Content

Stay up to date on the latest happenings in digital marketing

Summary

-

Evaluate Payment Strategies: Marketing professionals should assess whether to stick with Apple's in-app payment system or transition to in-house payment processing, weighing the benefits of lower fees (2-3% vs. 30%) against the complexities of managing payment processing, customer data, and compliance across multiple jurisdictions.

-

Leverage Customer Ownership: By taking payments in-house, brands can gain greater control over customer relationships and communications, enabling personalized marketing strategies, upselling opportunities, and improved retention efforts, which are essential for maximizing lifetime value (LTV).

-

Prepare for Increased Competition: As higher-margin apps can afford to bid more aggressively for user acquisition, marketers should anticipate rising user acquisition costs and adapt their strategies accordingly, including optimizing campaign performance metrics and experimenting with pricing structures to remain competitive.

Apple’s grip on App Store payments has been legally broken in the United States. But should you take advantage of the situation and take iOS payments in-house … or should you stick with the in-app payment scheme that you know?

It’s still early days so how we think about this could change, but in this post I’m going to:

- Overview the changes briefly

- Highlight the major impacts for iOS apps in the United States

- Review the strategic decisions app developers need to make

- Provide a checklist to work through as you decide whether you want to take iOS payments in-house

One of my sources: a livestream that I participated in with FunnelFox and others on the new iOS app payments realities, which you can watch here. Also, don’t miss our post on how to measure off App Store payments with your MMP, so that you don’t miss out on campaign optimization, LTV calculation, ROAS calculation, and other critical parts of performance marketing for mobile apps.

Let’s go …

iOS payments: there’s new rules in place

Briefly, here’s the new changes that are in place:

- IAPs can now be OAPs

iOS apps can now direct users to third-party payment methods outside the App Store, making in-app purchases out-of-app purchases (or OAPs). For the first time, developers can bypass Apple’s 30% commission by offering web-based or alternative payment options. - Apple instantly complied with the legal ruling

Apple updated its App Store guidelines immediately to comply. So you are 100% in the clear to use this new methodology in the United States … and Spotify already submitted an updated app to take payments! - Apple Pay could be a near-seamless replacement

Since you can now do payments any way you want, you could theoretically run them right through Apple Pay, not just external redirects to websites. That means Apple Pay could become the seamless alternative with no need to enter a credit card number or give your payment information to a random company. In effect you switch from 30% fees to 2%-3% while keeping a native, high-converting user experience.

For more details, check my original blog post.

8 impacts of the new iOS payment rules

Lower fees are good, but this is a candy that might just have a sour center. There are some challenges to bringing iOS payments in-house.

Here’s 8 impacts, both good and bad:

- Technical and tax complexity

If you take iOS payments in-house for the United States, you now have to manage your own payment processing, including sales tax/VAT collection per U.S. state, or use a provider like Stripe. This can be complex and can involve registering in up to 50 separate jurisdictions. Clearly, this is easier for larger companies (Netflix, Spotify, ChatGPT) who can already handle global payments. - Ownership of the customer relationship

The company that bills a customer owns a customer. Everyone else is a service provider. Using third-party payments means developers own the billing relationship and customer data (real email, address, and more) which — though it has its costs — is very good. This enables direct customer communication, retention offers, and email marketing, and opens opportunities for personalized pricing, upsells, and bundling. - Lower payment fees, but higher operational costs

Apple Pay or credit cards charge ~2%-3% versus Apple’s 30%, but developers absorb payment fraud risks, chargebacks, customer support, and subscription management. Also, cancellation flows and refund handling become the developer’s responsibility. Fun times … - App Store review will become stricter

Don’t forget, Apple retains full control over app approvals. You can expect stricter reviews to prevent scammy or dark-pattern payment implementations … which already have infiltrated the App Store and now will be charging full speed ahead, sniffing out scam opportunities galore. - More pricing and productization freedom

Early adopters could see ~30% revenue gains from avoiding Apple’s commission. But you also get more pricing freedom (no more rigid App Store price tiers) and greater opportunity for bundling and productization. Now your product is whatever you want it to be, at whatever price you wish, whether 1-time or subscription. - Faster payouts

App store payouts take time. Taking payments yourself should result in faster payouts, which improves cash flow and accelerates your ability to reinvest in user acquisition. Which means an already light-speed industry is going to get even faster optimization and growth cycles. - User acquisition could get more expensive

Apps with higher margins that are now taking closer to 100% of what users are paying can bid more aggressively for users, likely driving up ad costs. Higher CPM, CPI, or CAC … not something you wanted, but definitely a possible impact of the new iOS payments reality. Ad network revenues should go up. - Retention and churn: more under your control

Customers are ultimately in charge, but owning payments means that you can try to save customers or payers with immediate discounts, payment pauses, or offers during a cancellation flow. For those who are tempted to re-create big telco-style loyalty departments, please remember that FTC regulations require easy cancellation options.

App publishers: strategic options

It’s important to note that you essentially have 3 options now. Stick with Apple, or choose 1 of 2 different ways of allowing customers to pay you directly.

- Leave payments with Apple

- Take payments in-house via a seamless process (Apple Pay, perhaps PayPal, etc)

- Take payments in-house via a web2app style process (link-outs for the store, or start UA on the web)

Each approach has different pluses and minuses. Here’s an overview …

3 ways to take payments

Apple IAPs | In-house payments (in-app or web redirect) | Web-to-app funnel | |

Commission | 15%-30% | ~2%-5% (Apple Pay, Stripe, etc.) | ~2%-5% |

User experience | Seamless, native | Can be seamless (Apple Pay), slight friction if web redirect | Most friction, multiple steps |

Payment compliance | Handled by Apple | Developer responsibility | Developer responsibility |

Tax collection | Handled by Apple | Developer must handle | Developer must handle |

Own customer data? | No (anonymized by Apple) | Yes | Yes |

Control over pricing | Limited to Apple price tiers | Full flexibility | Full flexibility |

App Store review risk | Low | Moderate to High | Low (for web) |

Cash flow speed | Apple payout cycle (30-45 days) | Faster, depends on payment processor | Faster, depends on payment processor |

Churn management | Limited | Full control | Full control |

Attribution data | Limited | Can be richer (with user email, ID, etc.) | Richest (full web attribution) |

Technical complexity | Low | Medium to high | High |

Best fit for ... | Indie developers, small studios | Mid-to-large apps, high revenue apps | High LTV apps, sophisticated UA teams |

How to make your decision on taking iOS payments in-house

So app publishers have some decisions to make. For some, it’s easy: big developers from big brands should instantly move to third-party iOS payments. Small developers with fewer resources: it’s likely best to stay where you are.

The mid-tier, however, that’s where you have some challenging decisions to make.

So: should you move to bring iOS payments in-house? Work through this checklist as you make your decision:

- Business readiness

- Annual app revenue > $1M (recommended threshold to justify complexity)

- Legal team ready for tax registration & compliance in 50 U.S. states

- Accounting can handle U.S. sales tax filings per state

- Payment infrastructure

- Third-party payment processor (e.g., Stripe, Paddle, Adyen) integrated

- Apple Pay set up for lowest friction (if staying “inside” app)

- Refunds, chargebacks, and cancellations process prepared

- Customer management

- CRM or email platform ready to handle customer data & communications

- Subscription management & retention flow ready (discounts, pauses, win-back)

- User acquisition & attribution

- Server-to-server event tracking or Conversion API implemented

- Deep linking capabilities if using web payments

- Ability to track payments across web and app

- Pricing experimentation framework ready

- Strategic fit

- Is owning the billing relationship important to your growth/retention plans?

- Are the new bigger margins high enough to support the additional costs/risks?

- Is increased flexibility (pricing, offers, bundles) valuable to your business?

- Risk mitigation

- Clear, easy cancellation flow (to comply with FTC regulations)

- Consistent merchant name between app and payment processor

- Review App Store guidelines frequently for changes

There’s a lot to work through. Make sure any change you implement makes sense long-term for your app.

Take your time to make a decision

Just because Spotify is instantly moving to manage its own iOS app payments doesn’t mean you have to. There is value in payments just being solved for you by a trusted brand like Apple, so don’t feel like you have to make a change just because you can make a change.

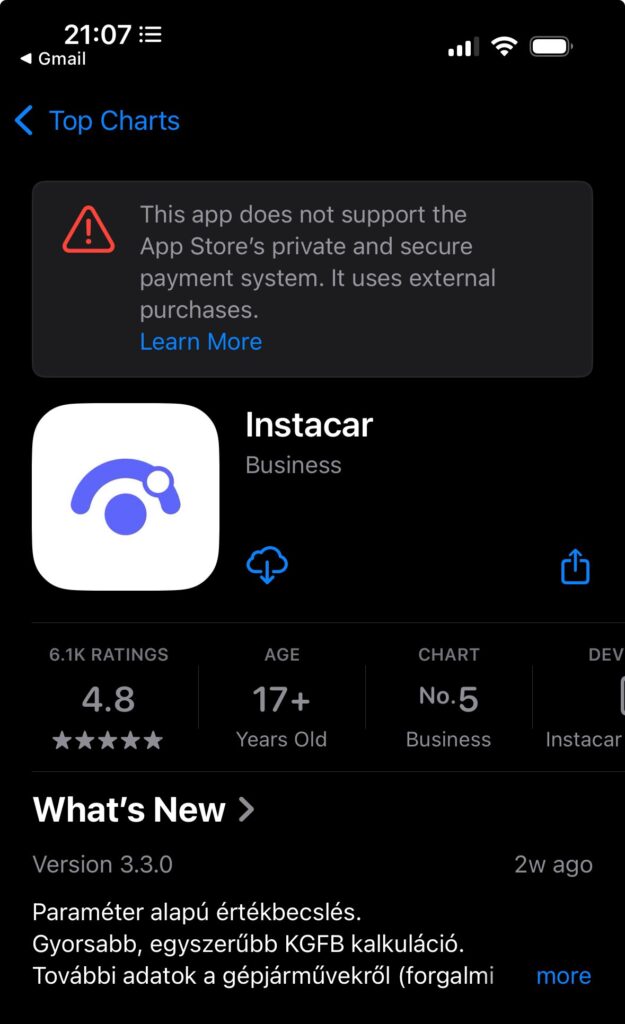

And Apple may do something in the U.S. market similar to what it has done in the EU: make a big alert in the app list about where your app takes payments. That could have a negative impact on your download velocity:

Make the right call, and don’t forget to build in testing time to see how it impacts user/customer/player behavior.

And if we can help, let us know.