users in Unexpected App Categories

High-value users don’t always convert from “relevant” apps—they convert from surprising places too. Mobile users visit dozens of independent ad-supported apps monthly. For example, food delivery app users visit an average of 40 independent apps, while travel booking users visit 35.

What to consider: Not only are users multidimensional and should be targeted as such, Moloco data shows cheaper CPP (cost per payer) outcomes when reaching users in adjacent, unexpected app categories.

3. 53% of Users Want to Spend LESS Time on Social Media

Users are actively trying to reduce social media usage due to emotional fatigue—Over 60% of 18-34 year-olds want to cut back. 42% of young adults feel negative emotions (envy, anxiety, distrust, overwhelm) when using platforms like Facebook or TikTok.

Time spent on mobile devices overall is hitting a natural saturation point, so the pressures on driving ad performance and scale are more intense than ever. It’s no surprise that 66% of young adults also feel ad fatigue from seeing the same ads repeatedly.

What to consider: As consumer sentiment shifts and competition increases, it’s critical to work with trustworthy partners who have the reach and proven performance to help you find and make the most of every growth opportunity.

For more insights, explore the interactive Performance Through Independence report, created in partnership with Moloco, Sensor Tower, and Singular. This data-driven report uncovers a new opportunity for app growth—users are spending more time in independent apps than ever before, converting from unexpected places, and rewarding marketers who follow them with significant incremental growth.

Multiscreen shoppers redefine the festive path to purchase

The global holiday season is no longer a single-channel experience. Consumers now navigate complex, multiscreen journeys before making purchase decisions. With Diwali and Dussehra recently wrapped up in India, the festive season has set the stage for a surge in consumer spending. Globally, regions are now gearing up for year-end holidays such as Black Friday, Christmas, and New Year, making this a critical period for digital advertisers.

At Affle, we recently conducted a first-party consumer study to dive into how shoppers engage in complex, multiscreen journeys, navigating discovery, research, and purchase across mobile devices, connected TVs, laptops, and even offline stores. Understanding these behaviors is key to designing campaigns that maximize festive and holiday season impact. While the survey results are limited to audiences in India, the learnings have an impact for global advertisers, where understanding these behaviors is key to creating campaigns that drive impact during peak festive periods.

Mobile Remains the Heart of Discovery and Transactions, But Living Room Influence via CTV Rises

Smartphones continue to dominate the festive shopping landscape, being the primary channel for both product discovery and final purchase. Living-room screens are increasingly influencing festive inspiration and purchase research. Our study found that 32% of consumers use Smart TVs, with 27% engaging in internet-based viewing on Connected TVs (CTV). This rise signifies an opportunity for advertisers to leverage CTV campaigns for inspiration-led storytelling, reaching audiences in a relaxed, intent-driven context. In fact, 31% of consumers discover new shopping apps through CTV ads, highlighting the channel’s role in extending the reach of digital campaigns beyond smartphones.

Cross-Device and Omnichannel Journeys

Festive shopping is rarely confined to a single device. Affle’s first-party study also showed that while 58% of consumers complete purchases on the same device where discovery occurs, 32% switch to another device, such as a laptop or tablet, before conversion. Moreover, 38% of shoppers eventually finalize their purchase offline, demonstrating the omnichannel impact of digital advertising. QR scanning from connected TVs and in-store mobile interactions further highlight the integrated, multi-device behaviors shaping festive commerce.

Over half (56%) of consumers consistently compare products across apps before making a decision, underscoring the competitive landscape and the importance of maintaining visibility across multiple digital touchpoints.

Implications for Advertisers

These insights highlight the importance of brands adopting multiscreen strategies during festive seasons. Mobile-first campaigns remain critical for discovery and transactions, but connected TV, cross-device retargeting, and omnichannel attribution are increasingly essential to capture influence throughout the consumer journey. In a market where discovery, comparison, and purchase are distributed across screens and offline channels, integrated campaigns that map to actual consumer behavior will drive the strongest festive-season impact.

For advertisers, the key takeaway is clear: campaigns that seamlessly engage consumers across screens and channels, while adapting to their non-linear, comparison-driven shopping behavior, will deliver the most significant impact. As holiday seasons unfold worldwide, embracing multiscreen strategies is no longer optional, it’s central to capturing attention, driving conversions, and shaping the future of digital commerce.

AI, video, and the new dynamics of mobile advertising

Link to Tinuiti’s Q3 2025 Digital Ads Benchmark Report

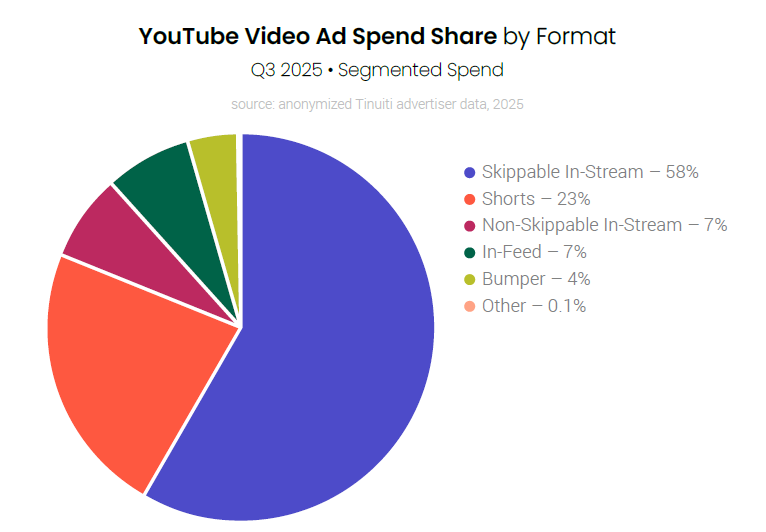

- YouTube Shorts Ads are the second-largest format for YouTube video ad spend, with mobile phones accounting for just a under a third of spending.

- Shorts Ad Spend Share and Device Split: In Q3 2025, Shorts ads made up 23% of segmented YouTube video ad spending, second only to skippable in-stream ads. But despite the vertical format having its roots in mobile devices, TV screens generated nearly half of Shorts ad spending for the average brand in Q3.

- Mobile-First Content Evolving Beyond Mobile: This is a pretty big shift for anyone thinking about mobile marketing. Shorts isn’t really “mobile content” anymore — it’s vertical, short-form content that people consume everywhere. Your mobile-optimized creative is now reaching living rooms, which means you need to think about how it plays across all these different screens. This suggests that YouTube Shorts offer a unique bridge to maintain mobile-native creative while gaining significant new TV-based reach.

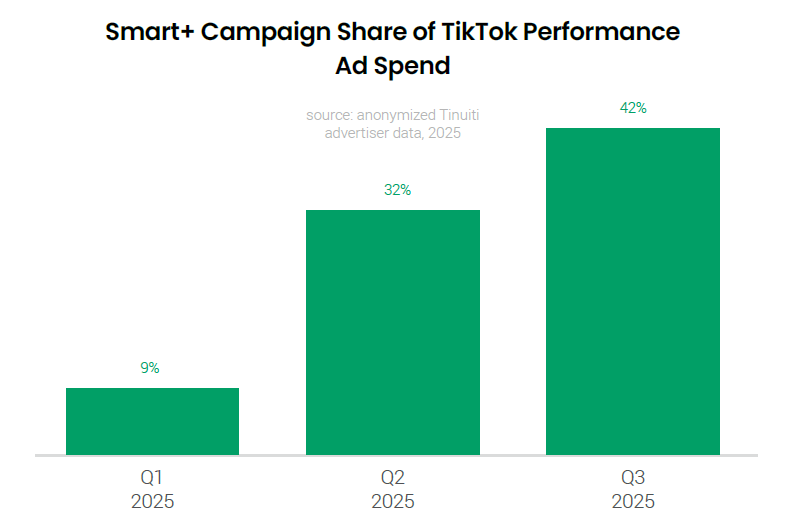

- TikTok Smart+ campaign adoption has surged among performance advertisers.

- Smart+ Campaign Adoption Rate: The share of TikTok performance ad spend attributed to TikTok Smart+ campaigns grew from just 9% in Q1 2025 to 42% by Q3 2025. Performance ad spend targets a specific goal, such as a purchase or sign-up.

- AI for Simplified Management and Performance: Launched in Q4 2024, Smart+ campaigns offer automated bidding, targeting, and creative solutions aimed at improving performance and streamlining management for advertisers. This rapid adoption signals a strong advertiser appetite for automated, AI-driven solutions on mobile platforms, especially those focused on driving a measurable bottom-line action.

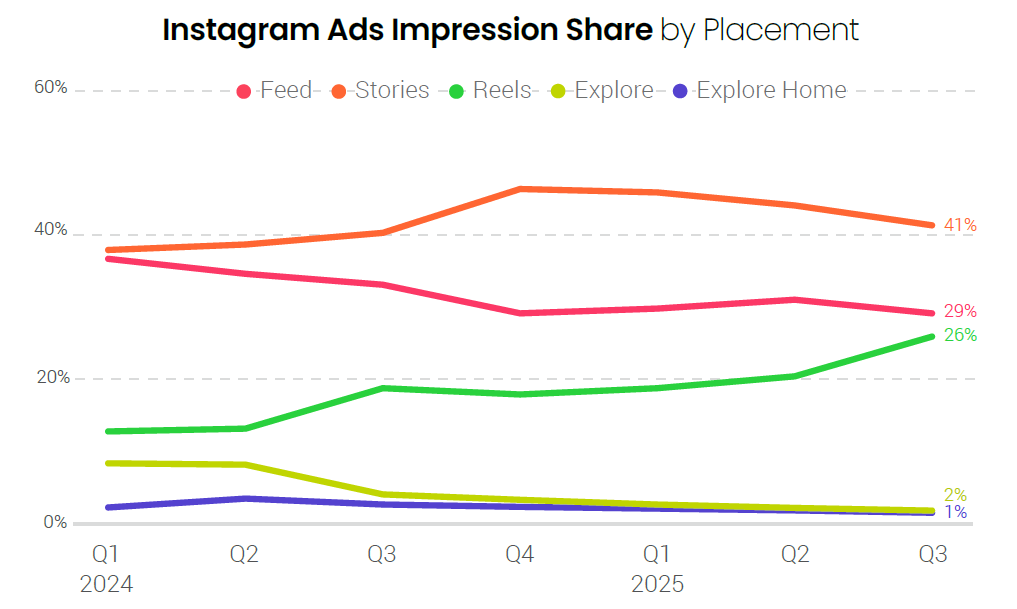

- Instagram ad impression share from Reels is growing, putting downward pressure on Instagram CPM.

- Reels Impression Share and Pricing: Reels placements accounted for 26% of Instagram ad impressions in Q3 2025, an increase from 21% in Q2 2025. This rise in Reels ads, which typically have a lower CPM than Feed and Stories ads, is contributing to a deceleration in Instagram’s year-over-year CPM growth. The CPM growth rate slowed from 19% in Q3 2024 to 11% in Q3 2025.

- Volume Driving Spending Growth: This increase in lower-priced Reels inventory is boosting volume and helping to accelerate spending growth. Instagram saw its spending growth improve to 21% in Q3, up from 11% in Q2, with impression growth accelerating to 9% year over year. For mobile marketers, the expanding Reels inventory provides a larger, more cost-efficient pool of impressions to drive overall spending and reach.

- As one in four Instagram ad impressions now comes from Reels, this placement is quickly moving from an experimental channel to a core component of a high-performing Instagram strategy. Successfully integrating mobile video into the advertising mix is key to capitalizing on the accelerating impression growth and optimizing cost-efficiency on Instagram.

The Q4 advantage: why retention outperforms acquisition when costs peak

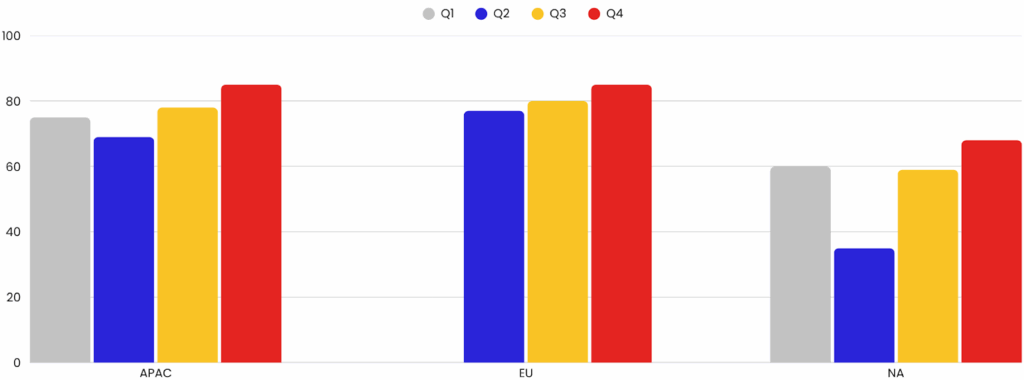

Trend 1: Retention growth in Q4: APAC, EU, and North America saw higher client (advertiser) retention rates than in other quarters

In Q4, we observed improved client retention across Mobupps advertisers in the APAC, Western Europe, and North America regions. This shift mirrors broader industry behavior: brands front-load UA earlier in the year and lean on remarketing/retention during peak season because retention yields far greater margin and conversion efficiency than fresh acquisition.

Q4 is the most expensive calendar window to recruit new customers. CPAs climb, auctions heat up, and acquisitions become far costlier than in normal months. Across industries, everything favors retention: numerous studies show that a small lift in retention drives outsized profit gains. For example, a 5% retention bump can raise profits by ~25–95%, while acquisition costs can be multiple times higher than retention spend. That dynamic explains why brands in APAC, EU, and NA are increasingly shifting budget into remarketing, VIP access, and owned-media flows in Q4 instead of purely chasing new installs.

The measurement partners confirm this strategic shift: remarketing budgets expanded meaningfully in H1 2025. Owned media / web-to-app tactics delivered big conversion uplifts, giving brands cheaper, higher-value conversions at scale.

Mobupps’ internal data supports this trend: average Day 1 advertiser retention improved by roughly 15-30% in Q4 compared to Q3 and Q2, signaling that more advertisers continue active campaigns throughout the peak season rather than pausing after initial flights.

Mobupps has found these steps underpinning the advertiser retention gains in APAC, EU, and NA during Q4: win back high-intent cohorts early, including VIPs and recent purchasers; protect inventory and maintain a smooth user experience for loyal customers; and deploy reactivation windows that prioritize repeat purchases and higher average order value (AOV) bundles.

This approach highlights a key insight: retention is more cost-effective and revenue-generating than acquisition in Q4. Existing customers are 9x more likely to convert, spend 3x more per transaction, and cost up to 80% less to market to than new users.

What are some tips for maintaining a high client retention rate?

- Move from seasonal UA to a full-funnel retention cadence: run early VIP access + post-purchase funnels that convert holiday buyers into repeat customers in January.

- Use owned media and deep linking to capture web traffic into app flows, where conversion rates and subsequent LTV are higher than many paid channels.

- Measure incrementality of remarketing (cohort tests) and favor bids for users with high repeat probability.

Remember that small changes in retention deliver outsized profitability.

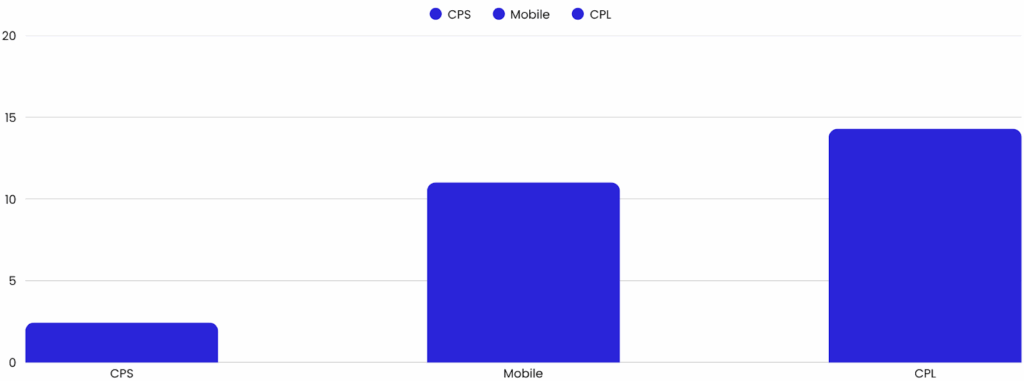

Trend 2: CPL campaigns – higher inactive-share risk in Q4 due to user attention, validation, and quality pressure

In Q4, CPL (Cost-Per-Lead) campaigns show a noticeably higher share of inactive or rejected campaigns compared to Mobile (CPM/CPV) and CPS (Cost-Per-Sale) programs, primarily due to lead quality, validation challenges, and user distraction during the busiest commercial quarter of the year.

CPL campaigns hinge on a discrete, verifier-ready action (a completed lead form or app registration). Many apps in finance, insurance, and utilities rely on this model to acquire users who can later be monetized through onboarding, upselling, or subscription flows. This makes CPL valuable for intent-rich performance but also creates more gates where campaigns can be labeled “inactive” – rejected leads, invalid form data, or non-compliant traffic.

During Q4, lead quality tends to decline as users are overwhelmed by holiday promotions and competing offers. Engagement windows shorten, attention fragments, and conversion accuracy drops, creating more rejections and inactivity. Many users fill out forms impulsively or with incomplete information, resulting in higher rejection rates.

Because CPS and broad mobile exposure programs rely on either a final sale (CPS) or simpler exposure metrics (CPM/CPV), there are fewer intermediate rejection points; a sale validates the conversion in one clean step, and impression/click buys don’t fail due to a poor lead form. That makes CPS and some mobile buys inherently less likely to be registered as “inactive,” even if downstream quality varies.

For apps and advertisers focused on long-term engagement, such as gaming and ad-monetized apps, where retention equals more sessions, impressions, and revenue, Q4 is a good period to scale activity. In contrast, lead-generation verticals (finance, insurance, telecom, etc.) may consider conserving CPL budgets until post-holiday, when user focus and intent stabilize.

What methods can be used to minimize this decrease?

- Treat CPL as a quality-first purchase: implement form validation, device fingerprinting, and fraud scoring before accepting leads.

- Prioritize remarketing and first-party user onboarding vs. broad lead capture during Q4 to improve ROI.

- Shift part of the budget to CPS or mobile exposure channels to maintain activity while user attention is fragmented.

- Reassess CPL strategies in January when consumer attention normalizes and lead validation accuracy improves.

AppGrowing: AI is reshaping the entire mobile advertising and marketing ecosystem

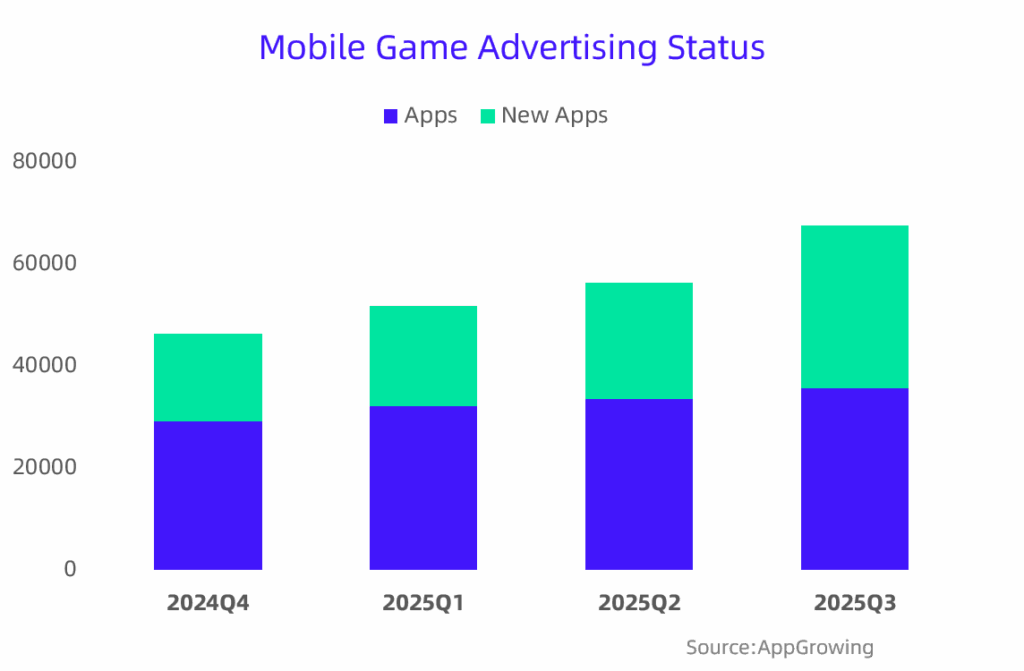

According to AppGrowing’s data, the global mobile gaming advertising market has continued to grow steadily throughout 2025. For example, the number of mobile games running ad campaigns increased consistently from Q1 to Q3. Notably, newly advertised titles in Q3 accounted for nearly half of all active campaigns — showing that publishers remain highly committed to investing in user acquisition. Even amid intense competition, most are still allocating significant advertising budgets to reach overseas users and expand their market share.

However, beneath these promising numbers, the market remains a red ocean dominated by top-tier publishers. For most companies, expanding overseas is no longer about rapid growth but about surviving in a zero-sum game. With traffic growth plateauing and user acquisition costs continuing to rise, many developers now face ad spend that exceeds revenue, leading to longer payback periods. The result is a paradox: performance metrics look strong, yet the business reality feels tougher.

So how can publishers break through this impasse? The key may lie in artificial intelligence (AI).

As we move further into 2025, rapidly advancing AI technologies are transforming every stage of the mobile advertising lifecycle. Generative AI can now produce high-quality creative assets — text, images, and even videos — at scale. Meanwhile, the growing accessibility and affordability of multimodal AI tools are helping marketing teams better understand market trends and creative strategies. This means marketers can identify opportunities and react faster, with fewer resources.

To support this shift, AppGrowing has launched two AI-powered tools: AI Creative Dissection and AI Strategy Analysis. These solutions help users uncover the true value of creative assets and make AI adoption easier. By combining AI technology with data modeling, users can quickly extract the key selling points of creatives through a professional “dissection” process. They can also interact directly with large language models to analyze results, identify winning creative patterns, and develop repeatable methods for creative optimization.

As paid user acquisition becomes standard practice, competition will increasingly depend on who can understand and respond to users more quickly and accurately. Leveraging AI effectively will be the decisive factor in boosting efficiency and maintaining a competitive edge.

Footnotes

Countries and tiers

We look at global data through a number of filters. One is country tiers, which because of our customer base we define as:

- China

- Japan

- Rest of world

- Tier 1 East: Korea, India

- Tier 2 East: Taiwan, Indonesia, Turkey, Thailand, Philippines

- Tier 1 West: Canada, France, Germany, UK

- Tier 2 West: Australia, Mexico, Brazil, Spain, Italy, Netherlands, Poland

- United States

About this data

All of this data is based on Singular’s view of the adtech ecosystem. While we have a significant share of the Mobile Marketing Platform space and see a huge amount of data, our insights will be biased towards actively marketing and growing apps that are spending significantly on user acquisition.